Accounts Receivable Disputes After Buying a Dental Practice

Co-Founder, Minty Dental

In Summary

- Dental practice accounts receivable (AR) is always negotiated separately from the purchase price — how you structure the AR deal shapes nearly every dispute that can arise after closing

- There are two main structures: the buyer purchases AR outright, or the seller retains AR while the buyer collects on their behalf, typically for a 5% fee

- A healthy AR balance should not exceed one month's average collections — balances significantly above this threshold are a due diligence flag worth investigating before you sign anything

- Most post-closing AR disputes trace back to vague or missing contract language, not bad faith — your attorney and CPA are your first line of defense

- Catching AR problems before closing is far easier than resolving them after — the contract negotiation phase is where buyers have the most leverage

AR Disputes Are a Post-Closing Problem You Can Mostly Prevent Before Closing

Dental practice accounts receivable is the total of outstanding balances owed by patients and insurance companies for services already performed — money the practice has earned but not yet collected. It is always negotiated separately from the purchase price, and how that negotiation goes will determine which disputes are even possible once the deal closes.

Most buyers encounter AR for the first time as a line item in the purchase agreement and treat it as a detail to sort out later. What tends to happen instead is that "later" arrives quickly — usually within the first 90 days of ownership — in the form of insurance payments landing in the wrong account, patients receiving duplicate bills, or collections on old balances stalling with no clear owner. By that point, the leverage to fix things cleanly is largely gone.

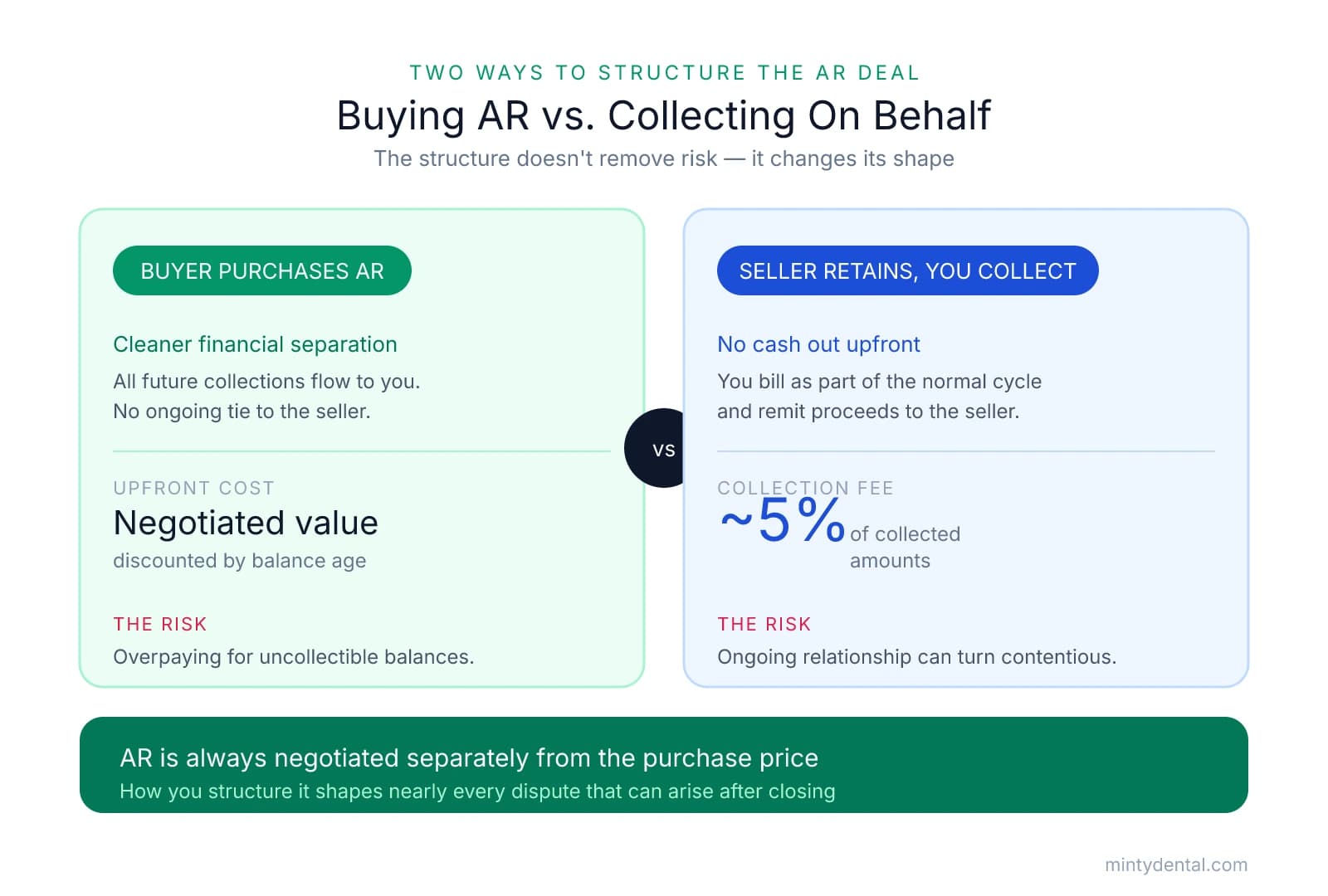

The two structures every buyer should understand:

-

Buyer purchases AR outright. You pay the seller a negotiated value for the outstanding portfolio — typically discounted based on age — and all future collections flow directly to you. This creates a cleaner financial separation but introduces the risk of overpaying for balances that turn out to be uncollectible.

-

Seller retains AR, buyer collects on their behalf. The seller keeps ownership of the outstanding balances, and you collect them as part of your normal billing cycle, remitting proceeds to the seller minus a collection fee — typically around 5%. This avoids upfront cost but creates an ongoing administrative relationship with the seller that can become contentious if expectations aren't documented precisely.

The structure you choose doesn't eliminate risk — it just changes the shape of it. Buying AR removes the entanglement of a post-closing financial relationship with the seller, but it means your due diligence on the portfolio's quality needs to be rigorous. Not buying AR keeps cash out of the deal upfront, but vague collection agreements are a common source of post-closing friction that can strain an otherwise smooth transition.

A benchmark worth applying immediately: according to EisnerAmper, total AR should generally not exceed one month's average collections, though this can vary by specialty and insurance mix. A balance significantly above that threshold isn't automatically disqualifying, but it warrants a direct conversation with the seller about why — slow insurance reimbursement, extended patient credit terms, and lax collections processes all tell different stories about what you'd be inheriting.

The core insight that runs through every section of this guide: most post-closing AR disputes don't start after closing. They start during due diligence, when the right questions weren't asked, or during contract drafting, when the right language wasn't included. Your attorney and CPA aren't just advisors here — they're your primary protection against disputes that are genuinely difficult to unwind once ownership has transferred.

How to Audit the AR Before You Close — and What Red Flags Actually Mean

The AR aging report is the single most important document you'll review during due diligence — and also one of the easiest to misread. Knowing what to request, and what to look for once you have it, is where buyers tend to separate themselves.

