LLC vs S Corp for Buying a Dental Practice: Which Structure Fits

Co-Founder, Minty Dental

In Summary

- LLC is a legal entity structure providing liability protection; S corp is a tax election layered on top — you can have an LLC taxed as an S corp

- The core tax difference: LLC default taxation subjects all profit to 15.3% self-employment tax, while S corp splits income into salary (payroll taxed) and distributions (not subject to self-employment tax)

- Most dental buyers form an LLC or PLLC first, then elect S corp taxation when net profit reaches $200,000+

- You don't lock into a tax structure on day one — many buyers start as an LLC and file for S corp status later when the math justifies it

The Real Difference Between LLC and S Corp Isn't What Most Buyers Think

Most first-time buyers treat LLC vs S corp as a binary choice — as if picking one means forgoing the other. That's not how it works. LLC is a legal entity structure that determines how your practice is organized and protected. S corp is a tax election that determines how the IRS treats your income. You can have an LLC taxed as an S corp. That's the setup most dental buyers eventually land on.

The confusion stems from casual conversation. When someone says "I'm an S corp," they usually mean they've elected S corp taxation for their LLC or professional entity. The legal structure underneath — whether it's an LLC, PLLC, or professional corporation — is a separate decision. For dental buyers, the legal structure question is usually straightforward: form an LLC or PLLC for liability protection and operational flexibility. The tax question is where the real decision sits.

