Dental Practice Seller Accepted My Offer Then Changed Mind

Co-Founder, Minty Dental

In Summary

- Most dental practice LOIs are non-binding on price and deal terms—you typically cannot force a seller to complete the sale if they back out

- Exclusivity clauses (usually 60-120 days) and confidentiality provisions are often the only legally enforceable parts of an LOI

- Even when non-binding, LOIs create psychological anchoring—sellers and their advisors reference agreed terms throughout the transaction

- Earnest money deposits are rare before a signed purchase agreement; if you did put money down at the LOI stage, recovery depends on how the deposit terms were written

- Violation of exclusivity or confidentiality may give you limited recourse, but forcing the sale itself almost never happens without a signed purchase agreement

What Your Letter of Intent Actually Protects (And What It Doesn't)

The seller accepted your offer. You signed the LOI. Then they changed their mind. The first question most buyers ask is: "Can they do that?"

In most cases, yes—they can.

Most dental practice letters of intent are hybrid documents: non-binding on the deal itself, but binding on specific procedural commitments. The seller isn't legally required to sell you the practice at the agreed price, but they may be bound by other provisions they signed.

Non-binding on deal terms means you cannot force specific performance. Courts rarely compel someone to sell a business against their will based on an LOI alone. Price, structure, closing date, and transition terms are typically unenforceable until a purchase agreement is signed.

Binding on exclusivity and confidentiality means certain procedural protections may still apply. Exclusivity clauses typically lock the seller into negotiating only with you for 60–120 days. If they violated that window by entertaining another offer, you may have grounds for a breach claim. Similarly, if they disclosed your financial information to competitors, confidentiality provisions could give you recourse.

Where buyers often misread the situation is assuming "non-binding" means the LOI is meaningless. Even when deal terms aren't enforceable, the LOI creates structural and psychological anchoring. Sellers, brokers, and attorneys reference the agreed terms throughout due diligence. Walking back major provisions—like purchase price or transition length—feels adversarial, even when it's technically allowed. One buyer tried to renegotiate price after the LOI was signed, assuming the non-binding language gave them flexibility. The seller took it as bad faith and killed the deal.

Earnest money deposits are uncommon at the LOI stage in dental practice transactions. Most buyers don't put money down until the purchase agreement is signed. If you did submit a deposit with the LOI, whether you get it back depends entirely on how the deposit terms were written. Some LOIs specify that deposits are refundable if the deal doesn't close; others tie refunds to specific conditions like financing approval or satisfactory due diligence.

Sellers who back out after signing an LOI often do so because something changed—another offer came in, a family member objected, or they got cold feet about retirement. The legal question of whether they can back out is separate from the strategic question of whether the deal is salvageable. If exclusivity was violated, you may have a claim for damages (though quantifying those damages is difficult). If they simply changed their mind within the exclusivity window, your leverage is weaker.

The distinction that matters most: the LOI protects your process, not your outcome. It buys you time to complete due diligence without competition. It keeps your financial details private. But it does not guarantee you will own the practice. That guarantee only comes with a signed purchase agreement—and even then, contingencies can unravel deals before closing.

