How to Know If Dental Collections Are Real Before You Buy

Co-Founder, Minty Dental

In Summary

- Tax returns are designed to minimize taxable income, not reveal true cash-generating ability—your practice management software contains the unfiltered transaction history sellers can't easily alter

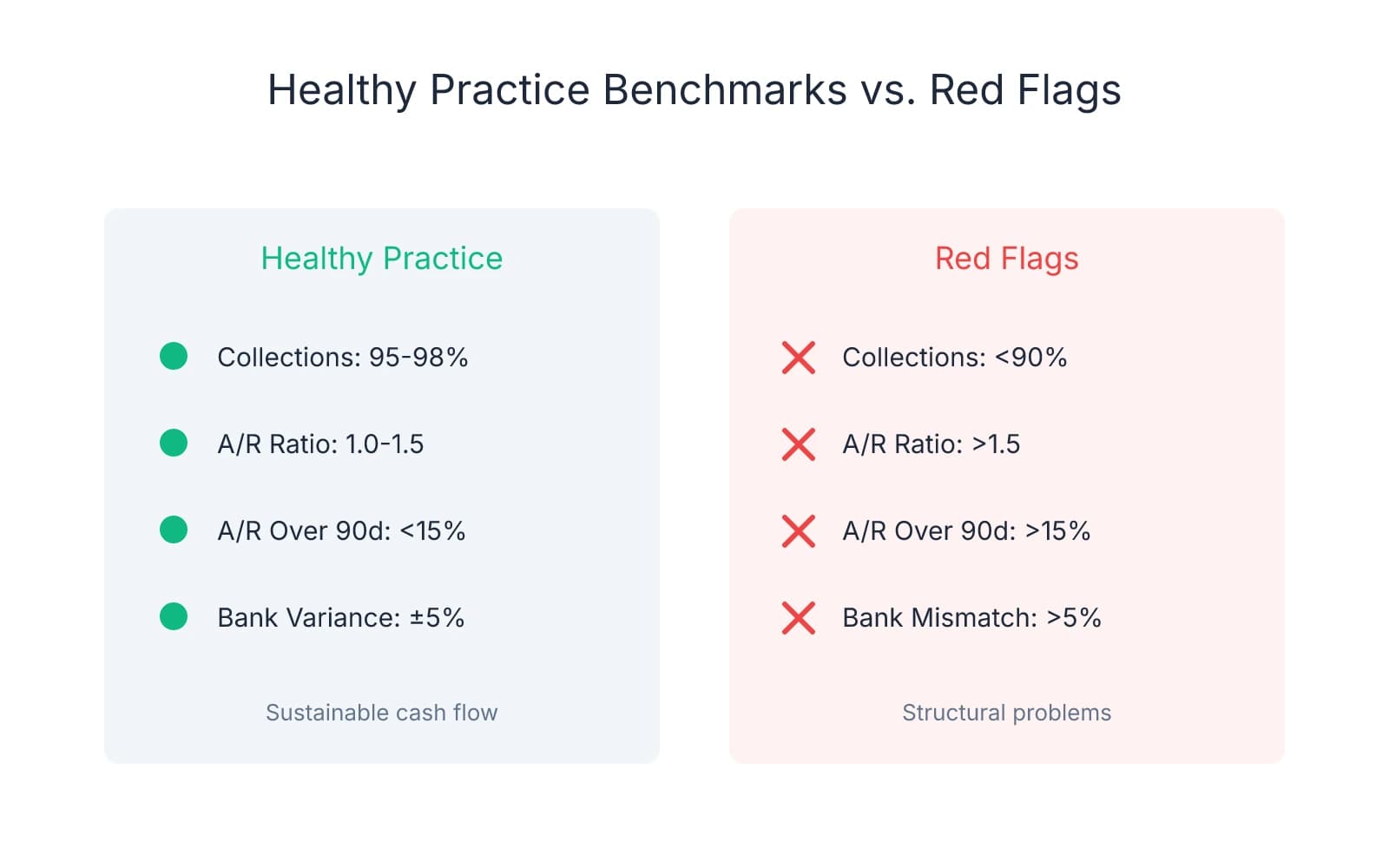

- Healthy practices collect 95-98% of adjusted production; significantly lower rates signal billing problems, insurance credentialing issues, or aggressive write-offs that will continue under your ownership

