Should You Form an LLC Before Making an Offer on a Dental Practice?

Co-Founder, Minty Dental

In Summary

- The letter of intent is signed personally by the buyer—not by an LLC—and most sellers and brokers expect this standard approach

- Forming an entity before you have a signed LOI means paying annual fees, registered agent costs, and potential name conflicts for a structure you might not use

- Lenders require entity documents only after the LOI is signed and you're moving into formal loan application—not during the offer stage

- The LOI should include language confirming you'll form an appropriate entity before closing, which satisfies both seller and lender expectations

- Having an existing LLC does not make your offer more competitive or credible to sellers—the strength of your offer comes from financing, terms, and transition planning

Entity Formation Happens After the LOI, Not Before

The letter of intent in a dental practice acquisition is signed by you personally, not by a business entity. This surprises many first-time buyers who assume they need an LLC in place before making an offer, but the standard practice is straightforward: you sign as an individual, with the understanding that you'll form the appropriate entity before closing.

Forming an LLC before you have a signed LOI creates unnecessary costs and complications. Annual state fees, registered agent expenses, and ongoing compliance requirements start the moment your entity is approved—whether or not you close on a practice. If the deal falls through, you're left paying for a structure you don't need.

Entity formation timing: The practical sequence is offer → LOI → entity formation → loan application → closing. Lenders don't need to see entity documents until after the LOI is signed and you're moving into formal loan application. At that stage, they'll require proof of entity formation, an EIN, and often a resolution authorizing the entity to borrow.

The LOI should include language stating that the buyer will form an appropriate entity before closing. A standard clause might read: "Buyer will form a professional limited liability company or other appropriate entity under [state] law prior to closing, and all closing documents will reflect the entity as purchaser." When negotiating the terms of your letter of intent, this language protects you from being locked into a specific entity type before you've consulted with your attorney and accountant.

One misconception worth addressing: having an existing LLC does not make your offer more competitive or credible to sellers. The strength of your offer comes from your financing, your proposed terms, and your transition plan—not from whether you've already filed paperwork with the state. Sellers evaluate offers based on price, structure, and the likelihood of closing.

If you're currently working as an associate and already have an LLC for tax purposes, you'll need to decide whether to use that entity or form a fresh one for the acquisition. That decision depends on factors like existing liabilities, name alignment with the practice you're buying, and lender preferences—but it's a decision you make after the LOI is signed. In some states, the entity choice itself may be limited by professional licensing requirements, making it even more important to wait until you have specific guidance from your advisors.

The Four-Layer Registration Process Takes 2-6 Weeks

With the LOI signed and your timeline established, entity formation becomes the next critical step. The process isn't a single filing—it's a sequence of registrations across four government levels, each with its own timeline and requirements. Most buyers underestimate how long this takes, particularly when state dental boards need to approve professional entities before they're officially recognized.

Federal EIN application: The first step is filing Form SS-4 with the IRS to obtain an EIN. This can be completed online in about 15 minutes, and the IRS issues the number immediately upon submission. The SS-4 confirmation letter is one of the most frequently requested documents in the acquisition process—banks need it to open accounts, credentialing specialists need it to enroll with insurance networks, and vendors need it to set up accounts. Save this document the moment you receive it.

State LLC or PLLC filing: Most states require dentists to form a Professional Limited Liability Company (PLLC) rather than a standard LLC, and many jurisdictions mandate dental board approval before the entity can be registered. Filing fees range from $100 in states like Kentucky to $800 in Massachusetts, with most falling in the $200–$500 range. Processing times vary significantly: expedited filings in states like Delaware or Nevada can be approved within 1–3 business days, while standard processing in California or New York can take 4–6 weeks. If your state requires dental board sign-off, add another 2–4 weeks to the timeline.

County and city registrations: After state approval, you'll need to register at the county level for a general business license and potentially at the city level for local permits. County business licenses typically cost $50–$200 and require proof of your state entity filing. City permits vary widely—some municipalities require health department inspections, zoning approvals, or occupancy permits before issuing a business license. These local filings are where buyers most often miss steps, particularly if they're working without legal guidance.

Fresh start entity vs. reusing an associate LLC: If you already operate an LLC as an associate, the instinct is often to reuse it for the acquisition. In most cases, that creates more problems than it solves. Lenders prefer clean entity structures with no legacy liabilities, and reusing an existing LLC means the bank has to review everything that entity has ever done—past contracts, prior debts, tax filings, and any potential claims. One pattern that tends to surface during underwriting is when an associate LLC has been used for side income, consulting work, or other ventures unrelated to clinical dentistry. That muddies the financial picture and can delay loan approval.

Working with a dental-specific attorney—typically $500–$1,000 for entity formation—ensures you complete all required registrations and avoid missing county or city-level filings that can delay closing.

Lenders and Insurance Credentialing Drive the Real Deadline

The practical deadline for entity formation isn't the LOI signing—it's the point where your lender needs documentation to finalize underwriting and where insurance companies need your entity information to begin credentialing. These two dependencies determine when you must have your LLC or PLLC fully registered, and both operate on timelines that work backward from your closing date.

