When Your Landlord Won't Assign the Lease in a Dental Practice Sale

Co-Founder, Minty Dental

In Summary

- Most dental practices operate from leased space, and without the ability to transfer that lease to a buyer, the practice has no physical location—making it essentially worthless

- Lenders typically require 5-7 years of remaining lease term to approve financing, meaning a lease expiring in 2-3 years can block the entire transaction

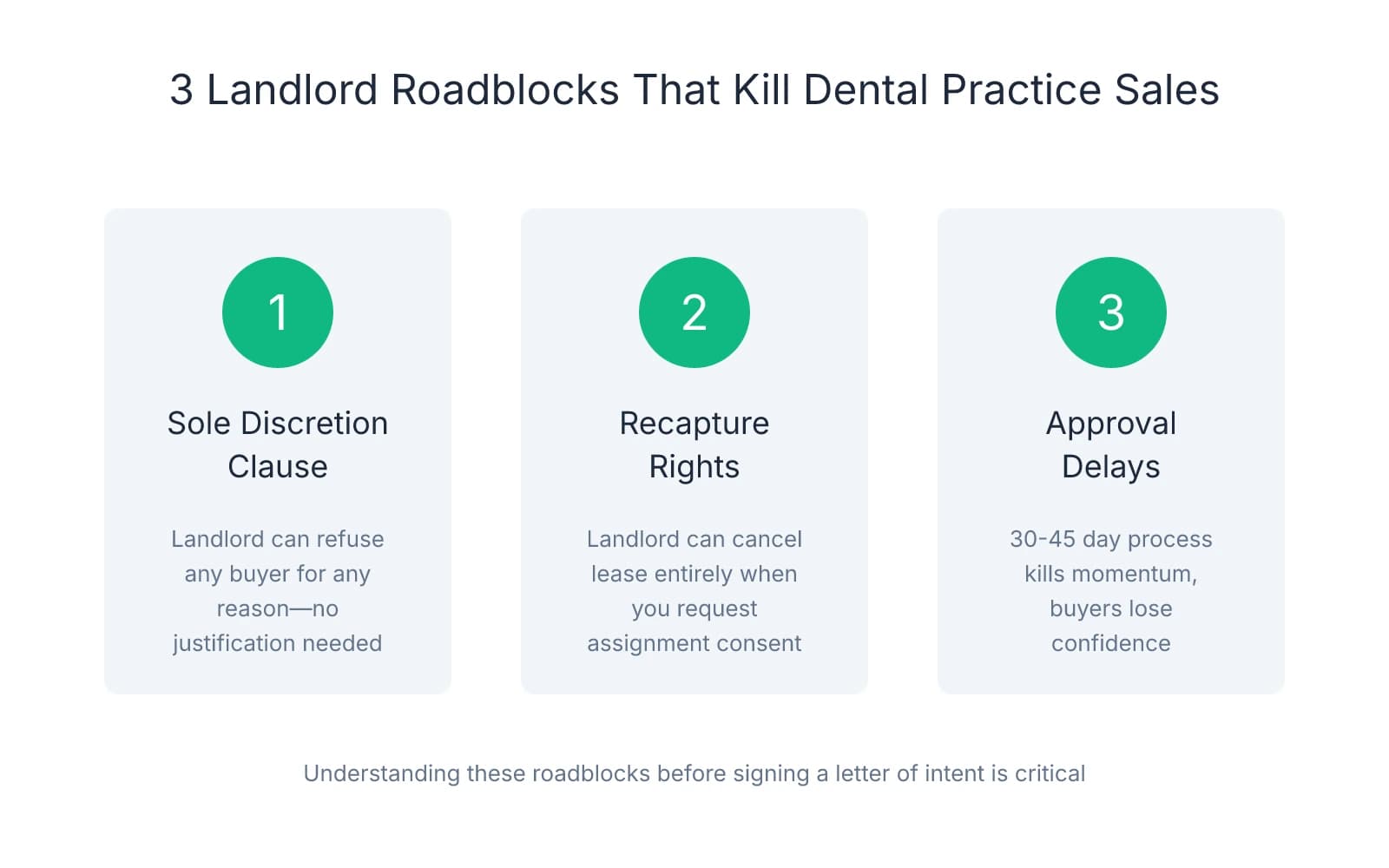

- Three common landlord roadblocks derail deals: 'sole discretion' assignment clauses that give landlords unlimited veto power, recapture rights that let them cancel the lease entirely when you ask for consent, and approval delays that stretch weeks or months while buyers lose confidence

- Location matters more in dental than most businesses because patient goodwill is tied directly to the physical address—patients won't follow a practice that relocates

Lease Assignment Refusals Can Kill Deals Before They Start

A dental practice without a transferable lease is a business without a location. You can have clean financials, loyal patients, and modern equipment, but if the buyer can't secure the space where those patients expect care, the deal collapses.

