5 Common Problems When Buying a Dental Practice

Co-Founder, Minty Dental

In Summary

- Most loan rejections are driven by debt-to-income ratios, and solutions typically involve dental-focused lenders, seller financing, or restructuring the deal. Lenders look for predictable cash flow signals—dense scheduling, stable staff, strong hygiene recall, and transparent reporting.

- A clearly defined 30–90 day transition—usually 60 days—with written responsibilities ensures continuity and reduces patient attrition.

- No transition increases risk, so price or structure (e.g., earnout or seller financing) should adjust to compensate.

- Credentialing can take 60–120+ days, creating a temporary cash flow gap that requires early application and working capital planning.

- The priority is operational stability—meet staff, transfer critical accounts, communicate with patients, and avoid immediate system changes.

When Your Loan Gets Denied (And What to Look for During Site Visits)

A financing rejection doesn't close the door—it signals you need a different path forward. One dentist applied to eight different lenders before securing approval, a pattern more common than most buyers realize.

Why Most Denials Happen

The majority of rejections come down to debt-to-income ratio, not creditworthiness. Traditional banks see your student loan balance and stop there. Dental-specific lenders—institutions focusing exclusively on healthcare practice financing—understand that $300,000 in student debt doesn't predict your ability to run a profitable practice.

When a conventional bank denies your application, three alternatives typically make sense:

Apply to dental-focused lenders. Institutions like Bank of America Practice Solutions or Wells Fargo Practice Finance use different underwriting models, weighting practice performance more heavily than personal debt ratios.

Negotiate seller financing for part of the purchase. Many sellers will carry a note for 20-40% of the deal if they're motivated. A typical structure: the seller finances $150,000 of a $600,000 purchase over five years at 6-7% interest, while a bank covers the remaining $450,000. This reduces the institutional loan amount and demonstrates the seller's confidence in the practice's stability.

Adjust the deal structure. If lenders will only approve $550,000 of a $650,000 purchase, you have three levers: increase your down payment, negotiate a lower price, or ask the seller to finance the gap. One pattern worth noting: practices priced above 80% of collections often face financing resistance regardless of the buyer's qualifications.

What to Observe During Site Visits That Predicts Loan Approval

The practice tour is where you gather evidence that strengthens your financing case. Lenders want proof of sustainable cash flow—you're looking for the same thing.

Patient scheduling density. Open the appointment book for the past two weeks. Practices with steady 8:00 AM to 4:00 PM scheduling across multiple chairs generate predictable revenue. Sparse schedules or heavy reliance on emergency slots signal volatility that makes lenders nervous.

Staff tenure and engagement. Ask how long the front desk coordinator, hygienists, and lead assistant have been with the practice. Teams that have worked together for 3+ years indicate operational stability. High turnover often correlates with management issues that affect profitability.

Hygiene recall strength. Request the recare report from the practice management system. Practices with 60%+ active recall have built-in revenue continuity. Weak recall systems mean you'll need to rebuild the patient base, which extends your timeline to profitability.

Access to practice management software. During the visit, ask to see real-time reports: active patient count, accounts receivable aging, production by provider. Sellers who hesitate or claim the data isn't available are either disorganized or hiding something. Lenders will request this data during underwriting—if you can't get it during due diligence, the loan process will stall later.

One protection many buyers overlook: take photos of the schedule, operatory setup, and front desk workflow. These become reference points when comparing practices or explaining the opportunity to your lender.

For more on connecting what you observe during tours to deal viability, see When Should You Walk Away From Buying a Dental Practice?. And if you're still planning your path to ownership, From Associate to Owner: How Long It Really Takes to Buy a Practice walks through realistic timelines for securing financing.

How Long the Seller Should Stay (And What That Time Should Look Like)

A well-structured 60 days often outperforms a vague six-month arrangement. The difference isn't duration—it's clarity about what happens during that time.

Typical Timeframes and What Drives Them

For private practice sales, transition periods typically run 30-90 days, with 60 days being most common. DSO acquisitions follow a different model—sellers often stay 3-5 years under employment agreements.

