Dental Practice Startup vs Acquisition: Which Path Fits You

Co-Founder, Minty Dental

In Summary

- Startup costs ($500K-$800K) look cheaper than acquisitions ($750K-$1.2M), but working capital requirements reverse the equation—startups need $150K-$250K in reserves to survive 18-24 months before profitability

- Acquisitions generate immediate cash flow from day one, meaning your loan payment is covered by existing patient revenue while you transition into ownership

- Lenders view acquisitions as lower-risk investments despite higher loan amounts, often resulting in better financing terms due to proven revenue history

- Transaction costs for acquisitions add $35K-$65K upfront, but the immediate revenue stream offsets these expenses within the first few months of operation

The Real Cost Difference Isn't What Most Buyers Expect

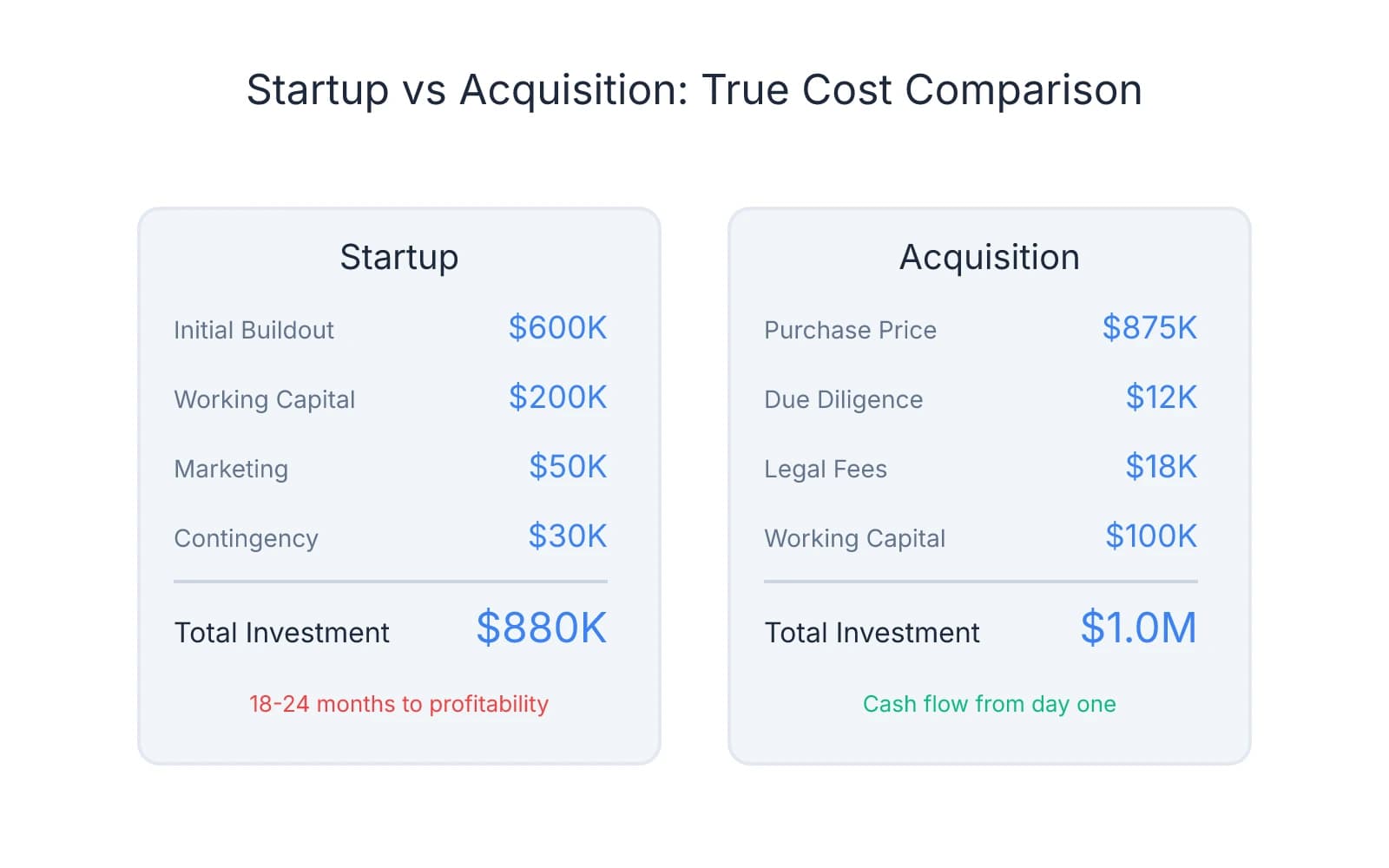

The headline numbers tell you startups cost less. Median practice sale prices sit around $875,000 for established general practices, while startup buildouts range from $500,000 to $800,000. That $200,000-$300,000 gap looks decisive until you calculate what happens in the 18 months after you sign.