Lease assignment transfers the seller's leasehold interest to the buyer, along with the rights and obligations under the existing lease. For buyers, this continuity is non-negotiable. The practice's value is built on patient relationships tied to a specific address. Relocating after closing means losing a portion of that goodwill—patients who won't follow, staff who can't commute, and referral networks that evaporate. Lenders understand this risk, which is why most dental practice lenders require 5-7 years of remaining lease term (including renewal options) before they'll approve financing. A lease expiring in two years doesn't meet that threshold, and without financing, most buyers can't proceed.

Three landlord roadblocks appear repeatedly. The first is the "sole discretion" assignment clause—language that gives the landlord unlimited authority to refuse any buyer, for any reason, without justification. The second is the recapture clause, which allows the landlord to cancel the lease entirely when you request assignment consent. Once you've asked, you can't un-ask. The landlord now holds leverage to demand payment in exchange for approval—or simply terminate the lease and leave you with a practice you can't sell. The third roadblock is delay. Even when a landlord eventually agrees to assignment, a 30-45 day approval process can kill momentum. Buyers lose confidence, lenders move on to other deals, and sellers watch their transaction fall apart over paperwork that should have taken a week.

Here's how this plays out. A buyer submits an offer, conducts due diligence, and secures preliminary loan approval. The lender issues a commitment letter contingent on lease assignment. The seller requests landlord consent. Weeks pass. The landlord asks for financial statements, credit reports, and personal guarantees from the buyer. The buyer's lender, unwilling to fund a deal with an uncertain lease, withdraws the commitment. The buyer walks away. The seller is left with a practice that's been off the market for two months and a landlord who may or may not cooperate with the next buyer.

This dynamic is more destructive in dental than in most other businesses because location is inseparable from value. A retail store can rebrand and relocate. A dental practice tied to a specific address loses patients the moment it moves. That's why understanding lease assignment risk before signing a letter of intent is one of the most important steps a buyer can take—and why sellers who ignore their lease terms until a deal is pending often discover they've been sitting on an unsellable asset.

What Assignment Clauses Actually Say—and Why 'Sole Discretion' Is a Red Flag

Most buyers scan the lease for rent and square footage, then move on. That's a mistake. The assignment clause determines whether you can actually complete the purchase—and the difference between landlord-friendly and tenant-friendly language can mean the difference between a smooth closing and a dead deal.

The most dangerous version reads: "Landlord may withhold consent to assignment in Landlord's sole and absolute discretion." This language gives the landlord unlimited authority to refuse any buyer, for any reason—or no reason at all. They can reject a buyer with perfect credit and 15 years of experience simply because they don't like the terms of the deal. They can demand a rent increase as the price of approval. The clause creates a veto power with no accountability.

The tenant-friendly alternative reads: "Landlord's consent to assignment shall not be unreasonably withheld, conditioned, or delayed." This sounds protective, and it's certainly better than sole discretion, but it still leaves significant room for landlord leverage. "Unreasonable" is a fact-specific standard, and the burden of proving unreasonableness falls on the tenant. Landlords can consider their own financial interests when evaluating a proposed assignee—meaning they can reject a buyer who doesn't meet their credit standards, even if that buyer would qualify for bank financing. They can condition approval on the seller remaining liable under the lease, or on the buyer providing a personal guarantee.

One pattern that surfaces repeatedly: landlords who agree to "reasonable consent" language but then delay the approval process for weeks. The lease says consent can't be unreasonably delayed, but what counts as unreasonable? Thirty days? Sixty? By the time you'd have grounds to challenge the delay, your buyer has likely moved on.

