How Much Money Do You Actually Need Saved to Buy a Dental Practice?

Co-Founder, Minty Dental

In Summary

- Most dental practice lenders finance 100% of the purchase price but require 10% of the loan amount in liquid assets—money that stays in your account as a safety buffer, not a down payment

- Actual out-of-pocket costs at closing run $15,000–$20,000 for legal fees, appraisals, and inspections, while the liquidity requirement protects against unexpected expenses like equipment failures or slow collections

- Qualifying liquidity includes savings, checking, and taxable brokerage accounts—but excludes retirement accounts, home equity, and other restricted assets that can't be accessed quickly without penalties

- High-producing associates ($400,000+ annually) or buyers with exceptionally stable practices may negotiate reduced liquidity requirements, sometimes as low as 5–7%

- Most buyers build the required liquidity over 2–3 years through aggressive saving as associates, often supplemented by family gifts or maintaining part-time associate work during the first year of ownership

The 10% Liquidity Requirement Is Not a Down Payment

The single biggest misconception delaying first-time buyers is treating the 10% liquidity requirement as a down payment. Most dental practice lenders finance 100% of the purchase price. The 10% they require sits in your account as a safety buffer—you keep it, you don't spend it.

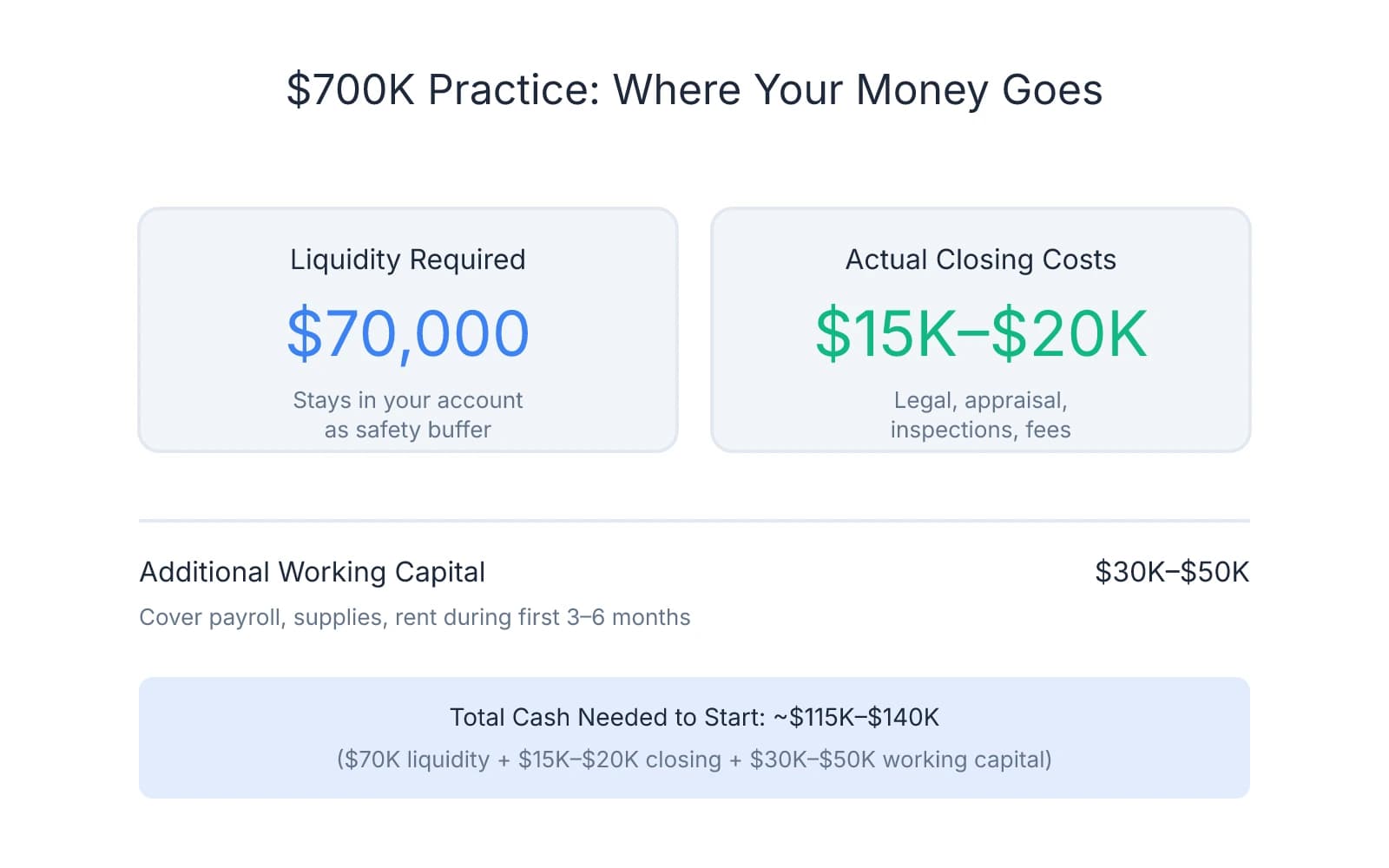

For a $700,000 practice, most lenders want to see $70,000 in liquid assets before approving the loan. That $70,000 doesn't fund the purchase—it stays in your checking, brokerage, or retirement account. The lender wants proof you can weather the first six months if collections slow, a hygienist quits, or the autoclave dies.