Startups demand $150,000-$250,000 in reserves to cover payroll, rent, supplies, and loan payments while you build a patient base from zero. Most new practices take 18-24 months to reach profitability—meaning you're funding operations out of savings while servicing debt. Acquisitions flip this model: you're buying revenue on day one, and existing patient cash flow covers your loan payment from the first month.

A $600,000 startup looks manageable until you add $200,000 in working capital, $50,000 in marketing, and $30,000 in unexpected delays. Your all-in number approaches $900,000—more than many acquisition deals—with no guarantee of patient volume.

Banks view acquisitions as lower-risk investments despite higher loan amounts. An established practice with three years of tax returns, stable patient counts, and predictable collections gives lenders confidence in your ability to service debt. Student loan debt doesn't prevent you from securing a practice loan—what matters is demonstrable cash flow to cover both obligations.

Transaction costs for acquisitions add $35,000-$65,000 upfront: $8,000-$15,000 for due diligence, $12,000-$25,000 in legal fees, and $75,000-$150,000 in working capital to cover the transition period. These aren't trivial expenses, but they're offset by immediate patient revenue. A practice generating $1.2 million annually produces roughly $100,000 in monthly collections—enough to cover your loan payment, payroll, and operating expenses while you learn the business.

Cash Flow Timeline: When You Actually Start Taking Home Income

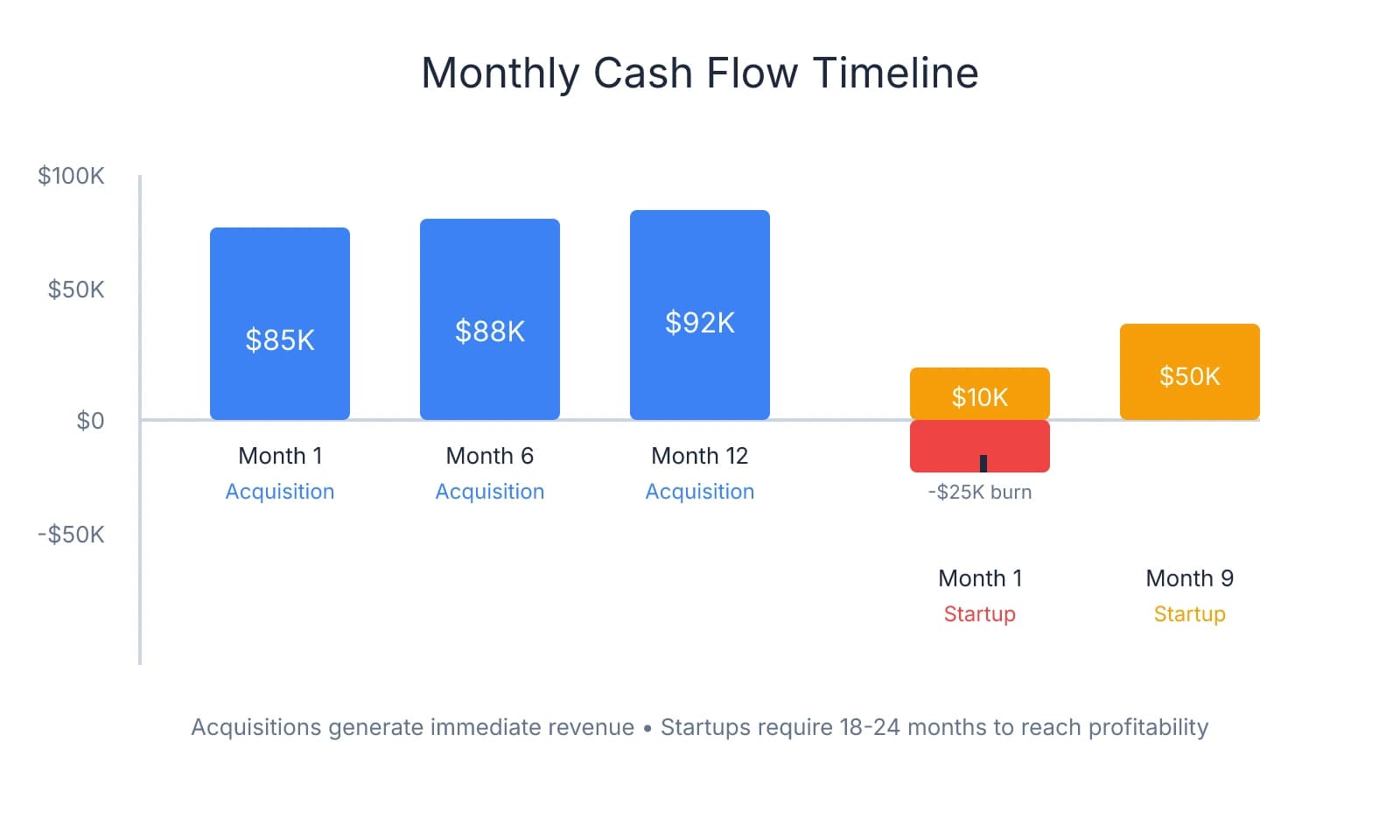

That cost comparison matters less than the revenue timeline. Acquisitions generate income from the day you take ownership—existing patients keep scheduling, hygiene recall stays active, and collections flow into your account. Startups operate in reverse: you're writing checks for rent, payroll, and loan payments while waiting for patients who don't exist yet.

When you acquire a practice, you inherit a patient base that produces immediate cash flow. A $1M collection practice generates roughly $80,000-$85,000 in monthly revenue, enough to cover a $7,000 loan payment, $50,000 in overhead, and leave room for owner compensation. You're not taking home what the seller did—patient attrition averages 10-20% during transitions when handled properly—but you're covering debt service and operating expenses from day one.

Startups face a different equation. In months 1-3, you're typically seeing 5-15 new patients while burning $25,000-$35,000 monthly on fixed costs. Most new practices don't hit $50,000 in monthly collections until month 6-9. During this period, you're funding the gap between revenue and expenses from working capital reserves—which is why the $150,000-$250,000 cash cushion isn't optional.

First-year acquisition buyers often take home less than they made as associates, even though the practice is profitable. If you were earning $180,000 as an associate and buy a practice generating $1M in collections, you might take home $120,000-$140,000 in year one after debt service and reinvestment. That $40,000-$60,000 gap isn't a loss—it's equity buildup through loan paydown—but it affects your lifestyle during the transition.

Startup owners face a steeper version of this tradeoff. Many take zero salary for the first 12-18 months, living off savings or a working spouse's income while the practice builds patient volume. Break-even for acquisitions typically occurs within 3-5 years, measured from when cumulative owner benefit exceeds invested capital. Startups extend that timeline to 4-7 years, driven primarily by the 18-24 month revenue ramp before profitability.