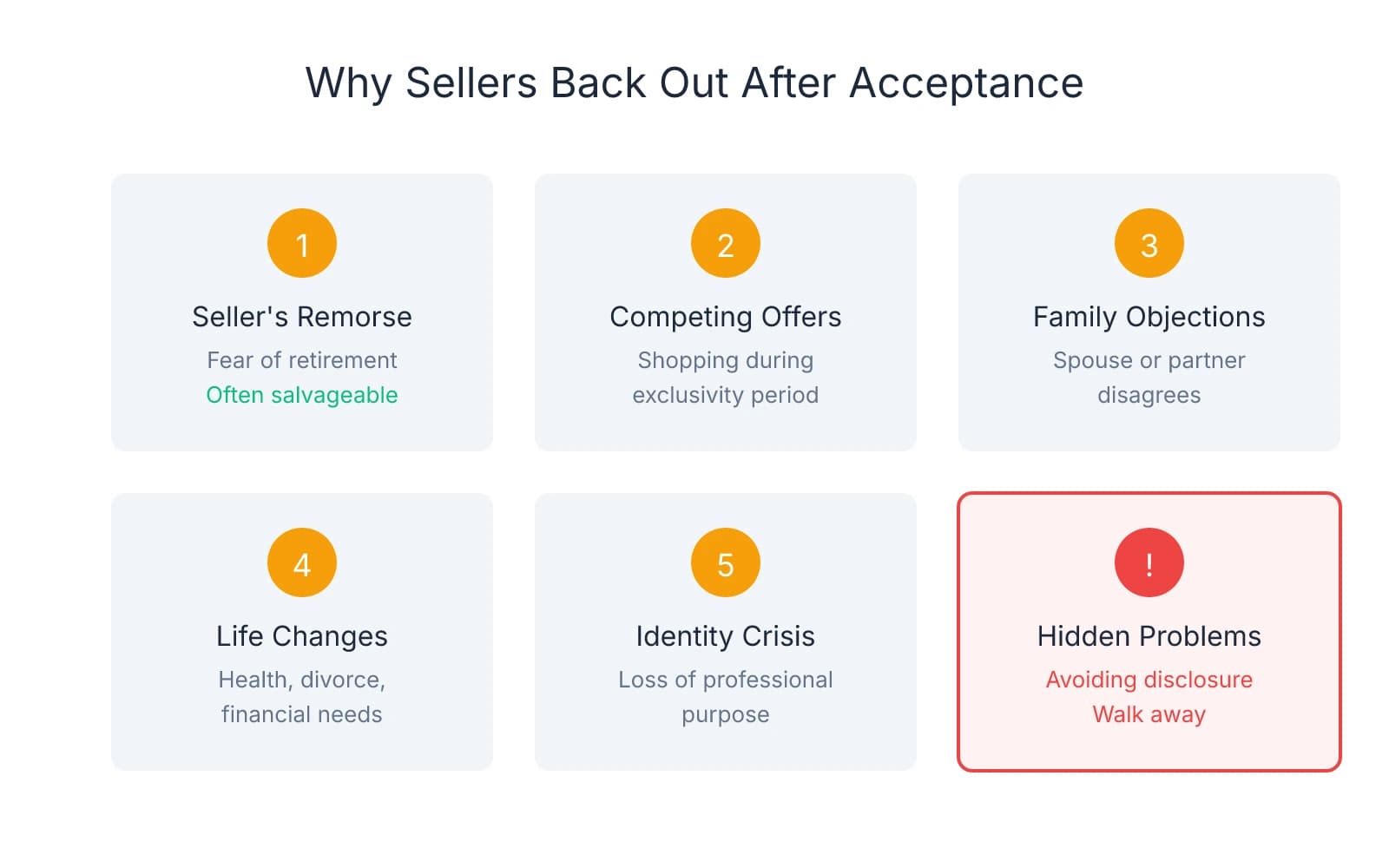

Why Sellers Back Out After Acceptance (And What It Reveals)

When a seller backs out after signing an LOI, the instinct is to assume bad faith. But what looks like betrayal is often fear—and understanding which kind determines whether the deal is salvageable.

Seller's remorse is the most common trigger. A dentist who built a practice over 25 years isn't just selling a business—they're closing a chapter of professional identity. That realization often hits hardest in the weeks after signing the LOI, when the abstract idea of "selling" becomes the concrete reality of "no longer being the owner."

This type of remorse is often salvageable. If the seller is withdrawing because they're scared of retirement, not because they found a better offer, a conversation about transition length or post-sale consulting can bring them back. One seller went silent two weeks after signing the LOI. When the broker finally reached him, the issue wasn't the price—it was that his wife had started asking what he'd do with his time. They restructured the transition from 60 days to six months with part-time clinical involvement, and the deal closed.