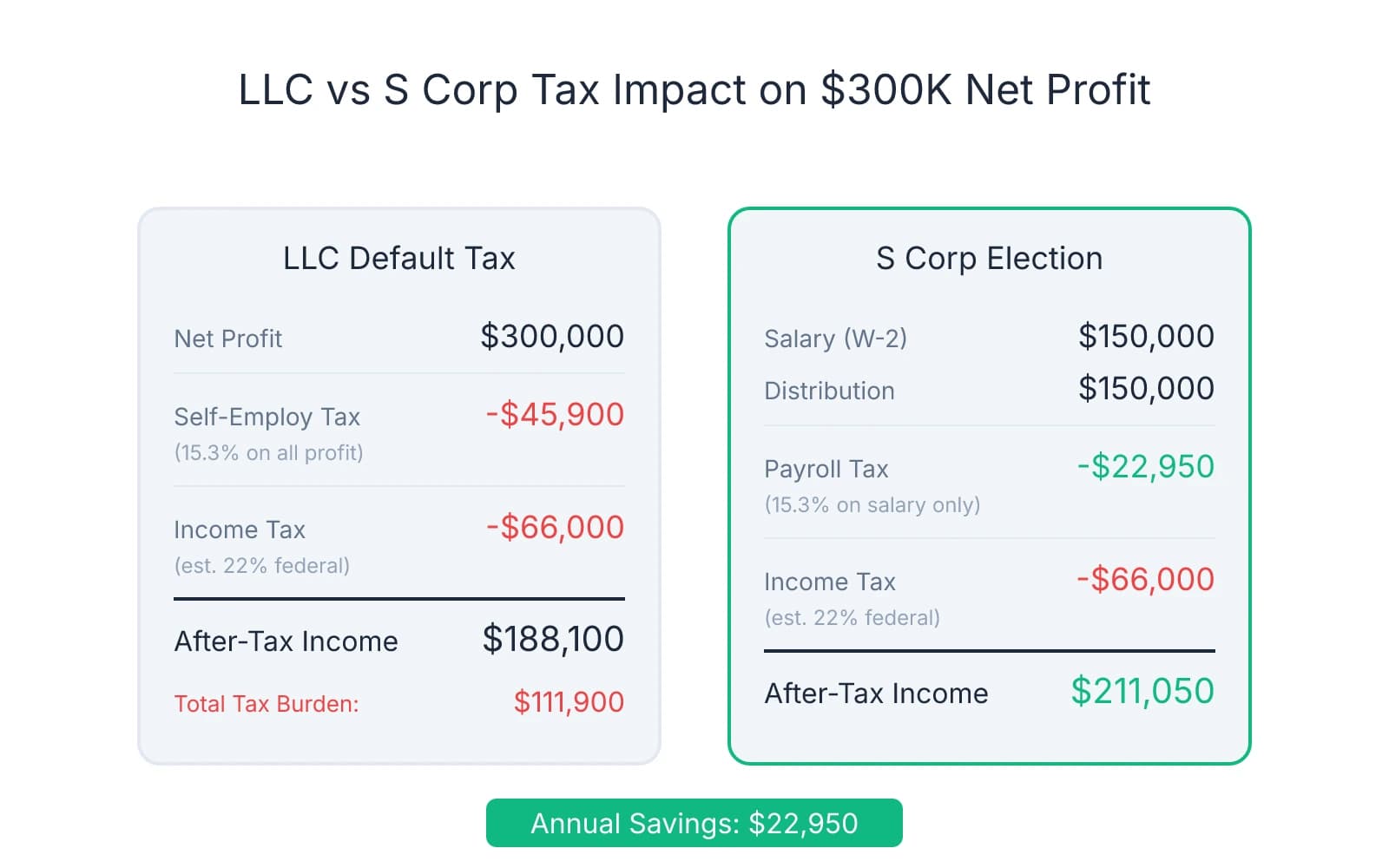

Here's the core tax difference. When you operate as an LLC without making any special election, the IRS treats all your profit as self-employment income. That means every dollar of net profit gets hit with 15.3% self-employment tax on top of federal and state income tax. If your practice nets $300,000, you're paying roughly $45,900 in self-employment tax before income tax even enters the picture.

S corp taxation changes that structure. You split your income into two buckets: salary and distributions. Your salary gets treated like any W-2 employee's pay — subject to payroll taxes. But distributions beyond that salary aren't subject to the 15.3% self-employment tax. Using the same $300,000 example, if you pay yourself a $150,000 salary and take $150,000 in distributions, you're only paying payroll taxes on the salary portion. That's roughly $22,950 in payroll tax instead of $45,900 — a $22,950 annual savings.

The catch is that the IRS requires you to pay yourself a "reasonable salary" for the work you do. You can't pay yourself $50,000 and take $250,000 in distributions just to dodge payroll taxes. For dentists, reasonable compensation typically falls in the $120,000–$180,000 range depending on your region, specialty, and practice revenue. Underpay yourself and you risk an audit. Overpay and you're leaving money on the table.

Most buyers don't need to make this decision on day one. You can start as an LLC, get the practice stabilized, and elect S corp status later when your net profit justifies the administrative cost. S corp requires payroll processing, quarterly filings, and tighter bookkeeping — expenses that don't make sense until you're clearing at least $200,000 in net profit. Below that threshold, the tax savings often don't outweigh the added complexity and cost.

One pattern worth noting: many buyers assume they need to match the seller's entity structure. You don't. If the seller operated as a sole proprietorship or partnership, you're free to form an LLC and elect S corp taxation from the start. The structure you choose is independent of how the practice was previously run. The only constraint is your state's professional licensing rules — some states require dentists to operate as a PLLC or professional corporation rather than a standard LLC.

When S Corp Election Actually Saves Money (And When It Costs You)

The math on S corp taxation looks compelling on paper — save $22,950 a year by avoiding payroll taxes on half your income. But that calculation leaves out the costs and constraints that come with the election. With the added expenses factored in, the breakeven point typically sits around $200,000 in annual net profit.

Below that level, the added costs start eating into your savings. S corp requires payroll processing, which runs $1,500–3,000 annually depending on your provider and pay frequency. Your tax preparation gets more complex — expect to pay an additional $1,000–2,000 for the extra filings and compliance work. You're also taking on quarterly payroll tax deposits, annual W-2 and W-3 filings, and stricter bookkeeping requirements to separate salary from distributions. When your practice is netting $150,000, a $10,000 tax savings minus $4,000 in added costs leaves you with $6,000 — not nothing, but not the windfall the headline number suggests.

The real leverage appears when net profit crosses $250,000–300,000. At that level, you're saving $15,000–25,000 annually in payroll taxes, and the administrative costs become a smaller percentage of the benefit. One pattern many buyers notice: the S corp election makes more sense in year two or three of ownership, once you've stabilized revenue and have a clearer picture of what the practice actually nets after your draw.

The IRS reasonable compensation requirement is where many dentists miscalculate. You can't just pick an arbitrary salary and maximize distributions. The IRS expects you to pay yourself what a dentist in your role would earn on the open market — typically 40–60% of net income for owner-operators. If your practice nets $300,000, a $120,000 salary might trigger scrutiny, while $180,000 would likely pass review. The exact threshold depends on your region, specialty, and how much clinical work you're doing versus managing the practice.

