Working Capital in Dental Practice Loans, Explained

Co-Founder, Minty Dental

In Summary

- Working capital covers payroll, supplies, rent, and insurance reimbursement delays during the first 3-6 months—it's separate from the acquisition loan that buys the practice

- Most dental-specific lenders provide working capital as either a lump sum or line of credit, but not all lenders structure deals this way

- Buying accounts receivable reduces but doesn't eliminate working capital needs—you still need cash for immediate expenses and unexpected costs

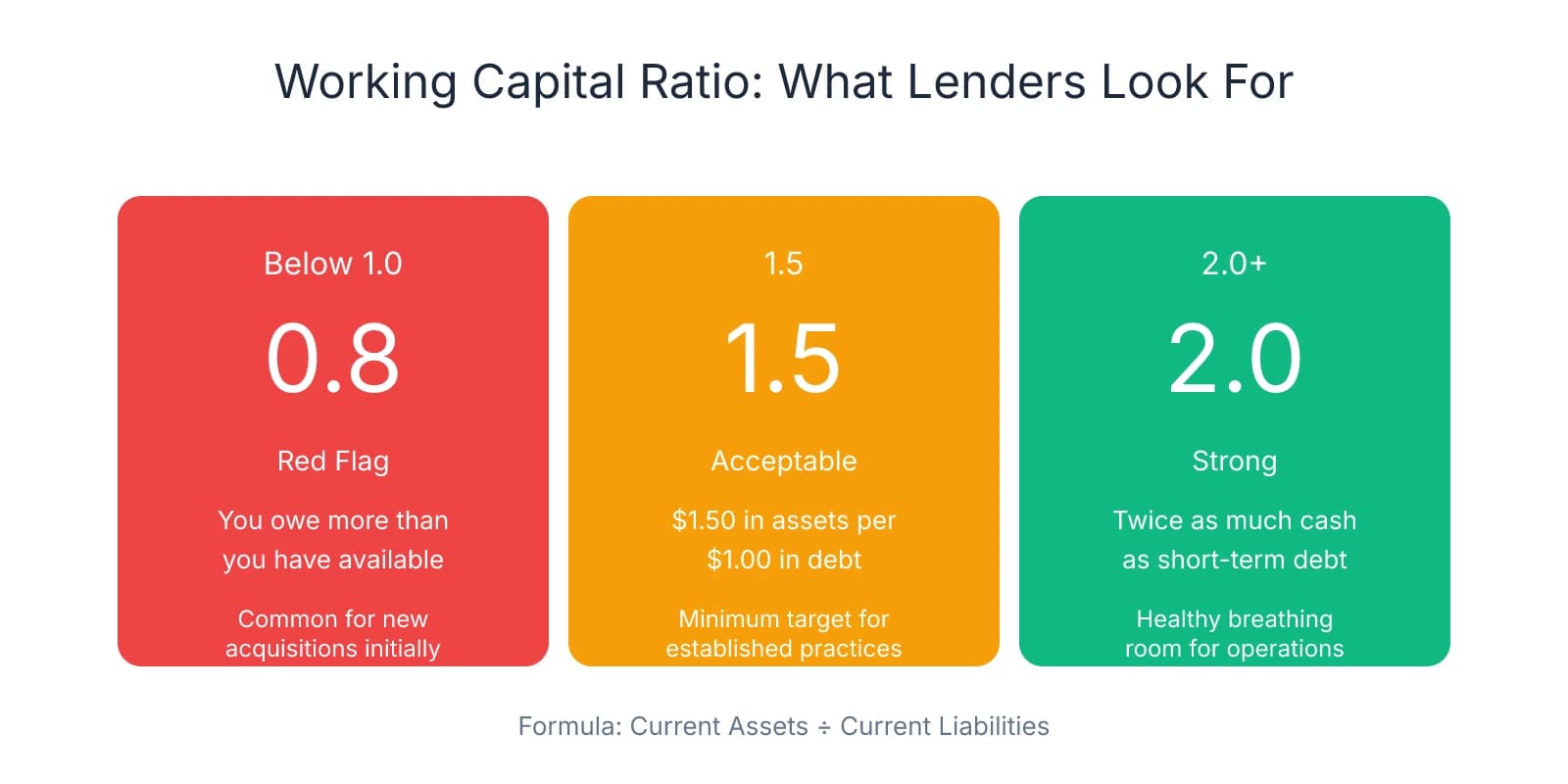

- A working capital ratio below 1.0 (current assets divided by current liabilities) signals you owe more than you have available—a red flag lenders watch closely

Working Capital Funds Operations, Not the Purchase

Working capital is current assets over current liabilities—the cash available to cover operating expenses. It's the money in your practice account that pays for payroll, supplies, rent, lab fees, and insurance claims that haven't cleared yet. The acquisition loan covers the purchase price. Working capital covers everything after you take ownership.