Recapture clauses create a different problem entirely. These provisions allow the landlord to terminate the lease instead of approving the assignment. The language typically reads: "Upon Tenant's request for consent to assign, Landlord may elect to recapture the Premises and terminate this Lease." Once you ask for consent, the landlord can cancel the lease, leaving the buyer without a location and you without a sale. The request itself triggers the landlord's right to recapture, and you can't withdraw it. This gives the landlord extraordinary leverage to extract payment—either a percentage of the sale price, a rent increase, or a lump sum—in exchange for waiving their recapture right.

Personal renewal options create a parallel risk. Many leases include extension options that are "personal to the original Tenant" and don't transfer to an assignee. If your lease expires in three years but includes two five-year renewal options, you might assume the buyer has 13 years of occupancy. But if those options are non-transferable, the buyer has three years—and most lenders won't approve a loan on a lease that short.

Before making an offer, pull three documents: the lease, any amendments, and any correspondence between the seller and landlord about a potential sale. Have your attorney review the assignment clause specifically. If the lease contains sole discretion language or a recapture clause, factor that into your offer structure. You may need to negotiate landlord consent as a condition precedent in the purchase agreement, or build in a longer due diligence period to address lease issues before you're financially committed. Discovering these clauses after signing a letter of intent leaves you negotiating from a position of weakness.

How to Assess Lease Risk Before You Make an Offer

The time to evaluate lease risk is before you're emotionally or financially committed to the deal—not after you've signed a letter of intent and your lender starts asking questions. One protection many buyers overlook is requesting the lease document during initial due diligence, before making an offer. Most sellers treat the lease as a formality and hand it over late in the process, but that sequencing creates risk.

Start by calculating the effective lease term: base term remaining plus renewal options you can actually exercise. If the lease expires in four years with two five-year renewal options, that looks like 14 years on paper. But if those renewal options are "personal to the original Tenant" and don't transfer to an assignee, your effective term is four years—not enough for most lenders. Pull the lease and check whether renewal language includes phrases like "Tenant or its permitted assigns" or "transferable to assignees." If the options are personal, you'll need the landlord's agreement to make them transferable, and that agreement typically comes with conditions.

The assignment clause language determines how much leverage the landlord holds. If it reads "Landlord may withhold consent in its sole discretion," you're operating in a high-risk scenario. If it reads "consent not to be unreasonably withheld," you have some protection, but the landlord can still condition approval on financial qualifications, personal guarantees, or the seller remaining liable. The safest version includes specific approval criteria—credit score thresholds, financial statement requirements, or industry experience standards—because that removes subjectivity from the process.

Check for recapture rights next. If the lease allows the landlord to terminate upon your request for assignment, you're handing them a veto power that can't be withdrawn. Many buyers discover this clause only after the seller has already approached the landlord, at which point the landlord holds all the leverage.

Personal guaranty requirements matter more than most buyers expect. Some leases require the buyer to provide a personal guaranty even if the seller's lease didn't include one, or they require the seller to remain liable after closing. If the seller stays on the hook, they'll likely demand a higher purchase price or refuse to close unless the landlord releases them.

Consent fees and profit-sharing provisions show up in some commercial leases, particularly in medical office buildings. The landlord may charge a flat fee for processing the assignment (typically $500–$2,000), or they may demand a percentage of the sale price as a condition of approval. One pattern worth paying attention to is landlords who agree to assignment but then delay the approval process for 30–45 days while they "review" the buyer's financials.

Request the lease document immediately after initial conversations with the seller, before you make an offer. Have your attorney review the assignment clause, recapture rights, and renewal options before you sign the letter of intent. Approaching the landlord comes later—after the LOI is signed and financing is arranged, but coordinated carefully to avoid violating confidentiality or spooking the landlord with a premature request.

When you identify a lease problem, you have four options. The first is to walk away—if the lease has sole discretion language, a recapture clause, and less than five years remaining, the risk may outweigh the opportunity. The second is to renegotiate the purchase price to account for lease risk. The third is to require the seller to amend the lease as a condition of closing. The fourth is to accept the risk and budget for a new lease negotiation post-closing—viable if the practice is in a tenant-friendly market, but risky if the landlord knows you have no alternative location. When deciding whether to proceed with a risky lease, weigh the practice's other strengths—patient base, revenue stability, equipment condition—against the likelihood of lease complications affecting your practice's value and your ability to expand, relocate, or sell within the first few years of ownership.