- The A/R aging report reveals whether strong collections are real or sitting on uncollectible debt—practices with over 15% of A/R aged past 90 days typically write off 30-40% as bad debt

- Bank deposits don't lie—reconciling 12-24 months of statements against PMS collection reports catches revenue inflation, unexplained transfers, and structural discrepancies before you close

- For practices over $1M in collections, spend $2,500-$5,000 on forensic PMS verification rather than risk discovering post-closing that revenue was overstated by $100K+ annually

Tax Returns Tell One Story—Your PMS Audit Tells Another

When a seller hands you three years of tax returns showing steady revenue growth, it's tempting to treat those numbers as gospel. But tax returns are designed to minimize taxable income—not to reveal a practice's true cash-generating ability. Sellers and their accountants legally manipulate timing, categorize expenses strategically, and take write-offs that make profitability look lower (or higher) than operational reality.

One protection many buyers overlook is forensic PMS verification—pulling production and collection data directly from the practice management software. Unlike tax returns, which reflect accounting decisions made months after transactions occurred, your PMS contains the unfiltered transaction history: every procedure coded, every adjustment entered, every payment posted.

Most practices run on Dentrix, Eaglesoft, or Open Dental. Each platform tracks gross production (what was billed), adjusted production (after contractual write-offs), and actual collections (cash that hit the bank). All three numbers matter, but they tell different stories. Gross production shows clinical activity. Adjusted production reflects what insurance and patients actually owe. Collections show what you converted to cash.

A pattern worth paying attention to: healthy practices collect 95-98% of adjusted production. When that percentage drops to 85% or 90%, it signals one of three problems—aggressive write-offs to avoid collection efforts, insurance credentialing issues causing claim denials, or broken billing processes aging receivables into uncollectible territory.

Request direct PMS access during due diligence, or at minimum, comprehensive production and collection reports with adjustment codes visible. Summary numbers from a seller's P&L won't show you why collections lag or where revenue is leaking. You need adjustment categories: contractual write-offs versus bad debt, insurance payments versus patient payments, procedure mix over time.

Where buyers often get burned is accepting a single collections number without understanding its composition. A practice might show $800K in annual collections, but if $200K came from a one-time insurance backlog payment or a PPO fee schedule about to reset, that revenue isn't repeatable. What many buyers miss is the difference between sustainable cash flow and accounting artifacts that inflate a single year's performance.

Cross-reference what the PMS reports against tax returns and bank deposits. If the PMS shows $850K in collections but the tax return reports $780K and bank statements show $820K in deposits, someone needs to reconcile those gaps. Timing differences are normal—insurance payments lag, refunds get processed—but material discrepancies without clear documentation warrant investigation before you wire the down payment.

The PMS audit isn't about catching fraud. It's about verifying that the revenue the seller claims is both real and repeatable under your ownership. What buyers often overlook is that a practice's financial performance can shift dramatically when fee schedules reset, key staff leave, or the seller's personal production disappears. The PMS data helps you model those scenarios with actual numbers instead of optimistic assumptions.

The Accounts Receivable Test: Where Inflated Collections Hide

With the PMS data in hand, the next place to look is accounts receivable—where strong collections on paper often mask uncollectible debt. Many buyers focus on the headline collections number and miss the structure behind it, which is often where the real risk sits.

Start with the A/R ratio: total accounts receivable divided by average monthly production. In most cases, a healthy practice carries an A/R ratio between 1.0 and 1.5. If the practice produces $80K per month, total A/R should sit between $80K and $120K. Anything above 1.5 signals the practice is billing faster than it's collecting—or worse, booking production without ever receiving payment.