The length you negotiate depends on three factors: whether you're already working in the practice, how much specialized clinical work the seller handles, and whether the patient base can support two providers during overlap.

If you're an associate buying out the practice, you may need minimal seller presence. Patients already know you. The handoff becomes operational—transferring vendor accounts, introducing you to the accountant, walking through payroll systems. In these cases, 30 days is often sufficient.

If you're acquiring a practice cold, 60-90 days gives you time for patient introductions, clinical case reviews, and staff reassurance. Beyond 90 days, diminishing returns set in unless the practice has multiple providers or the seller offers specialized services you can't replicate immediately.

What Should Actually Happen During Transition

Duration matters less than structure. Before closing, define four things in writing:

The seller's schedule and compensation. Will they work three days a week? Two half-days? Are they paid a percentage of collections (typically 30-35%), or is this unpaid time to finish work in progress? Vague agreements like "the seller will be available as needed" create conflict.

Patient introduction protocol. Who schedules the seller's time during transition? Do they see only their existing patients, or help with overflow? Staff members typically handle most patient introductions—they interact with patients first and set the tone. The seller's role is reinforcement, not primary communication.

Clinical handoff for complex cases. If the seller has patients mid-treatment—crown preps, ortho cases, implant restorations—define who completes that work and how it's compensated.

Exit milestones. What triggers the end of the transition period? A specific date? Completion of all work in progress? Clear exit criteria prevent the seller from lingering indefinitely or disappearing earlier than agreed.

One pattern worth noting: buyers who negotiate longer transitions often get less structured ones. A six-month arrangement sounds safer, but without defined responsibilities, the seller may show up sporadically. A 60-day transition with a written schedule and weekly check-ins typically delivers better continuity.

When the Seller Refuses Any Transition Period

If the seller won't stay at all—not even 30 days—that's worth addressing in price negotiations. Without that bridge, patient attrition risk increases, especially if you're unknown to the community.

Two ways to adjust for zero transition:

Reduce the purchase price. If the practice is priced at 80% of collections but the seller refuses any handoff, negotiate down to 70-75%. You're absorbing more risk—the price should reflect that.

Require seller-financed contingency. Structure part of the deal as an earnout tied to patient retention. If 85% of active patients return within six months, the seller gets the full amount. If retention drops below 70%, the final payment adjusts downward.

A seller who refuses any transition period and won't adjust price or terms is signaling something—either they're burned out, or they know something about the patient base they're not sharing.