The distinction matters because most buyers focus exclusively on financing the purchase price and assume cash flow will handle the rest. What they miss is the gap between when expenses hit and when revenue lands in your account. Insurance reimbursements lag 30-60 days. Payroll hits every two weeks. Supply orders ship immediately. Working capital fills that gap.

Most dental-specific lenders provide working capital in addition to 100% purchase price financing, either as a lump sum at closing or as a line of credit you draw on as needed. The lump sum gives you immediate liquidity. The line of credit keeps your initial loan balance lower and lets you borrow only what you need. Both structures recognize that buying the practice and running it require different kinds of capital.

Where buyers get tripped up is assuming that buying accounts receivable eliminates the need for working capital. It doesn't. Accounts receivable give you cash flow from day one, but they don't cover the full operating cycle. You still need cash for payroll before those receivables convert to deposits, for supply orders that ship before insurance checks clear, and for the unexpected—a hygienist who quits, equipment that fails, a month where collections dip.

One pattern worth noting: buyers who underestimate working capital needs end up using personal funds, high-interest credit cards, or emergency financing to cover shortfalls. That's expensive, stressful, and avoidable. Calculate working capital before you close, not after you've burned through savings.

A useful benchmark is the working capital ratio—current assets divided by current liabilities. A ratio below 1.0 means you owe more than you have available in the near term, which lenders flag as a risk. A ratio of 2.0 means you have twice as much cash as you owe, giving you breathing room. Startups and new acquisitions often run below 1.0 initially, but lenders expect that ratio to normalize within the first few months as collections stabilize.

The calculation itself is straightforward, but getting the inputs right—especially projecting your first 90 days of expenses and collections—requires looking at the practice's actual cash flow patterns, not just its P&L. That's where many buyers who focus on how much cash they need at closing miss the operational reality that follows.

How Lenders Structure Working Capital: Lump Sum vs. Line of Credit

With the financing basics clear, the next decision is how to structure that working capital. Lenders provide it through two primary approaches: as an additional loan amount added to your acquisition loan, or as a revolving line of credit. The lump sum approach is more common—dental-specific lenders typically add $50,000 to $150,000 on top of the purchase price for solo practices. You receive the full amount upfront, deposited into your practice account, and start paying interest on the entire balance from day one.

The benefit is certainty. You know exactly how much liquidity you have before closing, and you don't need to manage draws or monitor credit limits. The downside is cost—you're paying interest on the full amount whether you use it immediately or not. If you only need $30,000 in the first 90 days but borrowed $100,000, you're still servicing debt on the unused $70,000.

A line of credit works differently. The lender approves a maximum borrowing limit—say, $100,000—but you only draw what you actually need, when you need it. Interest accrues only on the amount you've drawn, not the full credit line. If you draw $30,000 in month one and another $20,000 in month three, you're only paying interest on $50,000 total. The unused portion sits available for seasonal fluctuations, unexpected expenses, or months where collections dip below projections.

The tradeoff is discipline. A line of credit requires more active management—tracking what you've drawn, what's available, and when you can pay it down. For buyers already managing payroll, supply orders, and patient schedules, that extra layer of financial oversight can feel overwhelming. But for practices with predictable seasonal patterns—summer slowdowns, holiday dips—a line of credit offers flexibility that a lump sum can't match.

Both structures are typically unsecured, meaning no personal collateral is required beyond your personal guarantee. Terms usually run 5 to 10 years, with fixed monthly payments for lump sums and variable payments for lines of credit based on what you've drawn.

Where this breaks down is when lenders max out at the purchase price and can't provide additional working capital. This happens most often when the practice is overpriced relative to its cash flow, or when you're working with a local lender who lacks dental-specific experience. If the lender views the purchase price as already stretching your debt service coverage ratio, they won't layer on another $100,000 for working capital—they'll cap the loan at the acquisition amount and expect you to cover operations from personal liquidity or practice cash flow.