Liquidity demonstrates cash reserves, not equity contribution. Many buyers assume they need to save $70,000 to "afford" a $700,000 practice, when they actually need to have $70,000 accessible while spending far less at closing. Actual out-of-pocket costs—legal fees, appraisals, inspections, entity formation—typically run $15,000–$20,000.

The first 90 days are where deals go sideways. A practice collecting $60,000 monthly under the seller might drop to $45,000 while you're learning patient names and rebuilding trust. Without reserves, a single bad month can spiral into missed loan payments. The 10% threshold gives lenders confidence you can absorb that volatility.

Buyers with strong production histories or exceptionally clean deals sometimes negotiate flexibility on the 10% figure. If you're producing $800,000 annually as an associate and buying a $600,000 practice, some lenders accept 7–8% liquidity. But that's the exception—most hold firm on the benchmark.

The liquidity requirement also explains why many buyers with $400,000 in student loans can still purchase practices—the debt-to-income ratio matters more than absolute debt, and as long as you've maintained 10% liquidity alongside those loans, lenders move forward.

For a $500,000 practice, that's $50,000. For $800,000, it's $80,000. The number scales with deal size, but the principle stays the same: lenders want proof you can handle the unexpected without putting their loan at risk.

What Counts as Liquidity (and What Doesn't)