The IRS has been clear on this: shareholder-employees must receive reasonable compensation before taking distributions. Underpay yourself and you're not just risking an audit — you're potentially reclassifying distributions as wages retroactively, which means paying back payroll taxes plus penalties and interest.

One factor that's shifted the calculus for smaller practices: the Qualified Business Income (QBI) deduction. For practices with taxable income under $500,000, LLC default taxation may allow larger deductions because all profit qualifies for the 20% QBI deduction. Under S corp taxation, only your distributions count toward QBI — your salary doesn't qualify. If you're paying yourself $150,000 in salary and taking $150,000 in distributions, you're only getting the QBI benefit on the distribution portion.

This has changed the breakeven analysis for practices netting $200,000–300,000. Where S corp used to be the default recommendation at that income level, many CPAs now run both scenarios to see whether the payroll tax savings outweigh the reduced QBI deduction. For some buyers, staying in LLC default taxation for another year or two maximizes total tax efficiency — especially if they're planning significant equipment purchases or other deductions that would lower taxable income below the QBI phase-out threshold.

The decision isn't static. You can elect S corp status in January of any year by filing Form 2553 with the IRS. Many buyers start as an LLC, track their first full year of net profit, and make the election once they're confident they'll consistently clear $200,000+. That approach avoids locking into payroll obligations before you know what the practice will actually generate under your ownership.

One protection worth building in: work with a CPA who specializes in dental practice taxation, not just general small business accounting. The reasonable compensation analysis for dentists is specific enough that generic benchmarks don't apply. Your CPA should be pulling salary data for your specialty and region, not just applying a flat 50/50 split.

The Reasonable Compensation Problem That Trips Up New Owners

The IRS defines reasonable compensation as what you'd pay another dentist to perform your role — considering your experience, location, and the practice's revenue. That sounds straightforward until you're the one setting your own salary. Many new owners underestimate how closely the IRS scrutinizes professional services businesses, where the owner's clinical skill generates most of the revenue.

The scrutiny exists because the incentive to underpay is obvious. Every dollar you shift from salary to distributions saves 15.3% in payroll taxes. For a practice netting $300,000, the difference between a $100,000 salary and a $180,000 salary is roughly $12,240 in annual payroll tax. But the IRS knows the math too, and they've built enforcement around professional services specifically because the temptation to manipulate compensation is highest in businesses where the owner is also the primary producer.

Industry guidance suggests 40–60% of net income as salary for owner-dentists, though this range shifts based on production level and whether you have associate coverage. A solo practitioner producing $800,000 in collections might justify a $200,000 salary — 25% of production — if comparable associate dentists in the area earn $180,000–220,000. But a multi-doctor practice where the owner is doing less clinical work and more management might need to adjust that calculation.

One pattern that consistently triggers audits: paying yourself less than what you'd pay an associate. If you're advertising associate positions at $150,000 but paying yourself $90,000 as the owner-operator, the IRS will ask why your compensation is lower than what you're offering employees. Without documentation showing a defensible rationale — maybe you're working fewer clinical hours, or the associate role includes production bonuses that you're taking as distributions instead — the IRS will reclassify the difference.

When reclassification happens, the consequences compound quickly. The IRS treats the underpaid portion as wages, which means you owe back payroll taxes on the reclassified amount — both the employer and employee portions. Add a 20% penalty for negligence, plus interest calculated from the date the taxes were originally due, and a $50,000 underpayment can cost you $70,000–80,000 by the time it's resolved.

Documentation is your primary defense if your compensation gets questioned. Board minutes approving your salary, salary surveys from dental associations showing regional benchmarks, and market comparisons to associate positions in your area all help justify your number. When an auditor asks why you paid yourself $120,000 instead of $180,000, "it seemed reasonable" doesn't hold up. "Here's the ADEA salary survey for my region, here are three comparable associate postings, and here are board minutes documenting the decision" does.

One complication many buyers miss: lower salary reduces your 401(k) contribution limits. Retirement contributions are based on W-2 wages, not distributions. If you pay yourself $100,000 in salary, your maximum 401(k) contribution is calculated on that $100,000 — not the $200,000 you took home after distributions. For buyers prioritizing retirement savings, artificially suppressing salary to maximize payroll tax savings can backfire by capping how much you can shelter in tax-deferred accounts.