When lenders won't provide working capital, buyers have a few options. The most straightforward is using personal savings, though that exposes personal funds to business risk. Another approach is negotiating seller financing specifically for working capital—not the purchase price, but an additional $50,000 to $75,000 structured as a short-term note with deferred payments. This works when the seller is confident in the practice's cash flow and willing to stay invested in your success during the transition.

A third option is structuring the accounts receivable purchase to provide immediate liquidity. If you're buying A/R at a discount and the lender funds that purchase, you'll have cash flow from day one that can cover near-term expenses. The risk is overpaying for receivables that don't collect as expected, which is why verifying dental practice collections before closing matters more when working capital isn't part of your financing package.

The structure you choose depends on how predictable your cash flow is, how comfortable you are managing credit, and whether your lender even offers both options. Many buyers default to the lump sum because it's simpler, but in most cases, the flexibility of a line of credit outweighs the administrative overhead—especially when you're navigating the first six months of ownership and every dollar of interest expense matters.

Calculate What You Actually Need: Practice Size, Collections Timing, and the Working Capital Ratio

Once you've settled on a structure, the next step is calculating how much working capital you actually need. Start by identifying your monthly operating expenses—the cash that leaves your account regardless of what's coming in. For most practices, this includes payroll (typically 25-30% of collections), rent or mortgage payments, lab fees, supplies, utilities, insurance premiums, and marketing. Add these up and you'll usually land somewhere between 60-70% of monthly collections. If the practice collects $80,000 per month, expect operating expenses around $48,000 to $56,000.

That monthly expense figure becomes your baseline. The question is how many months of expenses you need to cover. The answer depends on how quickly revenue converts to cash in your account. Insurance reimbursements lag 30-60 days in most cases. If you take over on January 1st, the work you do that month won't hit your account until late February or early March. Meanwhile, payroll runs every two weeks, supply orders ship immediately, and rent is due on the first. That gap is what working capital fills.

A common rule of thumb is securing working capital equal to 2-3 months of operating expenses. If monthly expenses run $50,000, you need $100,000 to $150,000 in working capital to cover the transition period and insurance reimbursement delays. This assumes relatively stable collections and no major disruptions during the first 90 days. For practices with seasonal fluctuations—slower summers, busy fall and winter schedules—push that cushion to 3-4 months of expenses. A practice that sees collections drop 20-30% in July and August needs enough working capital to cover the gap without scrambling for emergency financing.

The working capital ratio gives you a way to measure whether you have enough liquidity relative to what you owe in the near term. Current assets include cash, accounts receivable expected to convert within 30-60 days, and any short-term investments. Current liabilities include accounts payable, payroll obligations, and any debt payments due within the next 12 months.

Lenders typically look for a working capital ratio between 1.5 and 2.0 for established practices. A ratio of 1.5 means you have $1.50 in liquid assets for every $1.00 in short-term debt. A ratio of 2.0 means you have twice as much cash as you owe. Startups and new acquisitions often run below this threshold initially—you're carrying debt from the acquisition, and collections haven't normalized yet—but lenders expect that ratio to climb as revenue stabilizes over the first few months.

Here's a calculation example: if monthly operating expenses are $40,000, and insurance reimbursements lag 30-60 days, you need at least 2-3 months of operating expenses as working capital—$80,000 to $120,000. If you're buying accounts receivable at closing, factor in the discount rate and collection timeline. Buying $100,000 in A/R at a 10% discount gives you $90,000, but not all of that will convert immediately. Some claims will take 60-90 days to collect, and a portion may never collect at all. Don't assume 100% immediate liquidity from purchased receivables—plan for 70-80% conversion within the first 60 days and treat the rest as a bonus if it comes through.

One adjustment many buyers miss is accounting for the practice's actual cash flow patterns, not just its P&L. A practice that shows $80,000 in monthly collections on paper might only deposit $60,000 in a given month because of insurance delays, patient payment plans, or seasonal dips. Pull 12 months of bank statements and calculate the average monthly deposits—that's your real cash flow baseline, and it's what you should use to calculate working capital needs, not the collections figure from the P&L.