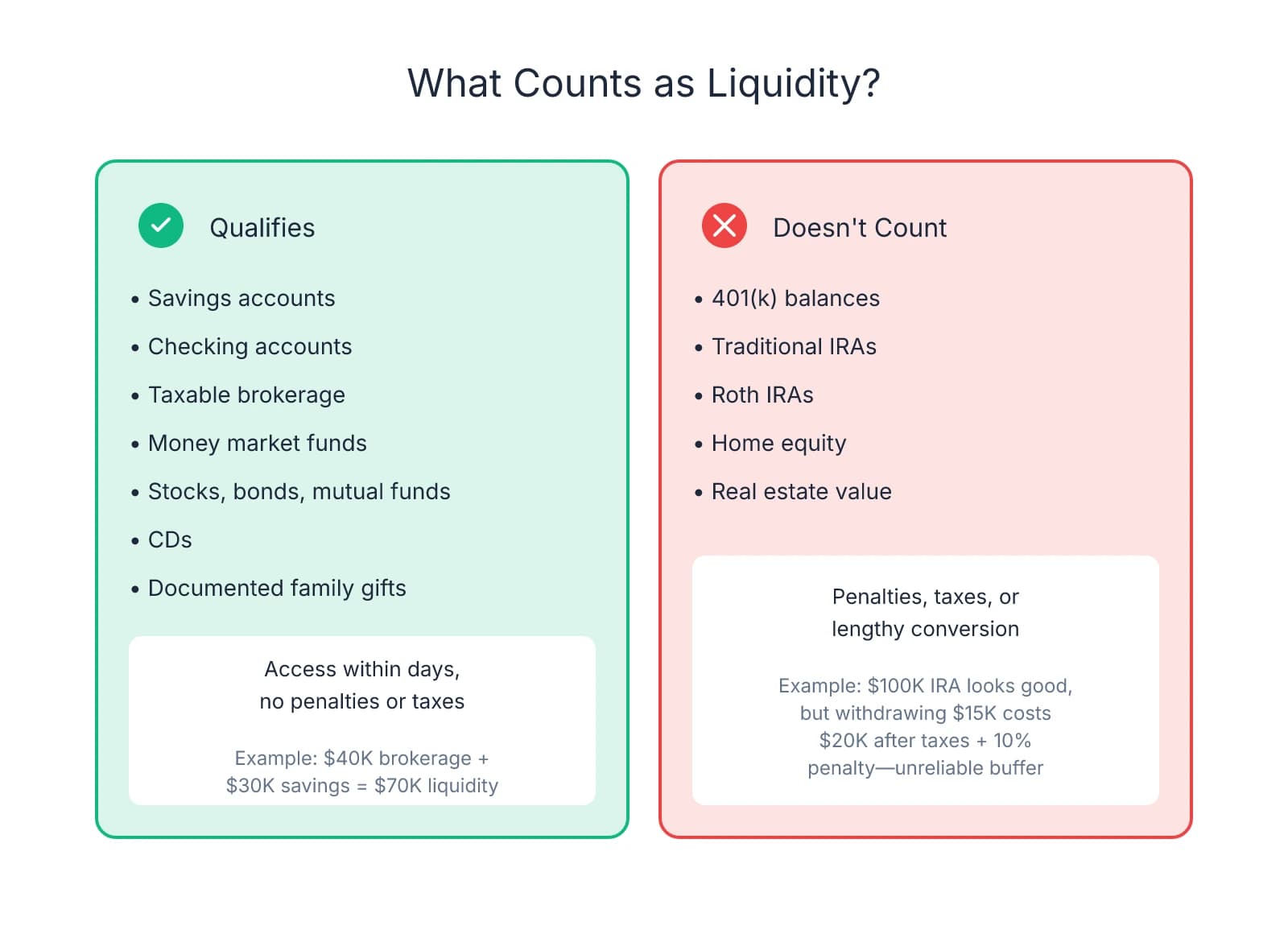

Lenders define liquidity narrowly: assets you can convert to cash within days without penalties or tax consequences. Many buyers assume their net worth qualifies, when lenders only care about what you can access in an emergency.

Qualifying liquidity includes: savings accounts, checking accounts, taxable brokerage accounts, money market funds, individual stocks, bonds, mutual funds, and certificates of deposit. If you hold $40,000 in a Vanguard taxable account and $30,000 in high-yield savings, you've got $70,000 in liquidity—enough for a $700,000 practice.

What doesn't count: 401(k) balances, traditional IRAs, Roth IRAs, and home equity. Lenders view these as restricted funds that trigger penalties if accessed early or require lengthy processes to convert. A $100,000 IRA looks impressive, but withdrawing $15,000 to cover payroll means paying income tax plus a 10% penalty—that $15,000 withdrawal costs you $20,000, making it unreliable as a safety buffer.

Home equity requires opening a HELOC or refinancing—processes taking weeks and depending on approval. Lenders want liquidity you can deploy immediately, not assets requiring secondary financing.

