What is a Realistic Dental Loan Financing Timeline?

Co-Founder, Minty Dental

In Summary

- Specialized healthcare lenders often finance 90-100% of practice acquisitions for established dentists, requiring little to no down payment—far more accessible than most associates expect

- Student loan debt does not disqualify buyers from practice financing; lenders evaluate production capacity and debt-to-income ratios, not total debt burden

- Three main lender categories serve dental buyers: specialized healthcare banks (fastest approval, best terms), SBA lenders (flexible for newer associates), and conventional banks (competitive rates for strong borrowers)

- Pre-approval before finding a practice makes offers more competitive in multiple-bid situations and clarifies realistic purchase price ranges

- The 2-4 month financing timeline means buyers who start lender conversations early can move decisively when the right practice appears

Specialized Dental Lenders Offer Better Terms Than Most Buyers Realize

Most associates assume practice financing requires a massive down payment and flawless credit. The reality is more buyer-friendly. Specialized healthcare lenders—banks that focus exclusively on medical and dental professionals—understand the cash flow patterns of dental practices and structure loans accordingly. Many established associates qualify for 90-100% financing on practice acquisitions, meaning zero to 10% down in many cases.

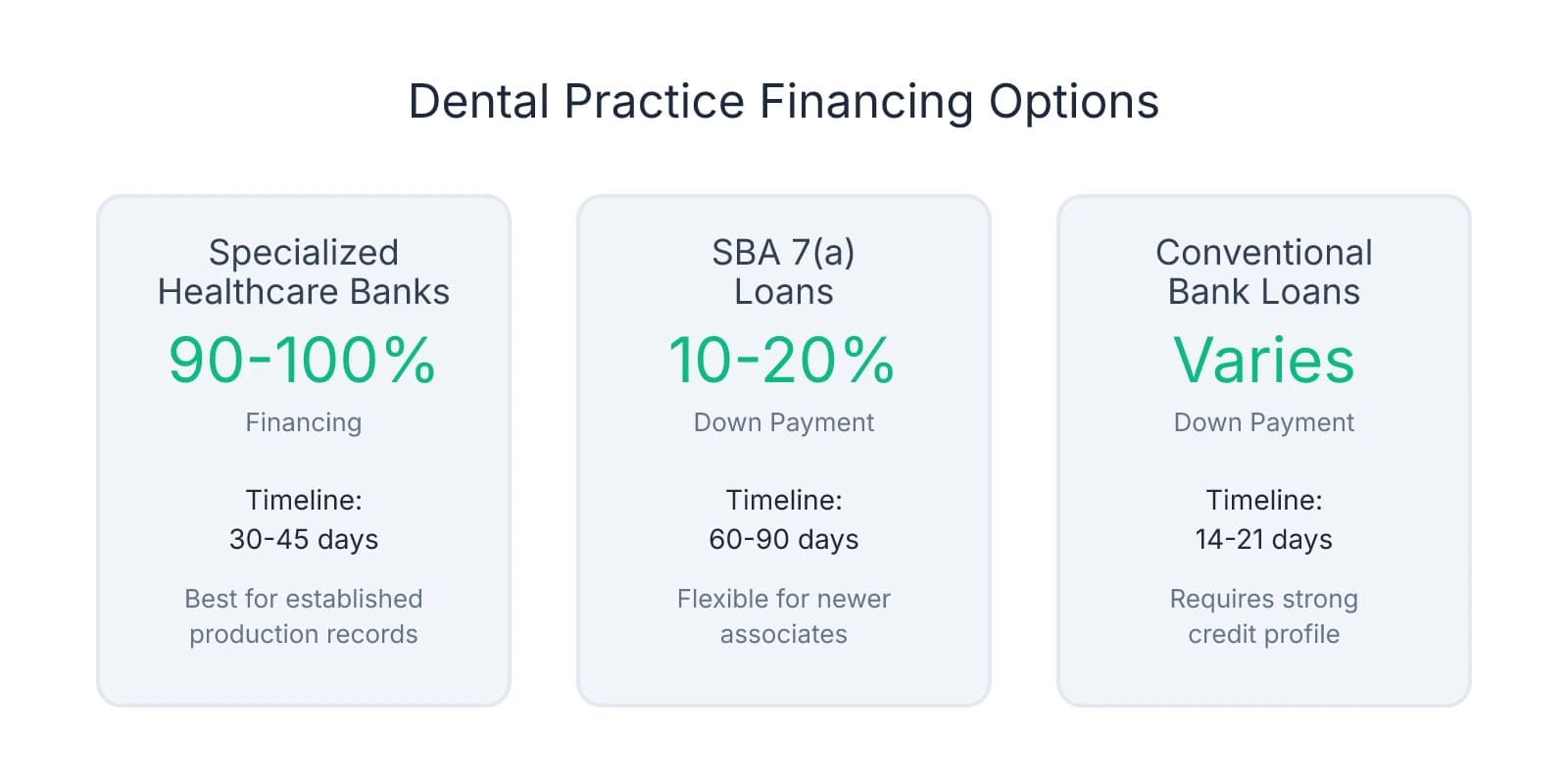

Three lender categories dominate the dental acquisition market, each with distinct advantages. Specialized healthcare banks like Bank of America Practice Solutions, Wells Fargo Practice Finance, and US Bank Healthcare move quickly and offer the most favorable terms for buyers with established production records. These lenders view dentists as low-risk borrowers because practice revenue is predictable and default rates are historically low. SBA 7(a) loans typically require 10-20% down and involve more documentation, but they work well for buyers with shorter production histories or lower liquidity. Conventional bank loans move faster—often 2-3 weeks versus 2-3 months for SBA—but require stronger credit profiles and demonstrated production capacity.

