SBA Loan vs Conventional Loan for Dental Practice Buyers

Co-Founder, Minty Dental

In Summary

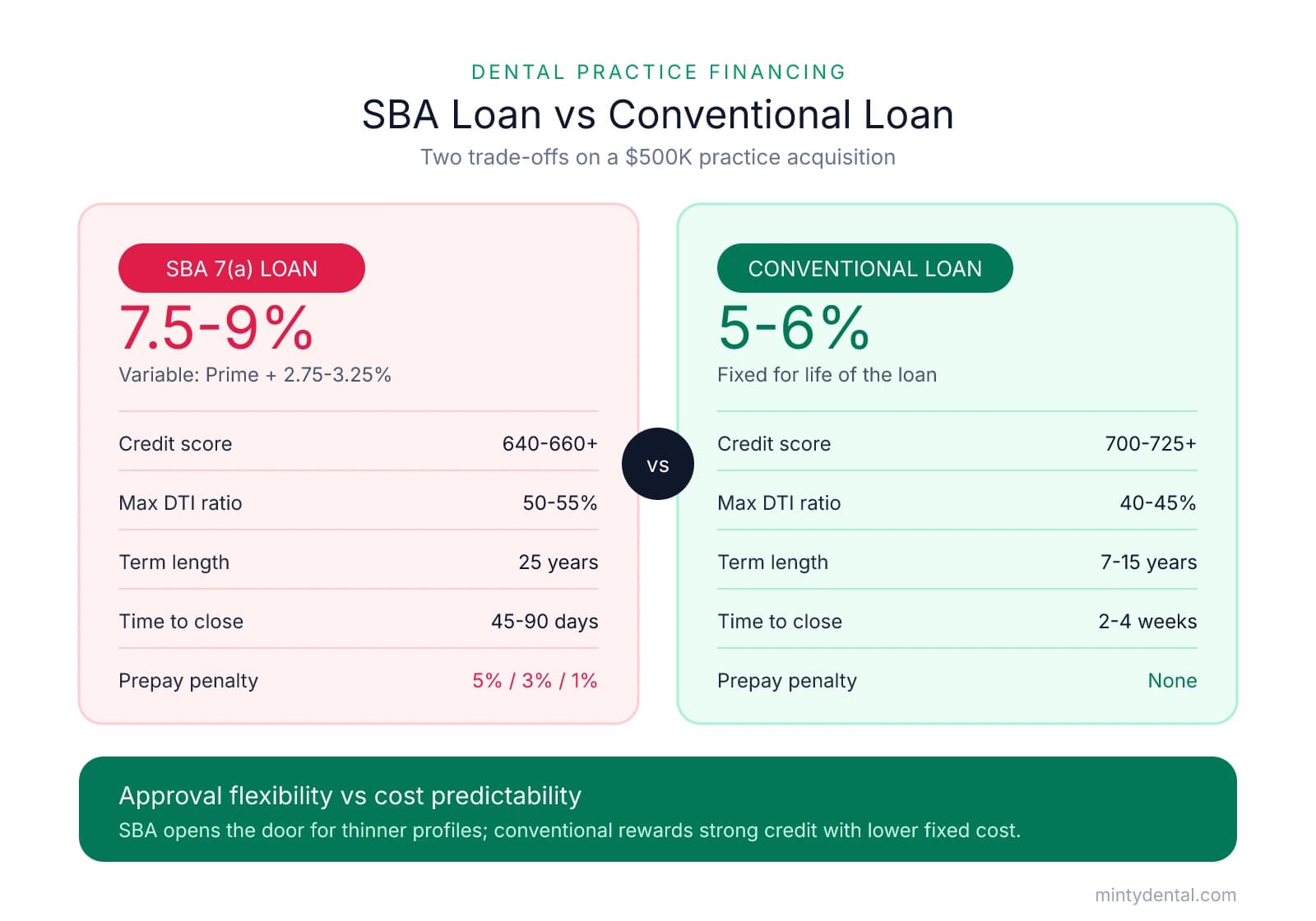

- SBA loans carry variable rates of Prime + 2.75-3.25% (currently 7.5-9%), while conventional loans offer fixed rates around 5-6%—the difference costs roughly $200,000 more in total interest on a $500K loan over 25 years

- SBA loans accept credit scores as low as 640-660 and accommodate higher debt-to-income ratios, while conventional loans typically require 700-725+ and stronger financial profiles

- Variable rates create cash flow uncertainty that affects budgeting in the first 2-3 years when margins are tightest, while fixed rates lock in predictable payments for the life of the loan

- Conventional loans close in 2-4 weeks with no prepayment penalties, while SBA loans require 45-90 days and charge 5%/3%/1% penalties in years 1-3

- The choice isn't about which loan is better—it's about which trade-off matches your financial position, risk tolerance, and timeline for ownership

The Core Trade-Off: Rate Predictability vs Approval Flexibility

The financing decision for most dental practice buyers comes down to a single question: do you optimize for approval flexibility or long-term cost predictability? SBA loans and conventional loans exist because they solve different problems—one prioritizes access for buyers with thinner credit profiles or higher debt loads, the other rewards stronger financial positions with lower, fixed-rate financing.