Where buyers often get burned is treating salary as a static decision. You set it in year one and forget about it. But as your practice grows — or as you bring on associates and shift from clinical production to management — your reasonable compensation changes. A $150,000 salary might be defensible when you're producing $700,000 solo. Three years later, when you're producing $500,000 and managing two associates, that same salary might be too high relative to your clinical role.

The safest approach: document your compensation decision annually. Pull current salary data, compare it to your role and production, and record the rationale in board minutes. If your salary stays flat while profit doubles, you should be able to explain why. If you cut your salary after hiring an associate, the documentation should show how your role changed.

Choosing Your Structure Before Closing (And When to Change It Later)

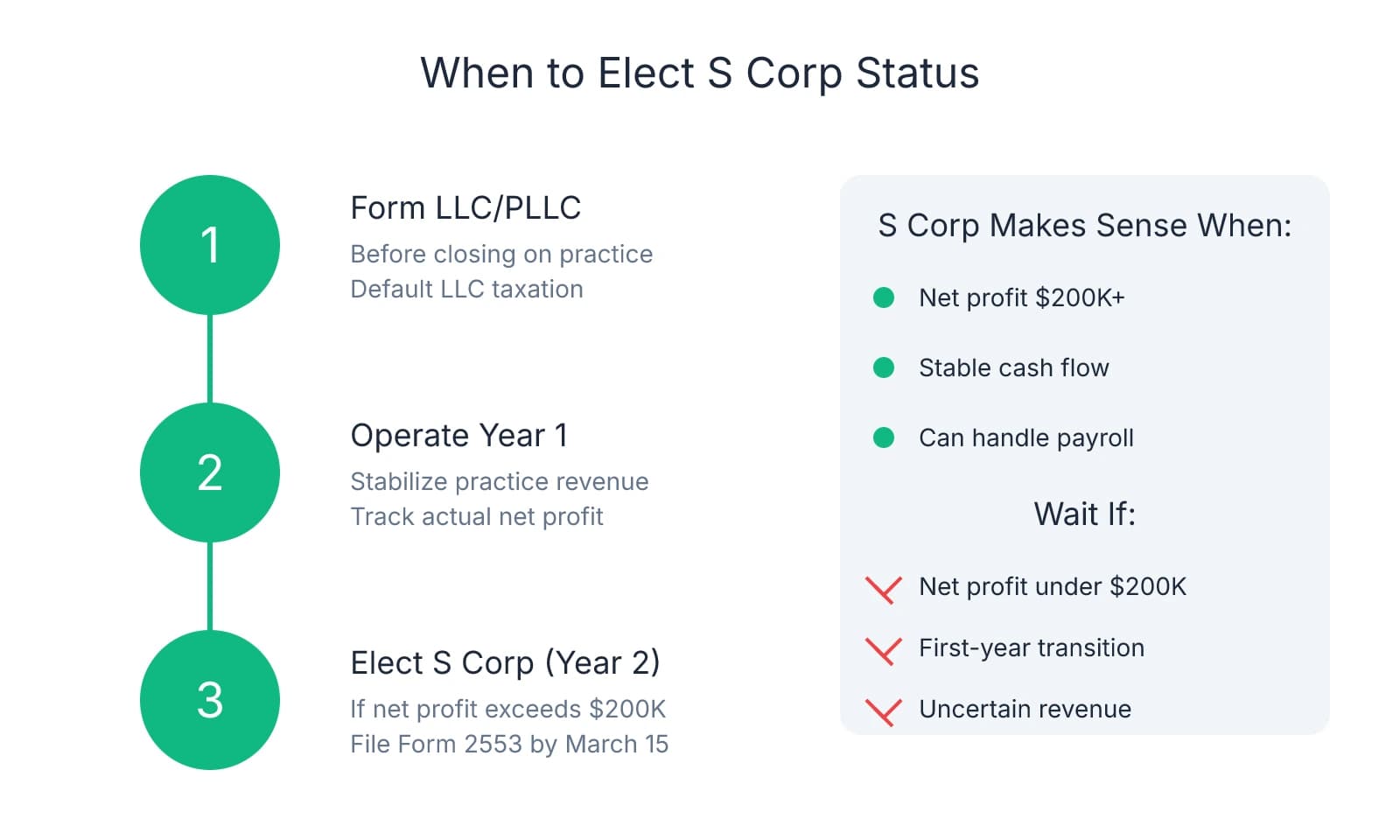

One misconception that slows down many buyers: you don't need to finalize your tax structure before closing. The acquisition itself requires a legal entity — typically an LLC or PLLC depending on your state's professional licensing rules — but the tax election can wait. Most buyers form their entity, close on the practice, and make the S corp decision six to twelve months later once they understand what the practice actually generates under their ownership.