Lender underwriting requirements: Most dental practice lenders require entity formation documents 30–45 days before closing to complete their underwriting process and finalize loan terms. The bank needs your Articles of Organization, Operating Agreement, EIN confirmation letter, and often a corporate resolution authorizing the entity to borrow. Where buyers often miscalculate is assuming they can form the entity a week before closing and hand the bank fresh documents—by that point, underwriting is already complete, and introducing a new entity structure forces the lender to restart portions of their review.

Insurance credentialing timelines: Insurance credentialing takes 60–90 days on average and cannot begin until you have an EIN and entity formation documents. Every major carrier—Delta Dental, Cigna, Aetna, MetLife—requires proof of your business entity, your National Provider Identifier (NPI) number, and your state dental license before processing credentialing applications. The credentialing process is tied to the individual dentist at a specific location, which means even if you're already credentialed as an associate at a different practice, you must re-credential at the practice you're buying.

The revenue gap problem: Closing before credentialing is complete creates a period where you own the practice but can't bill insurance under your provider number. Patients who arrive expecting in-network coverage are suddenly facing out-of-network rates, which can mean 30–50% higher out-of-pocket costs. Many patients will delay treatment, seek care elsewhere, or express frustration that their insurance "doesn't work anymore"—even though the practice has been in-network for years.

One protection many buyers build in is starting credentialing applications during due diligence, immediately after the LOI is signed. This requires forming your entity earlier in the process—typically 90–120 days before closing rather than 30–45 days—but it minimizes the gap between closing and when you can begin billing insurance. Credentialing specialists can submit applications in parallel across multiple carriers, but the process still requires your entity to be fully registered before any applications can be filed.

Seller transition billing arrangements: The seller staying on as a transition associate can allow continued billing under their provider number, but this arrangement must be negotiated in the purchase agreement and structured carefully. The seller must remain the treating dentist for claims billed under their number—you can't perform the work and bill under their credentials. When evaluating seller transition support, the credentialing gap is one of the strongest arguments for structured, compensated transition time rather than a quick handoff.

Where buyers get burned is assuming credentialing is automatic or that the practice's existing in-network status somehow transfers with the sale. It doesn't. Every insurance relationship must be re-established under your name, at your location, with your entity information.