One pattern many first-time buyers miss: starting lender conversations before finding a practice creates a competitive advantage. A pre-approval letter signals to sellers that you're a serious buyer with financing already lined up, which matters in multiple-bid situations. It also clarifies your realistic purchase price range, so you're not wasting time on practices you can't afford or underestimating what you qualify for.

The most common misconception? That student loan debt disqualifies you. It doesn't. The average 2018 dental graduate carried $285,184 in student loans, yet many still qualify for practice financing. Lenders evaluate debt-to-income ratios and production capacity, not just total debt. If your production history shows you can service both student loans and a practice loan while maintaining reasonable cash flow, the debt becomes manageable risk rather than a disqualifier.

Where buyers often get burned is waiting until they've found a practice to explore financing. By then, you're racing against seller timelines and competing buyers who already have pre-approval. The smarter sequence: talk to 2-3 lenders early, understand what you qualify for, then search for practices within that range. Understanding different financing structures early also helps when evaluating whether a particular practice fits your financial profile—some deals work better with SBA terms, others with conventional loans.

What Lenders Actually Evaluate (And How to Prepare for Each Requirement)

With financing options clearer, the next question becomes: what do lenders actually look for? Four criteria drive most approval decisions: credit score, production history, debt service coverage ratio, and liquidity reserves. Each one measures a different dimension of financial readiness, and buyers who prepare for all four position themselves as low-risk borrowers before they ever submit an application.

Credit score is the first filter. Most dental lenders use 680 as the minimum threshold, though specialized healthcare banks may approve borrowers in the 650-680 range if production history is strong. Buyers below 680 should focus on credit repair before applying—paying down revolving balances, disputing errors on credit reports, and avoiding new credit inquiries. Pull your credit report 6-12 months before you plan to apply, so you have time to address issues rather than discovering them during underwriting.

Production history proves earning capacity. Lenders want to see consistent monthly production reports showing you can generate enough revenue to cover loan payments, operating expenses, and your own compensation. Most require 2-3 years of associate production data, though some accept shorter histories if the numbers are strong. If you're working as an associate, request monthly production reports from your current employer and keep them organized. These reports become the foundation of your loan application.

Debt service coverage ratio (DSCR) measures whether the practice generates enough income to cover the loan. Most lenders require a DSCR of 1.25x or higher, meaning the practice produces 25% more income than needed to service the debt. A practice generating $600,000 in annual collections with $400,000 in operating expenses leaves $200,000 for debt service and owner compensation. If the annual loan payment is $120,000, the DSCR is 1.67x—well above the threshold. Buyers can calculate this before applying by reviewing the seller's profit and loss statements and estimating their own production capacity.

Liquidity requirements vary by lender but typically range from 5-10% of the loan amount in accessible cash or assets. A $500,000 loan might require $25,000-$50,000 in reserves. This doesn't mean you need that much for a down payment—many buyers finance 90-100% of the purchase price—but lenders want to see you have cash cushion for unexpected expenses during the transition. Retirement accounts, savings, and investment portfolios all count toward liquidity, though some lenders discount illiquid assets.

Documentation requirements are straightforward but time-consuming to assemble. Expect to provide 2-3 years of personal tax returns, a personal financial statement listing all assets and liabilities, production reports from your current employer, a resume or CV, and either a business plan for startups or the seller's practice financials for acquisitions. Tax returns may need to be requested from an accountant, production reports from an employer, financial statements from the seller. Starting this process 60-90 days before you plan to apply keeps you from scrambling when a practice appears.

One pattern worth paying attention to: lenders evaluate the practice's financial health as closely as yours. If the seller's collections have been declining, or if the practice carries significant deferred maintenance, that affects your approval even if your personal financials are strong. This is why understanding what to look for in a practice's financials matters before you apply for financing—a lender may decline a loan not because you're unqualified, but because the practice itself is too risky.

The 2-4 Month Financing Timeline (And Where Delays Actually Happen)

Once you understand what lenders evaluate, the next consideration is timing. Most buyers underestimate how long financing takes, which creates unnecessary pressure when they find a practice they want. The full timeline from initial lender contact to loan closing typically runs 6-12 weeks for conventional loans and 8-16 weeks for SBA loans. Breaking this into phases helps buyers understand where time gets spent—and where delays most often occur.