Competing offers during the exclusivity period signal something different entirely. If the seller violated the exclusivity clause by entertaining another buyer, that's not remorse—that's shopping. This happens when a practice hits the market and generates multiple inquiries in the first few weeks. Some sellers accept the first strong offer to create urgency, then continue fielding calls to see if they left money on the table. If the seller signed with another buyer during your exclusivity window, you may have grounds for a breach claim—but enforcing it is costly and time-consuming.

Family or co-owner disagreements that surface after the LOI often reveal poor succession planning. A seller who signed without consulting their spouse, business partner, or adult children may face resistance once the deal becomes real. This is particularly common in multi-doctor practices where one partner wants to sell and the other doesn't. These situations are rarely salvageable unless the objecting party can be brought into the negotiation.

Changed personal circumstances—health issues, divorce, sudden financial need—can make a seller reconsider timing even when they were committed at signing. These situations are unpredictable and usually non-adversarial. The seller isn't trying to hurt you; they're responding to life circumstances that override the transaction.

Cold feet about professional identity loss is especially common with sellers who define themselves by their clinical work. Dentists who haven't developed interests outside the practice often panic when they realize ownership was their primary source of meaning. If this is driving the seller's withdrawal, extended transition terms or a consulting role can help, but only if the seller is self-aware enough to name the issue.

The red flag scenario that should make you walk away entirely: the seller discovers problems during their own due diligence prep and backs out to avoid disclosure. This happens when a seller agrees to terms, then starts pulling financials for your review and realizes revenue has been declining, a key associate is leaving, or the lease renewal they assumed was automatic isn't happening. Rather than disclose the issue and renegotiate, some sellers simply withdraw and blame "personal reasons."

The pattern that separates salvageable situations from dead deals is whether the seller's objection is about the deal or about themselves. If they're reconsidering because of fear, identity loss, or family pressure, there may be room to adjust terms or timeline. If they're backing out because they found a better offer, discovered problems they don't want to disclose, or never intended to honor exclusivity, your best move is to move on.

Your Options When the Seller Backs Out

When a seller withdraws after signing the LOI, the best path depends on what you're actually trying to accomplish—and how much time you're willing to spend on a transaction that's already shown cracks.

Option 1: Attempt to salvage the deal makes sense when the practice fundamentals are strong and the seller's withdrawal stems from fear rather than opportunism. If the seller is backing out because they're scared of retirement or worried about patient continuity, those concerns can often be addressed through deal structure rather than price.

One protection many buyers overlook is offering more structured transition support. If the seller is anxious about walking away from patients they've treated for decades, propose extending the transition from 60 days to 90 or 120, with defined clinical involvement and patient introduction protocols. If they're worried about income loss, consider a consulting arrangement where they remain available for complex cases for six months post-close.

When you reach out, lead with curiosity rather than accusation. "I wanted to understand what changed for you" lands better than "we had an agreement." One buyer discovered the seller's spouse was the real objection—she hadn't been involved in the decision and felt blindsided. The buyer invited both of them to lunch, walked through the transition plan in detail, and addressed her concerns about patient care directly. The deal closed three months later.

Salvage attempts only work if the seller is still operating in good faith. If they violated exclusivity by signing with another buyer, or if they're using your offer as leverage to extract better terms from someone else, negotiation is a waste of time. The signal that tells you which situation you're in: whether the seller will get on the phone.

Option 2: Pursue limited legal recourse is rarely worth the cost, but there are narrow situations where it makes sense. If the seller violated a binding exclusivity clause—meaning they entertained or accepted another offer during your protected negotiation window—you may have grounds for a breach claim. The damages you can recover are typically limited to your out-of-pocket costs: attorney fees for LOI review, due diligence expenses, and potentially lost opportunity costs.

