Should You Sell Your Dental Practice to a DSO?

Co-Founder, Minty Dental

In Summary

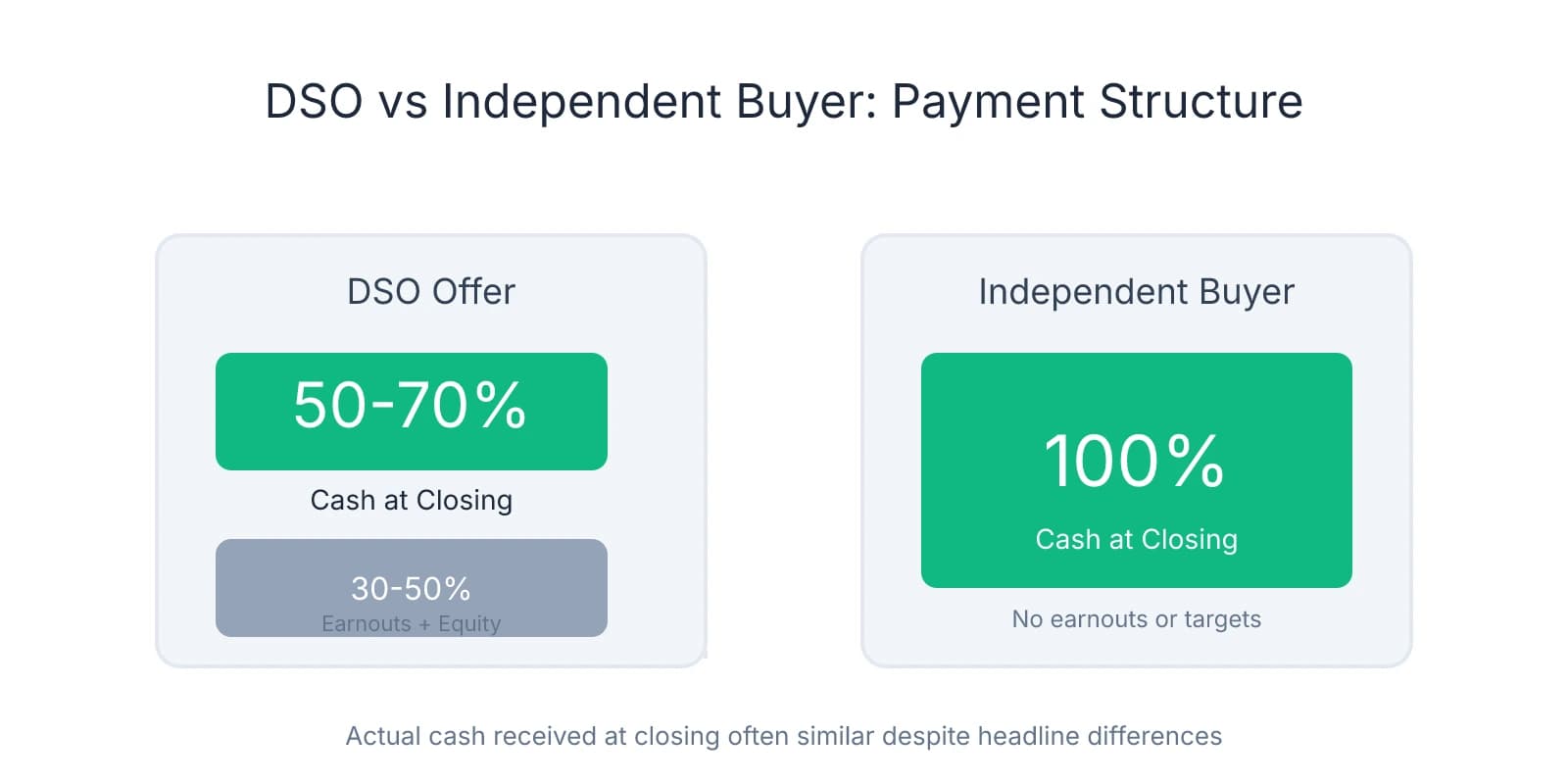

- DSO offers typically pay only 50-70% cash at closing, with the remainder tied to earnouts or multi-year employment commitments that may never materialize

- Independent buyers offer 100% cash at closing with no production targets or contingencies—giving sellers immediate liquidity and a clean exit

- Most sellers prefer the simplicity of an independent sale, with some advisors reporting that 95% of their clients choose independent buyers when both options are available

- DSOs target practices generating $1.2M+ in revenue with 20%+ EBITDA margins—many solid opportunities fall outside these thresholds

DSO Offers Look Bigger Because They're Structured Differently

You find a practice you want, start running numbers, and then hear a DSO offered 20% more. It feels like you're outgunned before you even submit a letter of intent.

That headline number rarely tells the full story.