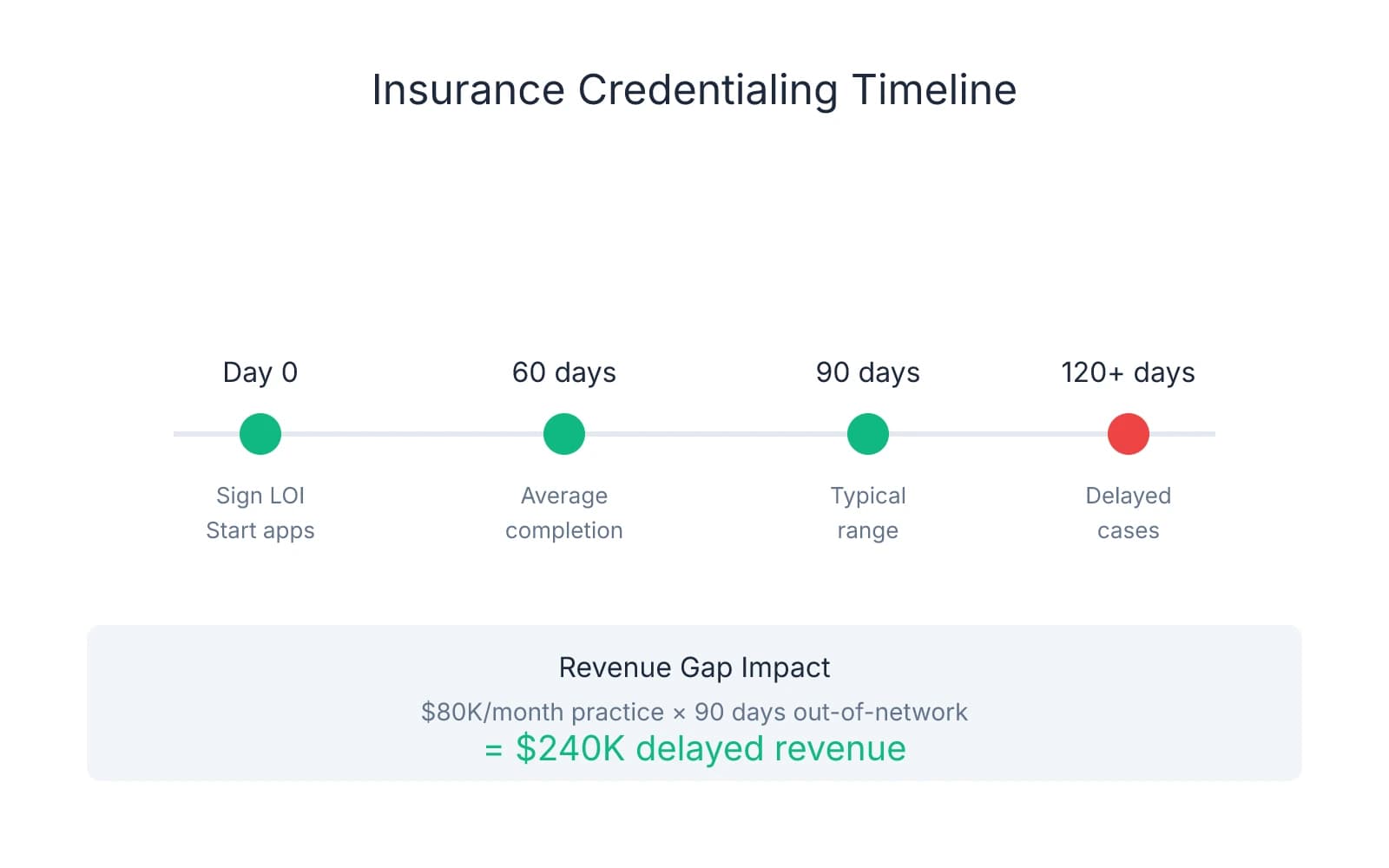

Navigating Insurance Credentialing Delays (And the Revenue Gap They Create)

Most buyers don't realize they can't bill insurance until credentialing completes—and that gap can stretch 60-120 days after closing. During that window, you're treating patients but not collecting insurance reimbursements.

Why Credentialing Takes Longer Than Expected

Insurance credentialing averages 60-90 days but frequently extends to 120+ days depending on the carrier and how complete your application is. The delay isn't arbitrary—insurance companies verify your license, run background checks, and process applications in order received.

Three factors drive most delays:

Incomplete applications. Missing a single form or uploading the wrong license verification stalls the entire process. Insurance companies don't follow up—they just move to the next application.

Carrier backlogs. Some insurers process applications within 45 days. Others take 90+ days as standard practice, with no way to expedite.

State-specific requirements. Certain states require additional documentation or have longer verification timelines for out-of-state dentists.

One protection many buyers overlook: start credentialing applications immediately after signing the LOI, not after closing. This shifts the credentialing window from post-closing to pre-closing, minimizing the revenue gap.

What Happens During the Gap

Until your credentialing completes, you're technically an out-of-network provider. Patients can still see you, but their insurance won't reimburse at in-network rates—which means higher out-of-pocket costs for them and delayed payments for you.

Two strategies help bridge this period:

Offer patients legal PPO discounts as an out-of-network provider. You can voluntarily discount your fees to match what the patient would have paid in-network. This reduces their financial burden and maintains loyalty during the transition.

Negotiate seller transition coverage to maintain billing continuity. If the seller stays on during transition and remains credentialed, they can continue treating patients under their provider number. This keeps insurance billing active while your credentialing processes. The seller works 2-3 days per week for 60-90 days, sees their existing patients, and bills under their credentials. You compensate them as an associate (30-35% of collections) during this period.