SBA loans optimize for approval flexibility. They accept credit scores as low as 640-660, accommodate higher debt-to-income ratios, and work with buyers carrying significant student loan balances. The trade-off is a variable rate structure—currently Prime + 2.75-3.25%, landing between 7.5-9%—that shifts with market conditions.

Conventional loans optimize for cost predictability. They offer fixed rates around 5-6%, which means your monthly payment stays constant for the life of the loan. But approval standards are stricter—most lenders require credit scores of 700-725+, lower debt-to-income ratios, and stronger liquidity reserves.

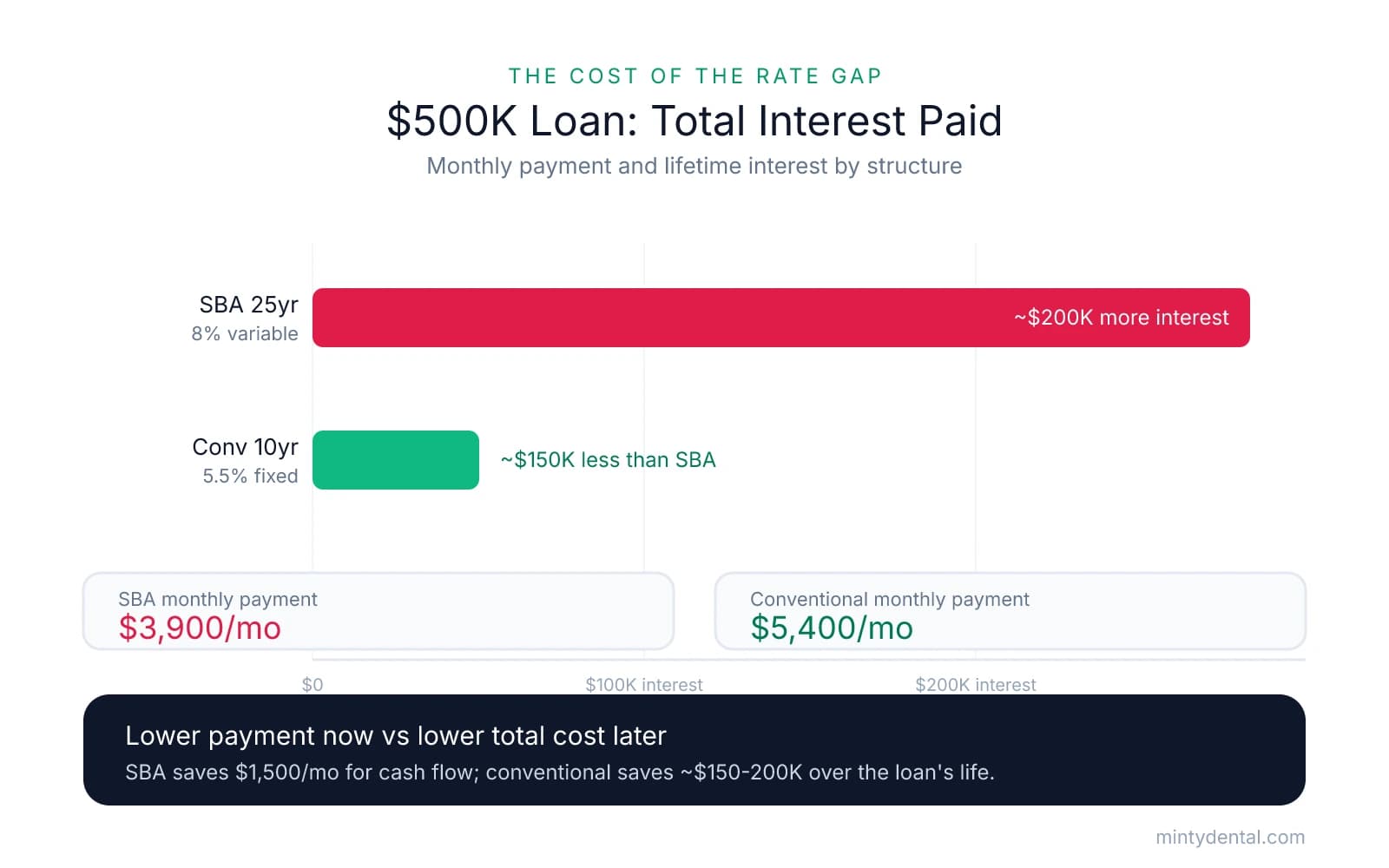

The rate difference compounds significantly over time. A $500,000 loan at 8% costs roughly $200,000 more in total interest over 25 years compared to the same loan at 5.5%, per Bank of America's refinancing analysis. That's the equivalent of an associate's annual salary or a major equipment upgrade.