Most DSO offers pay only 50-70% cash at closing. The remaining 30-50% gets tied to earnouts, production targets, or equity rollovers that may take three to five years to materialize—if they materialize at all. Many deals include work-back requirements, meaning the seller stays on as an employee with reduced autonomy and compensation tied to metrics they no longer control.

Independent buyers typically offer 100% cash at closing. No earnouts. No equity rollovers. No multi-year employment commitments. The seller gets paid in full, provides four to six weeks of transition support, and walks away with certainty.

When you compare actual cash received at closing—not the headline number—independent buyers and DSOs often land in a similar range. The difference is what comes with that number. One path gives immediate liquidity and a clean exit. The other spreads payment across years, introduces performance risk, and keeps the seller tethered to the practice long after they expected to leave.

A seller who sees two offers—one for $1.2 million cash at closing, another for $1.4 million with $500,000 deferred over three years and tied to production—isn't just comparing price. They're comparing certainty against complexity, liquidity against risk, and a short transition against years of continued involvement.

Research shows that when both options are available, the vast majority of sellers gravitate toward independent buyers. That preference isn't about sentimentality—it's about deal structure. Sellers want to know exactly what they're getting, when they're getting it, and when they can move on.

Sellers who initially lean toward DSO offers often reverse course once they understand the fine print. The earnout language, the equity rollover terms, the employment agreement—these details surface during due diligence, and many sellers realize the deal isn't what they thought. By that point, if an independent buyer presented a clear alternative early in the process, the seller already knows where they'd rather land.

Your advantage isn't capital—it's structure. The question isn't whether you can pay more. It's whether you can show the seller what they're actually comparing.

Most Sellers Prefer What You're Offering

That structural advantage matters because most sellers prefer the certainty and simplicity of an independent sale over the complexity of a DSO deal. Some advisors report that 95% of their clients choose independent buyers when both options are available.

What sellers consistently prioritize is a clean exit with no ongoing employment obligations. They want to provide four to six weeks of transition support, introduce the new owner to patients and staff, and then step away on their terms. DSO deals often require three to five years of continued employment, with compensation tied to production targets the seller no longer controls. Many sellers initially assume they'll enjoy staying involved—until they realize they're working under someone else's operational protocols, with reduced autonomy and metrics that may trigger earnout clawbacks if the practice underperforms.

The cautionary tales circulate quickly. Sellers hear about colleagues who lost promised bonuses when production dipped, practices that closed within two years under corporate ownership, or doctors who had to buy their practices back after corporate management eroded patient volume and staff morale. These stories are common enough that many sellers approach DSO offers with skepticism, even when the headline number looks attractive.

What independent buyers offer is exactly what most sellers want: certainty at closing, preservation of practice culture and staff, and a straightforward transaction without complex legal structures. When a seller knows they'll receive 100% cash at closing, with no earnouts or equity rollovers, the decision becomes simpler. They can plan their retirement, pay off debt, or reinvest in other ventures without waiting years to see if deferred payments materialize.

The cultural preservation piece matters more than many buyers realize. Sellers built their practices over decades. They know their staff by name, understand patient preferences, and take pride in the reputation they've cultivated. Selling to an independent buyer who plans to maintain the practice's identity—keeping the name, retaining the team, continuing the same standard of care—aligns with how most sellers want to be remembered. DSO deals often involve rebranding, staff turnover, and operational changes that erase the seller's legacy within months.

One protection many sellers overlook is the risk of earnout clawbacks. DSO agreements often include language that reduces or eliminates deferred payments if the practice fails to hit production targets post-sale. The seller no longer controls scheduling, marketing, or staffing decisions—but their payout depends on metrics influenced by those factors. Independent buyers eliminate that risk entirely.

When presenting an offer, frame it as a clean transaction: full payment at closing, a short transition period with defined responsibilities, and a commitment to preserving what the seller built. If you've already started asking the right questions about the seller's goals and concerns, you'll know exactly which points to emphasize—whether it's staff retention, patient continuity, or the ability to walk away without ongoing obligations.

Understanding Which Practices DSOs Actually Target

The fear that DSOs will outbid you on every deal assumes you're competing for the same practices. You're not. DSOs operate with specific acquisition criteria that exclude a significant portion of the market.

DSOs typically target practices generating $1.2 million or more in annual revenue, with EBITDA margins above 20%. That financial profile signals operational efficiency, strong provider productivity, and enough cash flow to justify the infrastructure costs DSOs absorb when integrating a new location. Practices below that threshold—even those with solid patient bases and consistent collections—often don't meet the minimum return requirements DSOs need.

DSOs aren't building portfolios one practice at a time based on individual merit. They're executing regional strategies that require density, scalability, and practices that fit into multi-location networks. A standalone practice in a market where the DSO has no other presence—even if it's profitable—rarely makes strategic sense. They need practices that support regional clustering, shared back-office infrastructure, and the ability to negotiate better rates with suppliers and payers across multiple locations.