Start With the Right Request

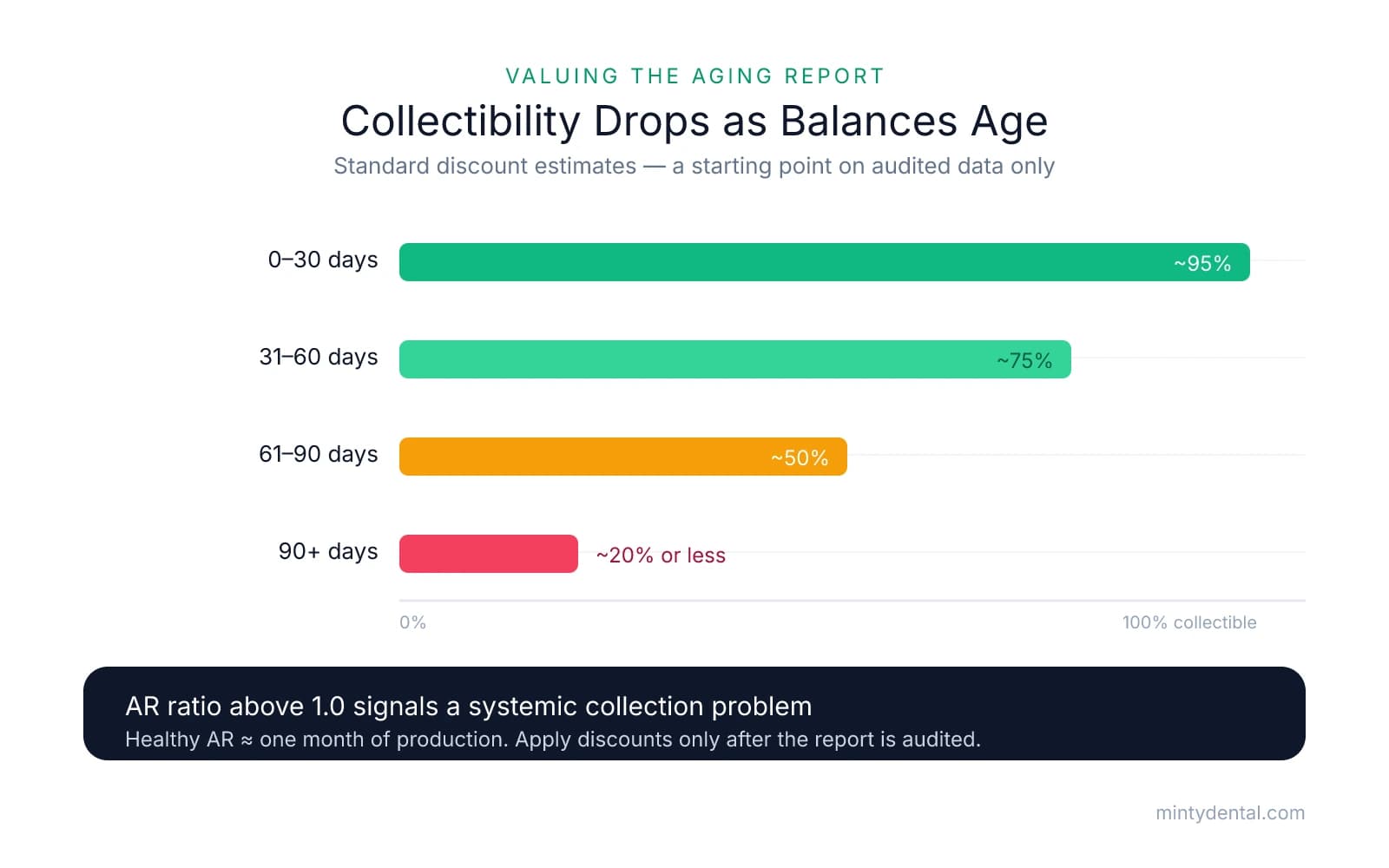

Ask for AR aging reports broken into standard buckets: 0–30 days, 31–60 days, 61–90 days, and 90+ days. Then ask for reports from multiple dates — ideally three to six months apart — not just a single snapshot. A one-time report tells you what the AR looks like today. A series of reports tells you whether the picture is consistent, or whether balances are being managed to look favorable ahead of a sale.

The Hidden Manipulation Risk

One pattern worth understanding before you sit down with those reports: billing software often retains insurance AR in the 0–30 day bucket even after 30 or more days have passed. Separately, some sellers post charges without applying the corresponding PPO or insurance contractual adjustments — which inflates the apparent current balance. Neither of these is necessarily intentional, but both make the portfolio look cleaner than it is. According to Dental CPAs, this exact combination caused one buyer to significantly overpay for AR they assumed was current — a mistake that only became visible months after closing.

The Standard Discount Table — and Why It's a Starting Point, Not a Formula

Once you have a verified, audited aging report, standard valuation discounts give you a working framework:

| Aging Bucket | Standard Collectibility Estimate |

|---|---|

| 0–30 days | ~95% |

| 31–60 days | ~75% |

| 61–90 days | ~50% |

| 90+ days | ~20% or less |

The critical word is audited. Applying these percentages to raw report figures — before cleaning up the data — is where many buyers overpay. Before you run the math, remove accounts that distort the picture: neighbor or friend balances that may never be collected, duplicate entries, patient credits sitting as positive balances, and very old accounts the seller has simply never written off.

The AR Ratio Check

One calculation worth running early is the AR ratio: total AR divided by average monthly production. As Duckett Ladd notes, a healthy practice typically carries an AR ratio around 1.0 — meaning total receivables roughly equal one month of production. A ratio significantly above 1.0 usually signals a systemic collection culture you'd be inheriting, not just a few slow insurance claims. The relationship between collections and production is worth examining alongside this ratio — a practice with strong production but weak collections is a different acquisition than it first appears.

Ask About the Large Individual Balances

For any balance over 90 days, ask the seller to explain it directly. The answer — whether it's a disputed insurance claim, a payment plan, a family member's account, or simply an account no one followed up on — tells you as much about the practice's operational culture as the number itself. Sellers who can't explain their own aged balances are revealing something important about how the practice has been managed.

The Contract Language That Prevents Most Post-Closing AR Disputes

Once you've audited the AR and understand what you're inheriting, the next job is making sure the purchase agreement actually reflects that understanding. The asset purchase agreement is the document every party will reach for if a dispute arises — which means vague or missing AR language isn't just an inconvenience. It's the root cause of most post-closing conflicts.

Five specific provisions, negotiated before signing, cover the vast majority of scenarios where buyers and sellers end up in conflict.