The 10-20% attrition rate in acquisitions sounds concerning until you compare it to startup patient acquisition timelines. Losing 15% of a 2,000-patient base still leaves you with 1,700 active patients generating predictable revenue. Building 1,700 patients from scratch takes most startups 24-36 months of consistent marketing and word-of-mouth growth.

Where this difference compounds is in your ability to service debt. Acquisition buyers can cover loan payments from existing cash flow while gradually improving systems. Startup owners are racing against their working capital burn rate—every month of slow patient growth extends the timeline before they can pay themselves.

Control vs Speed: What You Gain and Give Up in Each Path

The decision ultimately hinges on a single tradeoff: do you value the ability to build exactly what you want, or do you need operational momentum and immediate revenue?

When you build from scratch, you're making every decision that defines the practice. Location selection follows demographics you choose—not what happened to be available when the seller opened 20 years ago. You're selecting technology based on current standards, not inheriting a 2012 Dentrix server and operatory equipment that's been "good enough" for a decade. Payer mix reflects your strategic decisions: you can launch fee-for-service, selectively credential with PPOs that fit your target patient profile, or avoid insurance panels entirely.

Staff culture starts with your first hire. You're building a team that knows your systems from day one because you trained them. Fee schedules, clinical protocols, patient communication workflows—every operational element reflects your vision rather than inherited decisions you're trying to reverse.

Where this control becomes costly is the 18-24 month build phase. You're not just choosing systems—you're creating them while simultaneously attracting patients, training staff, and establishing vendor relationships. Insurance credentialing alone takes 3-6 months before you can see PPO patients, meaning early revenue depends entirely on fee-for-service volume.

In an acquisition, you're walking into a functioning business. Patients are scheduled for the next six weeks. Staff know the software, the supply vendors, the lab relationships, and which insurance plans reimburse fastest. The practice has established referral relationships with specialists, a recall system that's been running for years, and operational workflows that don't require you to build them from scratch.

Revenue starts immediately—not in 18 months. A practice collecting $1M annually generates roughly $80,000-$85,000 monthly from day one, covering your loan payment and operating expenses while you learn the business.

The tradeoff is inheriting the seller's decisions. That location might be in a declining neighborhood or a building with a landlord who hasn't updated HVAC in 15 years. Equipment condition varies—some sellers invest in updates before listing, others sell practices with operatory chairs from 2008 and panorex units that technically function but produce grainy images. Payer mix often includes PPO contracts the seller signed years ago when reimbursement rates were higher, and renegotiating or dropping plans risks losing the patients who depend on them.