The EBITDA threshold matters more than revenue alone. A practice generating $1.5 million in collections but operating at 15% EBITDA doesn't meet DSO criteria, even though it's profitable. DSOs underwrite deals based on normalized EBITDA because that's what determines valuation multiples and integration feasibility. Practices with lower EBITDA margins require operational overhauls that delay profitability and increase risk—something DSOs avoid unless the practice offers other strategic value.

Independent buyers have a structural advantage in practices that generate strong cash flow but don't meet DSO acquisition thresholds. A practice producing $900,000 annually with 18% EBITDA might support a comfortable lifestyle for an owner-operator, but it doesn't fit DSO underwriting models. Those practices still transact—they just transact with independent buyers who evaluate deals differently.

DSOs prioritize growth potential over current performance. They'll pay premium multiples for practices with untapped revenue opportunities—underutilized operatories, low hygiene recall rates, or markets with demographic tailwinds. If a practice is already optimized and running efficiently under the current owner, the upside DSOs need to justify their offer often isn't there. Independent buyers can succeed by maintaining what's already working rather than needing to extract additional growth to hit return targets.

If you're evaluating a practice and wondering whether a DSO will enter the picture, start by pulling three years of financial statements and calculating normalized EBITDA. If the practice sits below $1.2 million in revenue or operates under 20% EBITDA, DSO competition is unlikely. If it's a single location in a market where DSOs have no regional presence, that further reduces the risk. And if the practice's value comes from the owner's clinical reputation rather than operational systems that transfer easily—something buyers often miss when evaluating a practice—DSOs typically pass.

How to Position Yourself as the Stronger Buyer

With that understanding of where you actually face DSO competition, the most effective way to compete is to remove uncertainty before you make an offer. Sellers evaluate buyers on two dimensions: what they're offering and whether they can actually close. The second dimension matters more than most buyers realize.

Secure SBA pre-approval or a bank financing commitment before you start making offers. This isn't about having cash in hand—it's about demonstrating that you've already cleared the financing hurdle and the only remaining variable is the practice itself. Most dental associates carry significant student loan debt, and sellers know this. When you present a pre-approval letter alongside your offer, you're signaling that lenders have already underwritten your financials and committed capital.

Many buyers treat financing as something they'll figure out after the seller accepts their offer. By that point, the seller has already taken the practice off the market, turned down other buyers, and committed to your timeline. If your financing falls through—or takes longer than expected—the seller either restarts the process or accepts a backup offer at a lower price. Getting pre-approved early tells the seller you're serious and capable.

Independent buyers can close in 60-90 days with minimal complexity. DSO deals often take four to six months, with extensive due diligence, corporate approvals, and legal reviews that introduce delays and contingencies. When presenting your offer, frame this as a concrete benefit: "I'm pre-approved and ready to close within 75 days, with no corporate approvals or multi-party negotiations required."

Connect with the seller's motivations beyond price. Most sellers care deeply about what happens to their staff, patients, and practice reputation after they leave. Ask about their vision for the practice's future. What do they want to see preserved? Are there staff members they're particularly concerned about? When you show genuine interest in these concerns—and explain how your ownership aligns with their goals—you're competing on dimensions where DSOs can't match you.

Bridge valuation gaps through creative deal structures. Partial seller financing, transition consulting fees, or performance-based earn-ups allow you to increase the total purchase price while keeping your upfront capital requirement manageable. A seller who receives $800,000 at closing plus $200,000 in seller financing over three years often prefers that structure to a DSO offer of $1.1 million with $400,000 deferred and tied to production targets they no longer control. Your structure gives the seller a secured note with predictable payments, while the DSO structure ties payment to metrics the seller can't influence post-sale.

Present yourself as a long-term owner invested in the community, not a corporate entity optimizing for portfolio returns. Sellers respond to buyers who plan to stay, grow roots, and build on what they started. If you're moving to the area, talk about why. If you have family nearby or connections to the community, mention that. These details signal commitment in ways that corporate acquisition teams cannot replicate.

The reality is that most buyers transition faster than they expect once they understand the financing options available and start positioning themselves strategically. When you position yourself as the stronger buyer, you're not trying to outbid DSOs. You're showing sellers that what you offer—certainty, simplicity, cultural alignment, and a clean exit—is exactly what they want once they understand the full picture.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Private Buyer Sale VS. DSO Affiliation: Pros & Cons— dentaltransitions.comIndustry

- Why Independent Buyers Aren't Really Competing Against DSOs— nxlevelconsultants.comIndustry

- Dental Practice EBITDA - FOCUS Investment Banking— focusbankers.comIndustry

- The Truth about Dental Practice Loans— ada.orgIndustry

Frequently Asked Questions

Don't Let DSOs Win Your Practice

Competing with DSO offers doesn't mean accepting less than you deserve. Minty Plus connects you with independent buyers who can match or exceed DSO terms while preserving your practice's independence and culture.