Planning for the Cash Flow Impact

Even with early credentialing applications, some gap is likely. If the practice typically collects $80,000 per month in insurance reimbursements and you're out-of-network for 90 days, you're looking at $240,000 in delayed revenue.

Two ways to prepare:

Secure a line of credit before closing. Many dental-specific lenders offer working capital lines of credit alongside practice acquisition loans. A $50,000-$100,000 line covers payroll, rent, and lab bills during the credentialing gap.

Build 90 days of operating expenses into your acquisition budget. If your monthly overhead is $60,000, set aside $180,000 in reserves specifically for the credentialing period. This isn't part of your down payment—it's working capital to cover the gap.

One pattern worth noting: buyers who assume credentialing will complete "on time" often face cash flow crises 60 days post-closing. The ones who plan for 120 days and finish early have breathing room.

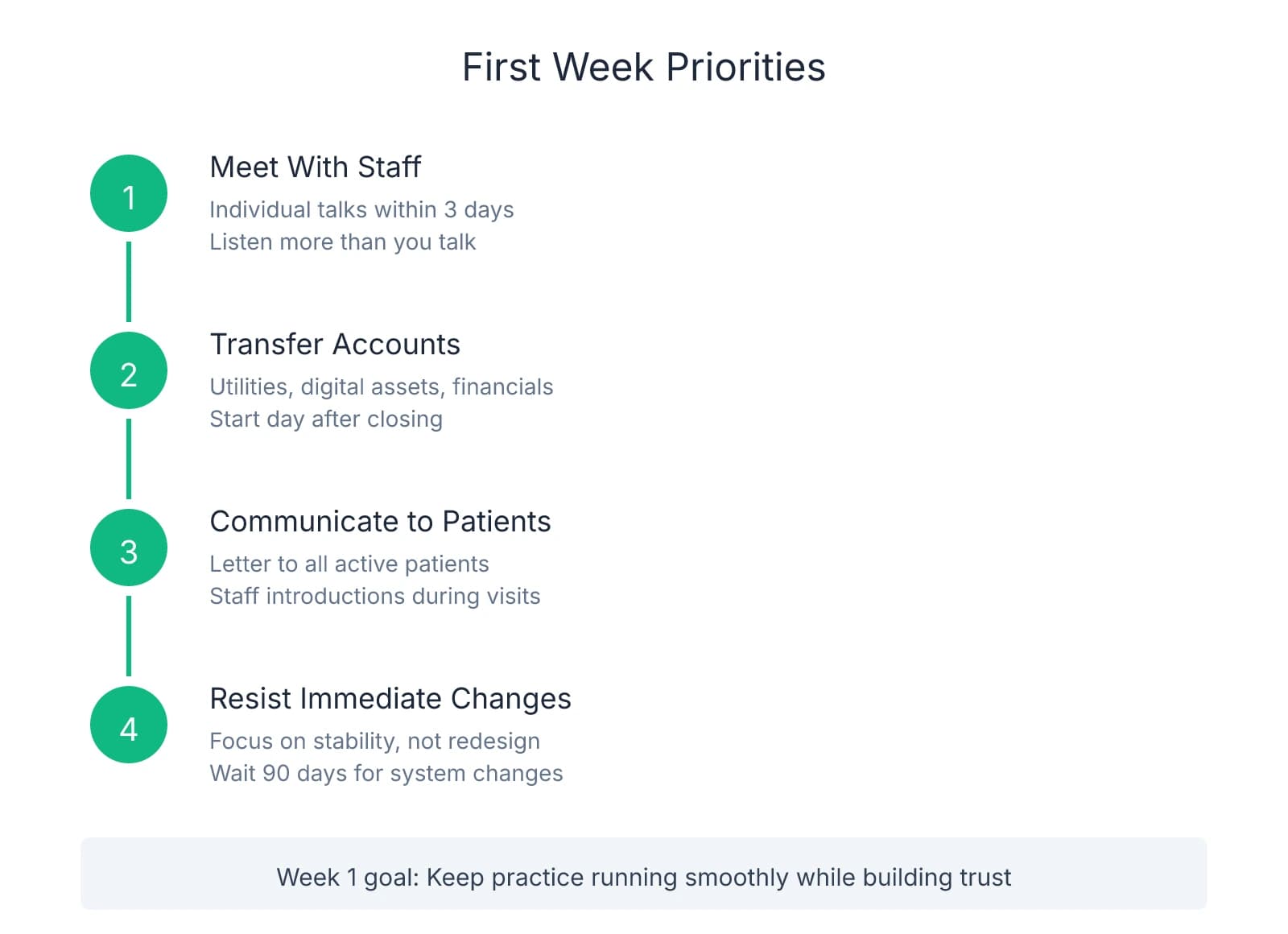

Your First Week as Owner: What Actually Needs to Happen

The first seven days set the trajectory for everything that follows. Your job isn't to implement your vision—it's to keep the practice running smoothly while building trust with the people who make that possible.

Meet With Staff Before You Change Anything

Schedule individual conversations with each team member within the first three days. Ask three questions:

- What's working well in the practice right now?

- What's one thing you'd improve if you could?

- What concerns do you have about the transition?

Listen more than you talk. The front desk coordinator knows which patients are likely to leave if their insurance gets dropped. The lead hygienist knows which systems are fragile and which ones can handle change. The assistant who's been there twelve years knows the seller's clinical shortcuts and where the practice actually makes money.

Transfer Essential Accounts and Digital Assets

Three categories of accounts need immediate attention: utilities and services, digital properties, and financial systems.

Utilities and services. Phone, internet, security monitoring, janitorial contracts, and medical waste disposal all need ownership transfers. Start this process the day after closing—some transfers take 7-10 business days.

Digital assets. Update ownership on the practice website hosting account, Google My Business listing, practice email domain, and social media accounts.

Practice management software and financial accounts. Add yourself as an administrator on the practice management system, update the EIN and tax information with your accountant, and transfer ownership of the business bank account.