1. The Collection Period Six months is the accepted industry standard for how long a buyer collects on the seller's behalf. Equally important — but less commonly negotiated — is what happens at the end of that window. Any remaining uncollected seller AR should revert to the buyer, not back to the seller. When sellers retain the right to pursue their own old balances, patients often receive aggressive collection calls from someone they no longer have a relationship with — a patient retention problem that lands on you.

2. FIFO Payment Allocation When a patient owes balances to both the seller (pre-closing) and you (post-closing), payments should be applied to the oldest balance first. This is standard practice, but it must be written explicitly into the agreement. Without that language, disputes over payment allocation are almost inevitable with patients who carry balances across the transition date.

3. Admin Fee for Collection Services A fee of 5% of collected amounts is the accepted norm for the administrative work of billing and remitting on the seller's behalf, as Dental CPAs notes. If the portfolio skews heavily toward older balances or complex insurance claims, negotiating that fee to 7–10% is reasonable — the harder the portfolio is to work, the more your time and staff resources are worth.

4. Patient Credits The cleanest structure is a check from the seller to the buyer at closing equal to all outstanding patient credits. This keeps you in control of those funds and turns a potential liability into a patient relationship opportunity — you can reach out to patients with credits and introduce yourself as the new owner at the same time.

5. Sunset Clause for Stale AR Seller AR older than 12–24 months should automatically revert to the buyer for nominal consideration — typically $1 — rather than remaining an active collection obligation. Without this clause, a seller can technically contact patients years after closing to pursue old balances. If the deal involves a meaningful escrow holdback, understanding how holdback structures interact with AR reversion timelines is worth a conversation with your attorney before finalizing terms.

These provisions aren't demands to issue — they're standard protections that experienced dental transaction attorneys negotiate routinely. A seller who pushes back hard on any of them is worth asking why.

When a Dispute Surfaces After Closing: How to Respond Without Escalating

Even with solid contract language in place, post-closing friction happens. Insurance payments land in the wrong account. A seller reaches out to a patient directly. Two parties read the same clause differently. What separates buyers who resolve these quickly from those who let them fester is usually how they respond in the first 48 hours.

The first move in any dispute is the same: pull the purchase agreement and find the AR provisions. Most conflicts have a contractual answer if the language was drafted clearly. Before sending any message to the seller, know exactly what the agreement says — because that document is what any mediator or attorney will reach for first.

A Decision Tree for the Four Most Common Scenarios

If an insurance check arrives at the wrong party's address: This is the most frequent post-closing friction point. The agreement should specify a forwarding protocol — in practice, a written acknowledgment and check forwarding within 5–7 business days resolves most of these without escalation. If no protocol exists, propose one in writing immediately and document every check that moves between parties.

If the seller is contacting patients directly about old balances: This is a goodwill risk that lands on you. Your tools are the collection period clause and the sunset provision. If those exist in the agreement, a written notice to the seller citing the specific language is usually sufficient to stop it. For broader context on managing a seller who remains too present after closing, the seller undermining you after closing framework applies here as well.

If there's a disagreement about which balance a patient payment should apply to: Look for the FIFO clause first. If it's there, the answer is already written. If it's missing, document every payment received since closing and propose a written allocation schedule to the seller before the disagreement hardens into a formal dispute.

If the seller claims you aren't collecting aggressively enough on their behalf: Pull your billing records and remittance history. If you've been following standard collection practices, that documentation is your defense. Most of these claims dissolve when the buyer can show a clear paper trail.

When the purchase agreement is silent or ambiguous, mediation is typically faster and cheaper than litigation for AR disputes of this size. Most dental-specific attorneys can facilitate this without going to court — and the cost of a few hours of mediation is almost always less than a prolonged dispute in terms of time, money, and mental energy. Attorneys who work specifically in dental practice sales note that ambiguous contract terms are among the most common sources of post-closing conflict they see.

One instinct worth resisting: paying the seller a small amount just to make the conflict go away. It's completely understandable — you're running a new practice, managing staff, and building patient relationships simultaneously. But settling without documentation can establish a precedent that invites future claims. Whatever the amount, put the resolution in writing.

The patients caught in the middle of a billing conflict are the same patients whose loyalty makes the practice worth owning — and how this transition is managed is often the first impression you leave with them.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Accounts Receivable negotiations Buying a Dental Practice— www.eisneramper.com

- Dental CPA Q&A: Should I Buy the Accounts Receivable?— dentalcpas.comIndustry

- Financial Due Diligence for Dental Practices— duckettladd.comIndustry

- Navigating Dental Practice Sales Transactions: What You Need to ...— www.youtube.com

Navigate AR Challenges When Buying Dental

Accounts receivable disputes can derail your practice acquisition. Minty's operations team handles billing complexities and AR management, so you can focus on patient care from day one.