What tends to happen is sellers report collections based on production figures, not actual cash received. They bill a $2,000 crown, post it as revenue, and count it toward annual collections—even if the patient never pays and the insurance claim gets denied. That unpaid balance sits in A/R indefinitely, inflating apparent revenue while contributing nothing to cash flow.

Request the A/R aging report for the past 12 months and look at how balances distribute across aging buckets. A healthy practice keeps 60-70% of A/R in the 0-30 day range, another 15-20% in 31-60 days, and less than 15% over 90 days. When more than 15% of A/R sits past 90 days, you're looking at either poor collection practices or balances that will never convert to cash. According to industry benchmarks, practices with over 20% of A/R aged beyond 90 days typically write off 30-40% of those balances as uncollectible.

Ask the seller three specific questions: "What's your collection percentage?" "How much A/R is currently over 90 days?" "Can I see your aging report for the past 12 months?" The answers will tell you whether the practice converts production to cash efficiently or whether you're inheriting a portfolio of uncollectible balances that will drag down your first-year cash flow.

Where buyers often get burned is assuming they can fix collection problems after closing. If the practice has been writing off bad debt for years, those patients expect that pattern to continue. If insurance claims have been denied repeatedly due to credentialing issues, you'll spend months resolving those problems while carrying the same uncollectible A/R the seller left behind. When the A/R structure is fundamentally broken, it's often a signal to walk away rather than assume you can repair it post-acquisition.

Cross-Referencing Bank Deposits Against Reported Collections

The most direct way to verify whether collections are real is to follow the money. A practice can manipulate PMS reports and adjust A/R aging—but bank deposits don't lie. When you match 12-24 months of business bank statements against collection reports from the same period, you're conducting the most concrete verification available: did the cash the seller claims to have collected actually make it to the bank?

Request complete business bank statements for the past two years—not summaries or screenshots, but full monthly statements showing every deposit, withdrawal, and transfer. Then pull the corresponding monthly collection reports from the PMS. Your goal is to reconcile: does the total deposited each month match what the PMS says was collected?

In most cases, you'll find small timing differences. Insurance payments post to the PMS when the claim is processed, but the check doesn't clear until three days later. Patient payment plans show as collected when posted, but ACH transfers take 24-48 hours to settle. These are normal operational lags—nothing to worry about as long as monthly totals align within a few percentage points over a rolling 90-day window.

What you're watching for are structural discrepancies: months where reported collections are $15K higher than bank deposits with no clear explanation, or patterns where deposits consistently exceed collections by amounts suggesting unreported revenue. One pattern worth paying attention to is when bank deposits include large, irregular transfers from personal accounts. Where I've seen deals go sideways is when sellers quietly move personal funds into the business account to inflate apparent revenue—then report those deposits as collections.

A real example: a buyer pulled 18 months of bank statements and found three deposits of $25K, $30K, and $20K labeled "transfer" with no corresponding PMS entries. When questioned, the seller explained they were "temporary loans to cover payroll." But the deposits occurred in months where the practice reported its highest collections—and none of the funds were ever repaid. The buyer's accountant flagged this as revenue inflation: the seller was manufacturing deposits to make cash flow look stronger than it was.

Ask the seller to explain any deposit that doesn't match a corresponding PMS entry. Legitimate explanations include equipment sale proceeds, tax refunds, or loan disbursements—but those should be documented and easy to verify. Unidentified deposits or deposits that don't match reported collections are major red flags.

Your lender will likely require a 4506 form—IRS tax return verification—which confirms that the tax returns the seller provided match what was actually filed. This catches sellers who hand you a "draft" return showing higher revenue than what they reported to the government. According to SBA lending guidelines, lenders use 4506 verification to ensure borrowers aren't misrepresenting income, and discrepancies between provided returns and filed returns often kill financing.