Staff loyalty to the previous owner creates transition friction. Employees who've worked with the seller for 10-15 years may resist protocol changes or question your clinical decisions. Some buyers spend the first year managing around key staff members before making difficult termination decisions—which then triggers patient attrition when longtime hygienists or front desk staff leave.

Outdated technology compounds this problem. If the practice runs on paper charts or legacy software, you're either accepting inefficiency or investing $30,000-$50,000 in system upgrades during your first year—on top of your acquisition loan.

Patient acquisition from zero is the defining constraint in startups. Most new practices see 5-15 patients in month one, 20-40 by month three, and 60-100 by month six if marketing is aggressive. Building to 1,500-2,000 active patients—the baseline for a sustainable general practice—takes 24-36 months under normal growth conditions.

Insurance credentialing delays compress early revenue. Even if you plan to participate with major PPOs, the application and approval process takes 90-180 days. During that window, you're either seeing fee-for-service patients only or accepting the reduced reimbursement that comes with out-of-network billing.

A Decision Framework: Matching the Path to Your Situation

The choice isn't about which path is objectively better—it's about which model fits your specific financial position, risk tolerance, and professional priorities.

Buy an existing practice if: You have less than 12 months of living expenses saved beyond your down payment. Acquisitions generate immediate cash flow that covers loan payments and operating expenses from day one, eliminating the need to fund operations from reserves while building patient volume.

You found a practice in a location that fits your long-term goals, with solid financials and a patient base you can retain. The opportunity cost of passing on a well-positioned practice—especially in markets where listings are scarce—often outweighs the control you'd gain from starting fresh. Location matters more than most buyers realize, and inheriting a proven site removes demographic risk.

You can negotiate structured transition support—ideally 60-90 days with defined responsibilities. Seller presence during the handoff protects patient retention and gives you time to learn operational workflows.

You prefer operational momentum over customization. If your priority is practicing dentistry rather than creating infrastructure, acquisition speed fits that preference.

Start from scratch if: You have 18+ months of living expenses saved beyond your startup capital. Working capital reserves aren't optional in a startup—they're the buffer that determines whether you survive the 18-24 month ramp to profitability.

You want full control over location, technology, and practice culture. Startups let you choose the exact site based on current demographics, select equipment that reflects 2025 standards, and build a team that knows your systems from day one.

You're in an underserved market with strong demographics and limited competition. Markets where the dentist-to-population ratio sits below the national average create faster patient ramps for new practices.

You have the risk tolerance to build from zero and value long-term vision over immediate cash flow. Startup owners spend the first 12-18 months funding operations from savings while patient volume builds.

Self-assessment factors that clarify the decision:

- Working capital reserves: Can you fund 18-24 months of living expenses plus startup overhead, or do you need immediate income to service debt?

- Risk tolerance: Does the uncertainty of building patient volume from zero energize you, or does the stability of inherited cash flow reduce stress?

- Timeline pressure: Are you willing to wait 18-24 months before taking home meaningful income, or do you need salary replacement within the first year?

- Location control: Is choosing the exact site critical to your long-term vision, or is inheriting a proven location an acceptable tradeoff for operational speed?

Some dentists thrive on the creative challenge of building a practice from scratch—designing the layout, selecting technology, establishing clinical protocols. Others prefer inheriting operational systems and focusing energy on patient care rather than infrastructure development. Neither preference is better, but mismatching your personality to your path creates friction that compounds over years.

If you're leaning toward acquisition, start building your advisory team now—connect with a practice transition attorney, a CPA experienced in dental practice valuations, and a lender who specializes in SBA practice loans. Get pre-qualified for financing so you know your buying power before you find a practice.

If you're leaning toward startup, focus on market research and demographic analysis first. Identify underserved areas with strong population growth, favorable income levels, and limited competition. Build your working capital reserves to the 18-24 month threshold, and develop relationships with equipment vendors, contractors, and consultants who specialize in practice buildouts.

The decision isn't permanent, but it shapes the next 3-5 years of your professional life. Match the path to your financial position and risk tolerance, not to abstract advice about which model is "better."

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Demystifying the Practice Loan Process | American Dental Association— ada.orgIndustry

- Demystifying the Practice Loan Process | American Dental Association— ada.orgIndustry

- Patient Retention Following a Dental Practice Sale— dentaltransitions.comIndustry

- Demystifying the Practice Loan Process | American Dental Association— ada.orgIndustry

Frequently Asked Questions

Ready to find your ideal dental practice?

Whether you're leaning toward acquisition or startup, exploring available practices is the first step. Browse dental practices nationwide to see what opportunities match your vision and goals.