The Post-Closing Working Capital Adjustment Most Buyers Don't See Coming

With your working capital calculation locked in, there's one more mechanism that can shift tens of thousands of dollars between buyer and seller 60 to 90 days after closing: the working capital adjustment. Most buyers treat it as paperwork, something the attorneys handle in the background. Where that becomes expensive is when the adjustment calculation wasn't clearly defined during negotiations, or when the seller ran down inventory and delayed payables in the weeks before closing.

Here's how it works: the purchase agreement establishes a target working capital level, usually based on a trailing 12-month average of the practice's current assets minus current liabilities. At closing, you calculate a preliminary working capital figure based on the balance sheet. Then, 60 to 90 days later, once all receivables have been collected and all payables have been reconciled, you calculate the actual working capital. If actual working capital is lower than the target, you receive a credit—the seller owes you the difference. If actual working capital is higher than the target, you owe the seller.

The adjustment exists because the balance sheet at closing is a snapshot, not a final accounting. Receivables that looked solid on paper may not collect. Payables that weren't recorded yet may surface. Inventory that was counted at closing may have been overstated. The true-up process reconciles what was promised with what was actually delivered.

Where buyers get burned is when the seller manipulates working capital in the weeks before closing. One pattern that shows up repeatedly: the seller stops ordering supplies, delays paying vendors, and accelerates patient collections. This inflates cash on hand and reduces payables, making the preliminary working capital calculation look stronger than it actually is. After closing, you're left with depleted inventory, angry vendors demanding payment, and a working capital adjustment that swings in the seller's favor because the "actual" working capital—once everything is reconciled—is higher than the target.

The opposite scenario is less common but equally painful: the seller leaves excess cash in the practice account or carries unusually high inventory levels at closing. The preliminary calculation shows working capital above target, so you owe the seller the difference. If the target was $75,000 and actual working capital at the true-up is $95,000, you owe the seller $20,000—on top of the purchase price you've already financed.

One protection many buyers overlook is negotiating the target working capital calculation during the LOI and purchase agreement phase, not waiting until closing to figure it out. The most defensible approach is using a trailing 12-month average, not a single month that may be artificially high or low. If the seller had an unusually strong December and wants to use that month as the baseline, you'll be chasing an inflated target that doesn't reflect normal operations. Push for an average that smooths out seasonal fluctuations and gives you a realistic benchmark.

The calculation methodology should be defined explicitly in the purchase agreement—what counts as a current asset, what counts as a current liability, how accounts receivable are valued, how inventory is counted, and who performs the reconciliation. If the agreement says "working capital will be calculated in accordance with GAAP," that's not specific enough. GAAP allows for interpretation, and interpretation is where disputes happen. Spell out the formula, the inputs, and the timeline for the true-up.

One clause worth negotiating is a cap on the adjustment—either a dollar limit or a percentage of the purchase price. If the purchase price is $600,000, you might cap the working capital adjustment at $30,000 or 5% of the purchase price. This limits your downside risk if the reconciliation uncovers issues that weren't visible during due diligence. Sellers often resist caps because they want full protection if working capital is lower than target, but in most cases, a reasonable cap protects both sides from extreme swings that neither party anticipated.

The timeline matters too. Most agreements call for a preliminary calculation at closing and a final true-up within 60 to 90 days. That's enough time to collect outstanding receivables and reconcile payables, but not so long that the practice's financial picture has shifted entirely under your management. If the true-up drags past 90 days, it becomes harder to separate what the seller left you from what you've done since taking over.

If you're navigating what buyers miss when evaluating a dental practice, the working capital adjustment is one of the most overlooked mechanisms—not because it's hidden, but because it doesn't feel urgent until after closing. By then, the terms are locked, and you're either receiving a credit or writing a check. The time to negotiate the adjustment is before you sign the purchase agreement, when you still have leverage and the seller still needs the deal to close.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- [PDF] Estimating your capital needs - BMO— bmo.com

- Working Capital Strategies When Buying a Practice - Dental CPAS— dentalcpas.comIndustry

- Dental Practice Working Capital | SBA & Conventional Loans— usmedicalfunding.comIndustry

Frequently Asked Questions

Ready to acquire your dental practice?

Understanding working capital is crucial when financing a dental practice acquisition. Minty Plus provides comprehensive guidance through the entire acquisition process, helping you secure the right financing and manage your new practice from day one.