One protection many buyers overlook: create a checklist of every account that needs transfer and assign each one a deadline.

Communicate the Transition to Patients

Patients need to hear about the ownership change from multiple sources: a written letter, staff introductions, and your own in-person presence.

Send a letter to all active patients within the first week. Keep it short: who you are, why you're excited to serve them, what's staying the same (same team, same location, same hours), and how to reach you with questions.

During appointments, have staff introduce you briefly: "Dr. [Name] is our new owner—she's been practicing for [X] years and we're excited to have her here." Then step in for a 30-second conversation.

Resist the Urge to Make Immediate Changes

The fastest way to lose staff and patients is to walk in on day one and start redesigning systems. Your priority in week one is operational stability—keeping the schedule full, keeping staff confident, and keeping patients satisfied.

That doesn't mean you ignore problems. If you notice a billing error or a safety issue, address it. But resist the temptation to implement new scheduling software, change the phone system, or rearrange the operatories. Those improvements can wait 90 days while you observe how the practice actually functions.

One decision framework that helps: for every change you're considering, ask whether it solves an urgent problem or whether it's about making the practice feel more like "yours." Urgent problems—broken equipment, compliance gaps, staff conflicts—get handled immediately. Everything else goes on a list for month four.

The first week isn't about proving yourself. It's about showing up, listening carefully, and keeping the practice running smoothly while you learn how it actually works.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- The Dental Practice Transition Period— www.adstransitions.com

- Transition Period in Dental Acquisitions - Kamkari Law— www.dentalmedicalattorney.comIndustry

- Insurance Credentialing in Dental Practice Transitions— www.adstransitions.com

- I Was Denied for My Dental Start-Up Loan 8 Times - Practice Biopsy— www.practicebiopsy.com

Frequently Asked Questions

Ready to navigate your practice acquisition journey?

Buying a dental practice involves complex challenges from financing to credentialing. Minty Plus provides hands-on guidance through every step of acquisition and the critical first weeks of ownership.