Pre-approval happens first and moves quickly. Initial lender conversations, a credit check, and preliminary documentation review usually take 1-2 weeks. The output is a pre-approval letter stating how much you qualify to borrow and under what general terms. This letter doesn't commit the lender to funding a specific deal, but it signals to sellers that you're a credible buyer with financing capacity. Many buyers skip this step and go straight to formal applications once they find a practice, which adds weeks to the timeline and weakens their negotiating position in competitive situations.

The formal application and underwriting phase is where most time gets consumed. Once you've identified a practice and submitted a purchase agreement, the lender begins detailed financial review. This includes ordering a practice appraisal, analyzing the seller's tax returns and profit-loss statements, verifying your production history, and calculating debt service coverage. Conventional loans typically complete this phase in 2-4 weeks. SBA loans add 4-8 weeks because the Small Business Administration must review and approve the loan package after the bank completes its own underwriting. The average SBA 7(a) loan takes 60-90 days from application to closing, compared to 30-45 days for conventional dental practice loans.

Due diligence runs parallel to underwriting and creates the most common delay point. While the lender completes its review, you're conducting your own financial and operational analysis of the practice. This phase typically takes 2-4 weeks, but it stretches longer when seller records are disorganized. Missing tax returns, incomplete patient charts, unclear lease terms, or undocumented equipment maintenance all slow the process. One protection many buyers overlook is requesting organized financials before signing a letter of intent—if the seller can't produce clean records during initial conversations, expect delays during due diligence.

Final approval and closing is the shortest phase if earlier steps went smoothly. Loan documents are prepared, final conditions are cleared, and funds are disbursed at closing. This usually takes 1-2 weeks, though it can extend if title issues surface or if the seller's attorney introduces last-minute contract changes. Lenders can still pull funding if something material changes between approval and closing, such as a significant drop in practice collections or an undisclosed liability.

The pattern that separates smooth closings from delayed ones is early preparation. Buyers who start lender conversations 3-6 months before they plan to purchase—well before they've identified a specific practice—move through the timeline faster because documentation is already assembled, credit issues are resolved, and pre-approval is in hand. Those who wait until they've found a practice and then scramble to secure financing often discover they're racing against seller deadlines or competing with buyers who already have financing lined up. Understanding the full acquisition timeline helps buyers sequence financing appropriately rather than treating it as a last-minute task.

One variable worth tracking: appraisal timelines vary by region and appraiser availability. In markets with few dental practice appraisers, scheduling can add 2-3 weeks to the process. Buyers in rural areas or smaller markets should ask lenders upfront how long appraisals typically take in their region, since this is one delay point that's largely outside your control once the process starts.

Building Your Financing Strategy Before You Need It

Understanding the timeline makes one thing clear: the strongest buyers start financing conversations 6-12 months before they actively search for practices. This creates space to address credit issues, build liquidity, and establish relationships with multiple lenders—advantages that matter when you're competing against other buyers or negotiating with sellers who want a fast close.

One step many buyers find valuable is interviewing 2-3 lenders early to compare down payment requirements, interest rates, loan terms, and timeline expectations. Specialized dental lenders often offer better terms than general business banks because they understand practice cash flow patterns and view dentists as low-risk borrowers. Many established associates qualify for 90-100% financing on practice acquisitions, meaning zero to 10% down in many cases. SBA 7(a) loans typically require 10-20% down and involve more documentation, but they work well for buyers with shorter production histories. Conventional dental practice loans move faster—often 30-45 days versus 60-90 days for SBA—but require stronger credit profiles and demonstrated production capacity.

Set up a folder now for tax returns, production reports, financial statements, and practice information so you can respond quickly when lenders request materials. Most lenders need 2-3 years of personal tax returns, a personal financial statement, production reports from your current employer, and either a business plan for startups or the seller's financials for acquisitions.

Getting pre-approved before making offers creates a competitive advantage in multiple-bid situations. A pre-approval letter shows sellers you're a serious buyer with financing already lined up, which matters when they're choosing between similar offers. It also clarifies your realistic purchase price range, so you're not wasting time on practices you can't afford or underestimating what you qualify for. Understanding what questions to ask sellers becomes more productive when you already know what you can finance.

The financing process is predictable when you prepare early. Buyers who wait until they find a practice often face delays, lose deals to faster competitors, or settle for less favorable loan terms because they're rushing to close. Those who start lender conversations months in advance move through the 2-4 month timeline more smoothly because documentation is assembled, credit issues are resolved, and they've already compared multiple lenders. The difference between a buyer who closes in 45 days and one who takes 90 isn't luck—it's preparation that happened long before the practice appeared.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Demystifying the Practice Loan Process | American Dental Association— ada.orgIndustry

- The average SBA 7(a) loan takes 60-90 days from application to closing— sba.gov

- How Much Down Payment Do You Need for a Dental Office Loan?— dentalcpausa.comIndustry

Frequently Asked Questions

Ready to Finance Your Dental Practice?

Understanding the financing process is just the first step. Minty Plus connects you with experienced advisors who guide you through every stage of practice acquisition, from securing the right loan to closing the deal and beyond.