One exception: gifted funds from family members count as liquidity if documented correctly. If your parents gift you $50,000, that satisfies the requirement—but only with a signed gift letter stating the funds don't need repayment. Without documentation, lenders treat the $50,000 as additional debt and adjust your debt-to-income ratio, potentially killing approval.

When collections drop 20% in your second month because hygiene patients rescheduled and a crown case fell through, lenders want to know you can cover the gap without scrambling. Taxable accounts let you sell shares and transfer cash the same week. Retirement accounts don't.

Buyers often conflate assets with liquidity. You might have $200,000 in total assets—$60,000 in a 401(k), $80,000 in home equity, $40,000 in a brokerage account, and $20,000 in savings—but only $60,000 qualifies as liquidity. For a $600,000 practice, you're still $10,000 short of the 10% threshold despite a strong balance sheet.

The practical takeaway: structure savings with liquidity in mind. If you're three years from buying and contributing heavily to a 401(k), consider shifting some contribution to a taxable brokerage account. Tax advantages matter, but not if they delay ownership by two years because you can't meet the liquidity requirement when the right deal appears.

When Lenders Reduce or Waive the 10% Threshold

The 10% liquidity requirement isn't fixed. When your financial profile or the practice's fundamentals reduce lender exposure, they'll negotiate.

High-producing associates earning $400,000+ annually often qualify for reduced liquidity requirements—sometimes as low as 5%, occasionally waived entirely. If you're generating $35,000 monthly in production as an associate and buying a $600,000 practice, the lender's default risk drops significantly. Your income history demonstrates repayment capacity independent of the practice's performance. Associates producing at this level often get approved with $30,000–$40,000 in liquidity on deals where the standard threshold would require $60,000–$70,000.

This flexibility extends beyond income level—it's about income relative to practice size. An associate earning $300,000 buying a $400,000 practice has more leverage than someone earning $500,000 buying a $1.2 million practice. Lenders evaluate whether your production can carry debt service comfortably.

Practices with rock-solid financials also trigger flexibility. When you're buying a practice with five years of consistent collections, overhead below 60%, minimal staff turnover, and stable patient base with low attrition, the lender's risk profile shifts. Where a typical deal requires 10% liquidity, a practice with exceptionally clean financials might get approved at 7–8%—or in rare cases, with no liquidity requirement if the buyer's production history is strong enough.

The inverse matters: practices with volatile collections, high overhead, or recent patient attrition see lenders hold firm on 10% regardless of your income. If the practice introduces risk, lenders won't reduce the buffer.

Debt-to-income ratio matters more than student loan balance. Many buyers assume $400,000 in student debt disqualifies them from flexibility, but lenders evaluate whether your income can service all debt obligations. If you're earning $350,000 annually with $400,000 in student loans on an income-driven repayment plan capped at $1,500 monthly, your debt-to-income ratio might sit at 25–30% even after adding the practice loan. The same buyer earning $200,000 would face a 40–45% ratio, limiting flexibility. The debt load isn't the issue—it's the relationship between income and total monthly obligations.

Credit score above 700 strengthens your position for negotiating reduced liquidity requirements. Scores between 650–700 are workable but rarely unlock flexibility. Below 650, most lenders hold firm on 10% regardless of income or practice quality. If your credit score is under 680, the chances of obtaining financing are slim.

Flexibility appears most often when a high-producing associate with a 720+ credit score buys a practice with stable financials in a market the lender knows well. That combination—strong borrower, strong practice, strong market—gives you leverage. The same buyer purchasing a practice with inconsistent collections or in a rural market the lender views as higher risk faces the standard 10% requirement.

If you're producing $400,000+ annually, buying a practice with clean financials, and carrying a credit score above 700, ask your lender directly whether they'll reduce the liquidity threshold. Many buyers never ask and assume the 10% figure is non-negotiable. It's not—but flexibility only appears when your profile reduces the lender's risk enough to justify it.