When you find a $50,000+ gap between bank deposits and reported collections, you have three options. First, ask the seller to reconcile the difference with documentation—insurance payment logs, refund records, or timing explanations that close the gap. Second, adjust your valuation downward to reflect the lower verified collections figure. Third, walk away if the seller can't or won't explain the discrepancy. Many buyers face this exact scenario and assume they can resolve it post-closing—but if the numbers don't reconcile during due diligence, they won't reconcile after you own the practice.

One protection many buyers overlook is requesting deposit detail for the largest transactions. If a practice shows a $40K deposit in March, ask for the remittance advice or EOB that corresponds to that payment. Insurance companies send detailed explanations of benefits with every reimbursement. If the seller can't produce documentation for large deposits, that's a signal the deposit might not be legitimate practice revenue.

Building Your Verification Checklist Before You Sign

With the frameworks above in place, you need the specific documents, calculations, and questions that turn theory into action. Verification isn't about being paranoid—it's about making a decision based on facts rather than seller representations.

Start by assembling your document request list: three years of business tax returns (Form 1120 or 1120-S), 12-24 months of PMS production and collection reports broken down by month, current A/R aging reports showing balances by 30/60/90/120+ day buckets, 12-24 months of business bank statements with all pages included, and adjustment code summaries showing contractual write-offs versus bad debt.

Once you have the documents, perform three calculations yourself. First, calculate the collections percentage: total collections divided by adjusted production. Healthy practices collect 95-98% of what they're owed after contractual adjustments. Anything below 90% signals billing problems or aggressive write-offs that will continue under your ownership. Second, calculate the A/R ratio: total accounts receivable divided by average monthly production. A ratio above 1.5 means the practice is billing faster than it's collecting. Third, reconcile bank deposits against reported collections for each month. If deposits consistently fall short of collections by more than 5%, you're looking at either timing issues that need explanation or revenue that was reported but never received.

Watch for specific red flag thresholds: collections under 90% of adjusted production, an A/R ratio above 1.5, more than 15% of A/R aged over 90 days, or bank deposits that don't match reported collections within 5% over a rolling quarter. According to dental practice due diligence specialists, these thresholds separate practices with sustainable cash flow from those with structural financial problems that will become your problems post-closing.

For practices reporting over $1M in annual collections, bring in a dental-specific CPA or practice consultant to conduct forensic PMS verification. They'll pull data directly from Dentrix, Eaglesoft, or Open Dental and audit adjustment codes, payment sources, and procedure mix in ways that surface problems you might miss. The cost—typically $2,500-$5,000—is minor compared to the risk of overpaying for inflated revenue or inheriting uncollectible A/R. Many first-time buyers skip this step to save money, then discover post-closing that collections were overstated by $100K+ annually.

Frame your verification requests professionally. Try: "My lender requires PMS access and bank statements as part of their underwriting process. Can we schedule time for my accountant to pull production and collection reports directly from your system?" Most sellers understand that serious buyers verify financial claims—and those who resist transparency often have something to hide.

If the seller refuses to provide PMS access or detailed financial documentation, you have two options. First, make your offer contingent on verification—if they won't provide access before closing, structure the deal so you can walk away penalty-free if post-closing audits reveal material discrepancies. Second, walk away entirely. What many buyers miss is that sellers who won't share financial data during due diligence are signaling either that the numbers don't support their asking price or that they're hiding problems they don't want discovered until after you've wired the funds.

Your verification checklist isn't a formality—it's the difference between buying a practice based on verified cash flow and buying one based on optimistic projections that evaporate the day you take ownership. Request the documents, run the calculations, and ask the hard questions before you sign.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Financial Due Diligence for Dental Practices: What to Look For in 2026— duckettladd.com

- Due Diligence for Evaluating Dental Practices— dentalcpaca.comIndustry

Frequently Asked Questions

Verify Collections Before Buying a Practice

Inflated collections claims can derail your practice acquisition. Minty Plus provides expert due diligence guidance to validate financial claims and protect your investment from day one.