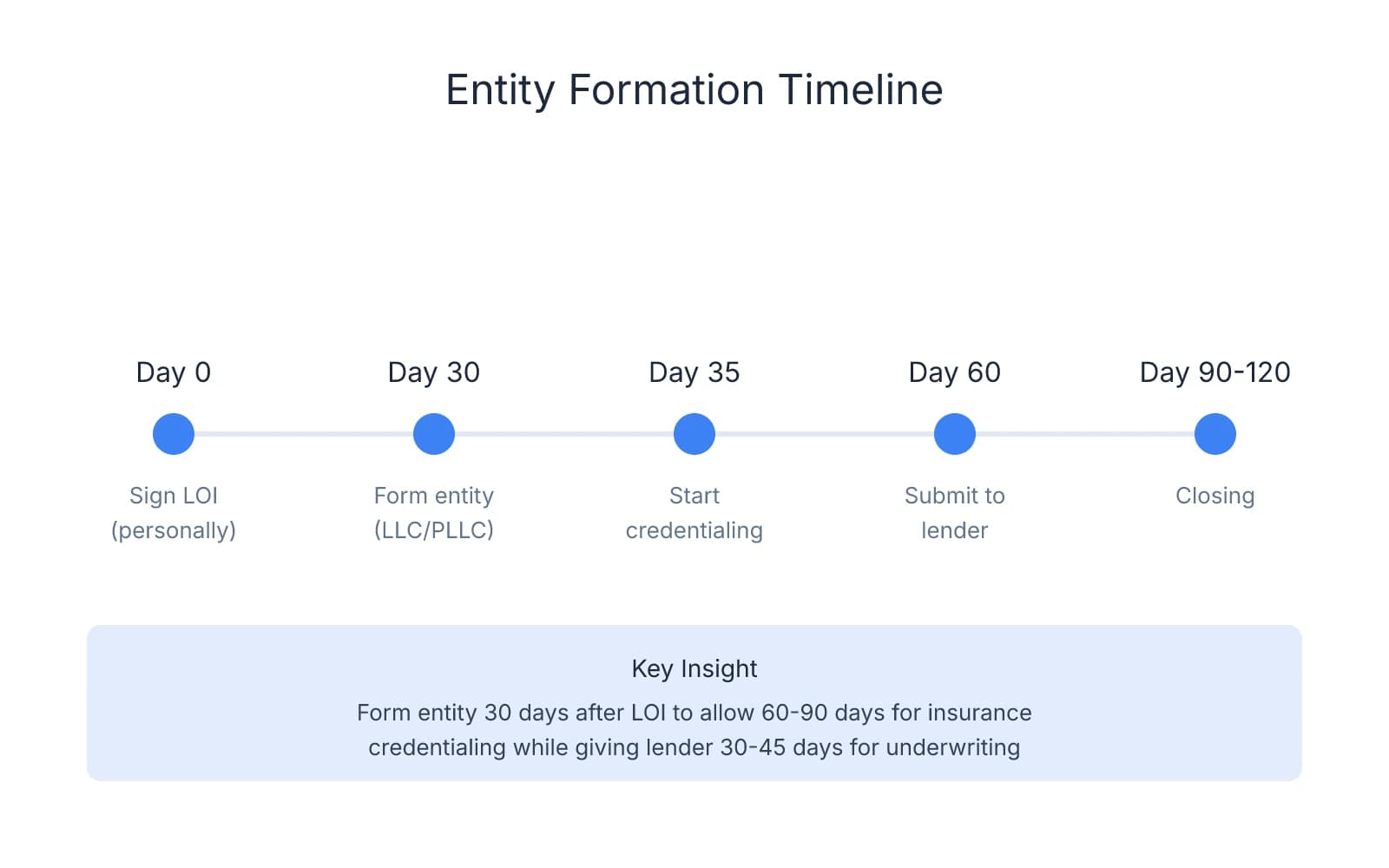

The Optimal Timeline: Form Your Entity Within 30 Days of LOI Signing

The sequence that protects both your closing timeline and your revenue stream is straightforward: sign the LOI personally, form your entity within 30 days, begin credentialing immediately, and provide complete entity documentation to your lender 30–45 days before closing. This cadence gives you enough runway to complete insurance credentialing before you take ownership while keeping entity formation costs contained to the period when you have a committed deal.

The standard timeline: For most acquisitions with a 90–120 day due diligence period, forming your entity 30 days after LOI signing aligns all three critical processes—lender underwriting, insurance credentialing, and state registration. You'll have your EIN and Articles of Organization in hand 60–90 days before closing, which gives credentialing specialists time to submit applications across all major carriers and gives your lender the documentation they need to finalize loan terms.

When to form earlier: If you're actively shopping multiple practices or expect a 120+ day due diligence period, forming your entity slightly earlier can streamline the process. A buyer evaluating three practices simultaneously might form an entity with a neutral name (e.g., "Smith Dental Group, PLLC" rather than "Riverside Family Dentistry, PLLC") that can be used regardless of which practice they ultimately acquire. This approach works best when you're confident you'll close on something within the next 6–9 months. The tradeoff is paying annual fees and registered agent costs during the period you're still shopping, which typically runs $300–$500 depending on your state.

If the deal falls through: A pattern worth paying attention to is what happens to your entity if the transaction doesn't close. In most states, you can reuse the entity for another acquisition as long as the name and structure still fit. If the entity name is specific to a practice you're no longer buying, most states allow dissolution with minimal fees if no business activity occurred—typically $50–$150 and a simple filing confirming the entity never operated.

State processing delays: Where buyers often get burned is underestimating how long state approval takes, particularly in jurisdictions like Florida or California where standard processing runs 4–6 weeks. If your closing timeline is tight—say, 60 days from LOI to closing—you'll need to file for expedited processing (typically an additional $100–$300) to ensure your entity is approved before credentialing deadlines hit. States that require dental board sign-off add another 2–4 weeks to the timeline.

Coordinating with your team: The entity formation process works best when your attorney, lender, and credentialing specialist are aligned on the same timeline. Your attorney handles the state filings and drafts your Operating Agreement. Your lender needs the EIN confirmation letter, Articles of Organization, and corporate resolution 30–45 days before closing. Your credentialing specialist needs those same documents plus your NPI number and dental license to begin insurance applications. One protection many buyers build in is sharing a single closing timeline document with all three parties—this keeps everyone working toward the same date and surfaces conflicts early.

Documents to gather before starting: Before you file for entity formation, collect your dental license, malpractice insurance certificate, NPI number, personal identification (driver's license or passport), and the practice address. Most states require proof of professional licensure before approving a PLLC, and credentialing applications won't move forward without current malpractice coverage. The NPI application itself takes 7–10 days if you don't already have one, so if you're a recent graduate without an NPI, factor that into your timeline.

The buyers who navigate entity formation most smoothly are the ones who treat it as a coordinated project with clear dependencies rather than a standalone legal task. When your attorney, lender, and credentialing specialist are working from the same timeline and you've gathered required documents upfront, the 30-day post-LOI window gives you enough runway to complete state filings, begin insurance credentialing, and provide your lender with everything they need—without paying for an entity you might not use or scrambling to meet deadlines two weeks before closing.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Business Formation for Dental Practices in Los Angeles— polishedlegal.com

- LLC for a Dental Practice: 7 Steps, Costs, and Benefits | ZenBusiness— zenbusiness.comIndustry

- The Hidden Challenge in Dental Practice Transitions — Insurance ...— ameriprac.comIndustry

- Credentialing for Dental Practice Insurance— www.dentalbuyeradvocates.comIndustry

Frequently Asked Questions

Ready to structure your practice acquisition?

Forming the right entity is just one piece of the puzzle when acquiring a dental practice. Minty Plus provides comprehensive guidance on entity formation, financing, and negotiation strategy to set you up for success from offer to close.