Structuring the Deal to Survive Landlord Interference

The best defense against landlord interference is building protection into the deal structure before you're committed. One step many buyers overlook is making the purchase agreement explicitly contingent on landlord consent to assignment—with a defined timeline and clear exit rights if consent doesn't arrive. The language should specify that the seller must obtain written landlord approval within 30-45 days of the effective date, and that if consent is denied, unreasonably delayed, or conditioned on terms unacceptable to the buyer, the buyer can terminate the agreement and receive a full refund of any deposit.

Where deals often go sideways is when the purchase agreement treats lease assignment as the buyer's responsibility. The seller signs the agreement, collects a deposit, and then tells the buyer to "work it out with the landlord." By that point, you're negotiating from weakness—the landlord knows you've already committed to the purchase, and they can extract concessions as the price of approval.

Clarify who pays for lease amendments, consent fees, and any required modifications. If the landlord demands a personal guarantee from the buyer that wasn't required under the seller's lease, or if they insist on a rent increase as a condition of assignment, those costs should fall on the seller—they're fixing a problem that existed before the sale. Many purchase agreements are silent on this point, which leads to disputes at closing when the landlord presents a $5,000 consent fee or requires the lease to be amended to remove favorable terms the seller negotiated years ago.

When assignment isn't possible—because the lease prohibits it, the landlord refuses, or the remaining term is too short—three alternative structures appear. The first is negotiating a new lease directly with the landlord. This takes longer, typically 60-90 days, and removes the benefit of inheriting the seller's favorable rent terms, but it gives you a clean lease with renewal options that transfer. Lenders often prefer a new lease over an assigned lease because it removes the risk of the seller's default history or undisclosed lease violations affecting your tenancy. The downside is cost—you'll likely pay market rent rather than the below-market rate the seller locked in five years ago.

The second option is having the seller remain as tenant and sublease the space to you. This keeps the existing lease in place and avoids the need for landlord consent to assignment, but it creates significant risk. The seller stays liable for rent, and if you default, the landlord can pursue them. Most sellers won't agree to this structure unless you're paying a premium to compensate for their ongoing liability. More importantly, many lenders won't approve financing on a subleased property because your occupancy rights are derivative—if the seller defaults on the master lease, your sublease terminates regardless of whether you've been paying rent.

The third option, relocating the practice, is expensive and threatens patient goodwill. Moving costs—tenant improvements, equipment relocation, new signage, updated marketing—can run $100,000 or more, and you'll lose a portion of your patient base in the process. Relocation is viable only when the practice's value isn't location-dependent—high-volume insurance practices with patients spread across a wide geographic area, or specialty practices where patients travel for care. For general practices in residential areas where proximity drives patient loyalty, relocation is a last resort.

Early landlord communication reduces these risks, but it must be done strategically. The seller or their broker should approach the landlord informally before the LOI is signed—not to request formal consent, which could trigger recapture rights, but to gauge cooperation and identify potential roadblocks. A simple conversation: "I'm considering selling the practice in the next 6-12 months. The lease has three years remaining. Would you be open to discussing assignment or a lease extension with a qualified buyer?" This signals intent without committing to a specific transaction, and the landlord's response tells you whether they'll cooperate or create obstacles.

The final decision point: knowing when to walk. If the landlord has absolute discretion under the lease, a documented history of blocking practice sales in the building, or demands a consent fee equal to 10-15% of the purchase price, the deal may not be worth the risk—especially if the practice's entire value is tied to that specific location. Lease risk is real, but it's manageable with the right due diligence, contract protections, and willingness to walk away from deals where the landlord holds too much power.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- How Lease Issues Can Slow Down—or Kill—Your Dental Practice ...— martilawgroup.com

- Assignment Clauses in Dental Office Leases: What Every Dentist ...— dentistryinsured.com

- A Practical Guide to Assignment Clauses in Commercial Leasing— aystrauss.com

- Dental Real Estate Leases: Protect Your Practice's Future— idealpractices.com

Frequently Asked Questions

Navigate lease obstacles in your practice sale

Lease assignment issues can derail a dental practice sale, but you don't have to navigate them alone. Minty Plus provides expert guidance through complex transactions, including lease negotiations and post-close management.