What you almost certainly cannot do is force the sale itself. Specific performance lawsuits, which compel a party to complete a transaction, generally require a fully executed purchase agreement—not an LOI. Courts are reluctant to force business sales based on preliminary agreements, especially when the LOI explicitly states that deal terms are non-binding.

The practical reality is that litigation over an LOI breach is a losing proposition for most buyers. Legal fees will run $15,000–$30,000 minimum, the timeline stretches 12–18 months, and the outcome is uncertain. The one scenario where legal action makes strategic sense: when the seller's breach was egregious and you want to establish a public record that protects your reputation with lenders and brokers.

Option 3: Walk away strategically is often the fastest path back to ownership. The question to ask yourself is whether fighting for this specific practice is worth delaying your search by 6–12 months. The opportunity cost of spending a year in litigation or renegotiation is that you're not looking at other practices, building lender relationships, or positioning yourself for better opportunities.

If you put down an earnest money deposit at the LOI stage, your ability to recover it depends entirely on how the deposit terms were written. If the LOI specifies that deposits are refundable if the deal doesn't close, you should get your money back within 30 days. If the language ties refunds to specific conditions (financing approval, satisfactory due diligence), and the seller backed out before those milestones, you're in a stronger position.

Before you move on, document the timeline and communications for future reference. If you're working with a broker, send a formal email summarizing what happened, when the seller withdrew, and whether any binding provisions were violated. This creates a paper trail that protects you if the seller or broker tries to reframe the situation later.

The lesson most buyers take from a failed LOI is what not to do next time. Did you skip a critical due diligence step before signing? Did you miss red flags in the seller's behavior during negotiation? Did your LOI lack a strong exclusivity clause or clear deposit terms? One pattern that appears repeatedly is buyers who rush to sign an LOI because they're afraid of losing the deal, then discover during due diligence that the practice wasn't what they thought.

The strategic frame that helps most buyers move forward: this wasn't your practice. If it were, the seller wouldn't have withdrawn. The next practice you pursue will benefit from everything you learned here.

Protecting Yourself in Future Offers: LOI Provisions That Matter

The best defense against seller withdrawal isn't litigation after the fact—it's structuring your next LOI to minimize the risk before you sign. That doesn't mean drafting a document so aggressive it scares off sellers. It means knowing which provisions actually protect you.

Exclusivity provisions are the most enforceable protection you have at the LOI stage. Standard language gives you 60–90 days where the seller cannot solicit, entertain, or accept competing offers. The key is making sure the clause defines what "exclusivity" means. Weak language like "the seller agrees to negotiate exclusively with buyer" leaves room for interpretation. Stronger framing specifies that the seller will not "directly or indirectly market the practice, respond to inquiries from other buyers, or enter into discussions regarding a sale with any third party" during the exclusivity period.

Where buyers often get burned is assuming exclusivity starts when they want it to. The clock typically begins the day the LOI is signed, not the day you start due diligence. One adjustment worth negotiating: exclusivity that begins when you receive full financial documentation, not at signing. This protects you if the seller delays providing records.

Earnest money structure is less common at the LOI stage in dental practice transactions than in real estate, but when it's used, the terms matter. Deposits typically range from $5,000–$25,000 depending on practice size, and they're held in escrow until closing. The protection you need is clear language on refund conditions: under what circumstances do you get your money back, and who decides?

The strongest structure ties deposit refunds to objective milestones—financing approval, satisfactory due diligence findings, lease assignment approval—rather than subjective seller satisfaction. Many first-time buyers assume earnest money is automatically refundable if the deal falls through, but that's only true if the LOI says so explicitly.

Contingencies that protect you are the escape hatches that let you walk away without penalty if something material changes. The most common: financing approval, due diligence findings, lease assignment approval, and key staff retention.