What You'll Actually Spend at Closing (and Where Buyers Get the Money)

You need $70,000 in the bank to buy a $700,000 practice, but you're not writing a $70,000 check at closing. The real out-of-pocket number sits closer to $15,000–$20,000.

Actual closing costs break down into five categories: earnest money deposit (typically $5,000–$10,000, which goes toward the purchase), attorney fees for contract review and entity formation ($3,000–$5,000), practice appraisal ($2,000–$4,000), environmental and equipment inspections ($1,000–$2,000), and loan origination fees if your lender charges them (0.5–1% of the loan amount, though many dental-specific lenders waive this).

The earnest money deposit gets credited toward the purchase price at closing—it's part of the transaction, not an additional expense. The risk is forfeiting the deposit if you walk away without a valid contingency (failed inspection, financing denial, undisclosed liabilities).

Beyond closing costs, working capital sits as the larger financial consideration. Plan for $30,000–$50,000 to cover payroll, supply orders, and rent during the first 3–6 months while stabilizing collections. Insurance reimbursements lag 30–60 days. Staff payroll hits every two weeks. Lab bills come due before the crowns you're placing generate revenue. Some lenders include this in your loan package as a lump sum or line of credit. Others expect you to fund it separately.

Most buyers build liquidity intentionally over 2–3 years. The most common path is working as an associate producing $200,000–$400,000 annually and saving aggressively. If you're netting $150,000 per year after taxes and living expenses and banking $30,000–$40,000 annually, you'll hit the $70,000 threshold in two years.

Three liquidity cushions show up repeatedly: significant cash savings built through associate work, a working spouse whose income covers household expenses while you're ramping up, or maintaining a part-time associate position during your first year of ownership. Many buyers work three days in their own practice and two days as an associate elsewhere during the first 6–12 months, removing financial pressure while building patient relationships.

Family gifts count as liquidity if documented correctly. If your parents gift you $40,000, that satisfies part of the requirement—but only with a signed letter stating the funds don't need repayment and won't create a future financial obligation. Without documentation, lenders treat the $40,000 as debt and adjust your debt-to-income ratio, potentially derailing approval.

The first 90 days bring unexpected expenses—a staff member who quits and needs replacing, an insurance credentialing delay pushing reimbursements back another month, a compressor that fails and costs $8,000 to replace. If you've allocated every dollar of your liquidity to closing costs and working capital, you've got no buffer. That's why the 10% threshold exists: it's not just about covering payroll—it's about absorbing volatility without triggering a financial crisis.

Buyers who start with $50,000 in liquidity instead of $70,000 often make it work by structuring deals creatively. They target smaller practices ($500,000 instead of $700,000), negotiate seller financing for part of the purchase to reduce the loan amount, or find lenders willing to accept 7–8% liquidity based on strong production history.

If you're starting from scratch, the timeline depends on how aggressively you save. An associate earning $250,000 and saving $40,000 annually will hit $80,000 in liquidity in two years. Someone earning $180,000 and saving $25,000 annually will take three years to reach $75,000. Most buyers who successfully transition to ownership automate transfers to a separate account every month and live on what's left, rather than saving whatever remains after spending.

You need $70,000 accessible to buy a $700,000 practice, but only $15,000–$20,000 leaves your account at closing. The rest sits as a safety buffer for the first six months. If you're two years away from that threshold, start building liquidity now. If you're already there, the path to ownership is shorter than you think.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Credit and Liquidity Tips for Dental Practice Buyers— www.menlotransitions.com

- 5 Financial Must-Dos Before Buying a Dental Practice— www.ada.orgIndustry

- How to Buy a Dental Practice: The Complete 2026 Guide— www.integritypracticesales.com

Frequently Asked Questions

Ready to turn savings into practice ownership?

Now that you understand the financial requirements for buying a dental practice, explore available practices that match your budget or get personalized guidance on structuring your acquisition.