This staged approach removes pressure from an already complex transaction. You're not guessing at reasonable compensation before you've seen a full year of revenue. You're not committing to payroll processing during the transition period when cash flow is tightest. And you're not locking into administrative obligations before you know whether the practice will clear the $200,000+ net profit threshold where S corp starts making financial sense.

The mechanics are straightforward. You form your LLC or PLLC, use that entity to acquire the practice, and operate under default LLC taxation for your first year. All profit flows through to your personal return as self-employment income — you'll pay the 15.3% self-employment tax, but you avoid payroll setup, quarterly filings, and the reasonable compensation analysis. Once you've closed your first full year and know what the practice nets, you file Form 2553 with the IRS to elect S corp taxation going forward.

Timing matters here. S corp election must be filed by March 15 of the tax year you want it to take effect, or within 75 days of forming your entity if you're electing from day one. Miss that window and you're stuck with LLC default taxation for the rest of the year. But if you're buying mid-year and closing in September, waiting until the following January to elect S corp often makes more sense than rushing the decision during the transition.

One pattern worth noting: many buyers operate as an LLC for year one specifically to absorb startup losses and transition costs without the added complexity of payroll. If you're investing in equipment upgrades, software conversions, or marketing to rebuild patient volume after the sale, those expenses can reduce or eliminate net profit in your first year. Running payroll and maintaining S corp compliance when you're barely breaking even — or operating at a loss — adds administrative cost without delivering tax savings.

Year two is typically when the S corp election makes sense. By then, you've stabilized revenue, you understand your true net profit, and you can set a defensible salary based on actual production rather than projections. If your first-year net profit came in at $220,000 and you expect similar or higher performance in year two, electing S corp status at the start of year two captures the tax savings going forward.

One consideration that affects timing: changing from LLC to S corp is straightforward — you file Form 2553 and start running payroll. Reversing the election is harder. If you elect S corp status and later decide it's not working, you're generally locked in for five years before you can revoke the election and return to LLC default taxation. This asymmetry favors starting conservative. If you're unsure whether your net profit will consistently exceed $200,000, waiting a year to elect S corp carries minimal downside.

The decision framework comes down to projected net profit and administrative capacity. If you're confident the practice will net $250,000+ and you have the systems in place to handle payroll and quarterly filings, electing S corp from day one can work. If you're buying a practice that's been underperforming and you're planning significant changes to rebuild revenue, starting as an LLC and revisiting the decision after year one reduces complexity during the transition.

Where buyers often stumble: defaulting to S corp because "everyone does it" without running the actual numbers. Your dental-focused CPA should model both scenarios based on your projected income, reasonable compensation for your region and role, and the QBI deduction impact at your income level. For practices netting under $300,000, the QBI deduction can shift the math enough that LLC default taxation delivers better total tax efficiency than S corp, especially in your first few years of ownership.

The recommendation most buyers benefit from: form your LLC or PLLC before closing, operate under default taxation for year one, and elect S corp status in year two if your net profit justifies it. This approach gives you flexibility during the transition, lets you make the tax decision based on real data rather than projections, and avoids locking into administrative obligations before you're ready. Work with a CPA who understands dental practice economics — not just entity structures in general — and who can model your specific numbers rather than applying generic thresholds.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- S Corp vs. LLC for Dentists: Which Is More Tax Efficient?— losangelescpa.orgIndustry

- Do You Have to Keep the Same Structure When Buying a Dental ...— www.agslawfirm.com

- S corporation compensation and medical insurance issues - IRS— www.irs.govGovernment

- Choosing the Most Tax-Efficient Business Structure for Your Practice— www.cainwatters.com

Frequently Asked Questions

Ready to structure your dental practice acquisition?

Choosing the right entity structure is crucial when buying a dental practice. Minty Plus provides expert guidance on tax-efficient ownership structures and handles the complexities of practice acquisition so you can focus on clinical excellence.