The balance here is being specific without being unreasonable. "Buyer may terminate for any reason" makes you look unserious. "Buyer may terminate if collections in the most recent 12 months are more than 15% below seller's representations" is defensible. One contingency many buyers overlook: seller's continued operation of the practice during the transition period.

Seller representations are where you lock in the claims the seller made during initial conversations. These are statements the seller affirms are true as of the LOI signing date: that practice financials are accurate and complete, that no material changes have occurred in the past 12 months, that they have full authority to sell, and that there are no undisclosed liabilities or pending legal issues.

The reason these matter is that they create a baseline for due diligence. If the seller represented that collections averaged $850,000 annually and you later discover they were $720,000, you have grounds to renegotiate or terminate based on misrepresentation. One pattern worth noting: sellers who resist including basic representations in the LOI often have something to hide.

Consequences for seller breach are rare in dental practice LOIs, but they're not impossible. Liquidated damages clauses—where the seller agrees to pay a specific amount if they back out without cause—are uncommon because they make the LOI feel adversarial. More realistic is language requiring the seller to reimburse your out-of-pocket due diligence costs (attorney fees, accountant review, appraisal expenses) if they withdraw after you've incurred them.

The challenge with enforcement provisions is that they only work if you're willing to litigate. The real value is deterrence—sellers who know they'll owe $10,000 in reimbursed expenses are less likely to walk away casually.

The balance between protection and cooperation is where many buyers miscalculate. Overly aggressive LOIs signal that you're litigious, which makes sellers nervous even when your terms are fair. One buyer included a clause requiring the seller to pay $50,000 in liquidated damages if they backed out for any reason. The seller's attorney advised them to reject the offer entirely, and the buyer lost the practice to a competing bid with simpler terms.

The frame that works better: structure the LOI to protect your time and money, not to punish the seller for changing their mind. Strong exclusivity, clear contingencies, and reasonable deposit terms accomplish that without making the transaction feel adversarial.

When to involve legal counsel is earlier than most buyers think. The time to have an attorney review your LOI is before you sign it, not after the deal collapses. A good attorney can structure provisions that protect you without scaring off the seller. The cost is typically $1,000–$2,500 for LOI review and negotiation, which is a fraction of what you'll spend if the deal falls apart.

One mistake first-time buyers make is assuming the seller's broker or attorney will draft a fair LOI. Brokers work for the seller, and their incentive is to close deals quickly with minimal friction. That often means LOIs with weak exclusivity, no deposit, and vague contingencies—terms that favor the seller if they change their mind.

The lesson that carries forward to every future transaction: the LOI is where you set the tone for how the deal will unfold. Sellers who honor strong exclusivity clauses, provide complete documentation on time, and communicate transparently during the LOI phase tend to behave the same way through closing. Sellers who push back on reasonable protections, delay providing records, or go silent for days at a time are showing you how they'll act under pressure. Pay attention to those signals—they're often more predictive than the deal terms themselves.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Letters of intent: Binding or non-binding - McDonald Hopkins— mcdonaldhopkins.com

- What Is Clinical Overlap in Dental Transitions? Webinar Recap— www.dentalbuyeradvocates.comIndustry

- contingencies can unravel deals— minty.com

- Managing Emotional Factors: Dealing with 'Seller's Remorse' - OffDeal— offdeal.ioIndustry

- Some sellers accept the first strong offer to create urgency— minty.com

- Dentists who haven't developed interests outside the practice often panic when they realize ownership was their primary source of meaning— minty.com

- Specific Performance: How a Real Estate Purchaser Can Force a ...— ansell.lawIndustry

- One pattern that appears repeatedly is buyers who rush to sign an LOI because they're afraid of losing the deal— minty.com

- Many first-time buyers assume earnest money is automatically refundable if the deal falls through— minty.com

Navigate seller uncertainty with expert guidance

Dealing with a seller who's having second thoughts? Minty Plus provides hands-on acquisition support to help you navigate deal complications and protect your interests throughout the entire process.