Variable rates also introduce cash flow uncertainty that affects budgeting, especially in the first 2-3 years when margins are tightest. If Prime rises 1-2%, your monthly payment increases by several hundred dollars—manageable for an established practice, but harder to absorb when you're still stabilizing patient flow. Fixed-rate conventional loans eliminate that risk entirely.

Both loan types can finance 100% of the purchase price plus working capital, so down payment requirements aren't the differentiator. The real question is whether your credit profile and debt load give you a choice. If your credit score sits above 700 and your debt-to-income ratio is manageable, conventional financing may save you six figures over the loan's life. If your credit score is below 680 or you're carrying $400K+ in student loans, SBA may be your only realistic path to ownership—and that's a perfectly viable one.

When SBA Loans Make Sense: Lower Barriers, Longer Terms, Higher Cost

SBA 7(a) loans exist because they solve a specific problem: they enable practice ownership for buyers who wouldn't qualify under conventional underwriting standards. The government guarantee—covering 75-85% of the loan amount—absorbs enough lender risk that banks can approve buyers with credit scores in the 640-660 range, higher debt-to-income ratios, and limited liquidity reserves.

The most immediate advantage is the 25-year term for practice acquisitions. Conventional loans typically cap at 10-15 years, which means higher monthly payments on the same principal. Spreading a $500,000 loan over 25 years instead of 10 can reduce your monthly payment by $2,000-3,000, which matters significantly when you're managing first-year cash flow alongside student loan obligations.

SBA loans work particularly well in three scenarios:

-

Your credit score sits between 640-700. Conventional lenders typically require 700-725+ for practice acquisition loans. SBA-approved lenders can work with scores as low as 640, though rates and terms improve as you approach 680.

-

Your debt-to-income ratio exceeds conventional thresholds. Most conventional lenders cap total debt service at 40-45% of gross income. SBA lenders can stretch to 50-55% when the practice's cash flow supports it.

-

The practice has characteristics conventional lenders flag as risky. Practices with heavy Medicaid patient mixes, older patient demographics, or seller transition concerns often struggle to secure conventional financing. SBA lenders evaluate these risks differently because the government guarantee reduces their exposure.

The trade-offs are real. SBA loans carry prepayment penalties—5% in year one, 3% in year two, 1% in year three—which limits your ability to refinance if rates drop. Most SBA loans also require personal collateral, often your home, which means you're pledging assets beyond the practice itself. Approval timelines run 45-90 days due to SBA documentation requirements, which can complicate deals where the seller expects a faster close.

The longer term and lower monthly payment structure makes SBA loans particularly valuable when you need to preserve first-year cash flow. A $2,500 lower monthly payment gives you $15,000 more liquidity in the first six months—enough to cover a hygienist's salary or replace a failing compressor without tapping personal savings.

If multiple banks have already declined your application, SBA financing is worth exploring before assuming ownership isn't realistic. The government guarantee exists specifically to enable small business ownership for buyers who don't fit traditional lending profiles.

When Conventional Loans Win: Speed, Stability, and Lower Total Cost

Conventional dental practice loans reward strong financial profiles with three advantages that compound over time: fixed rates that eliminate interest rate risk, approval timelines measured in weeks rather than months, and significantly lower total interest paid.

The fixed-rate structure is the most immediate benefit. Most specialized dental lenders currently offer rates between 5-6%, locked for the life of the loan. That means your monthly payment in year one is identical to your payment in year ten, which simplifies cash flow forecasting and eliminates the risk of rate spikes during economic uncertainty.

The rate difference translates to substantial savings. A $500,000 loan at 5.5% over 10 years costs roughly $150,000 less in total interest compared to a 25-year SBA loan at 8%, per Bank of America's refinancing analysis. Even if you plan to refinance or sell within 5-7 years, the lower rate saves you $40,000-60,000 in interest during that window.

Approval timelines run 2-4 weeks with specialized dental lenders who understand practice cash flow, patient retention patterns, and equipment valuation. Lenders like Bank of America Practice Solutions, Wells Fargo Practice Finance, and US Bank have dedicated dental acquisition teams that don't need to educate themselves on industry-specific metrics. Where SBA loans require 45-90 days, conventional lenders can move from application to closing in under a month when the buyer's financial profile is clean.

That speed matters in competitive markets where sellers receive multiple offers. A buyer who can close in 30 days with conventional financing has a structural advantage over a buyer requiring 60-90 days for SBA approval—especially when the seller is motivated to transition quickly or concerned about patient attrition during a prolonged sale process.

Conventional loans typically don't require personal collateral beyond the practice assets themselves. Where SBA loans often pledge your home or other real estate, conventional lenders rely on the practice's cash flow and equipment value to secure the loan. That means your personal residence isn't at risk if the practice underperforms.

No prepayment penalties means you can pay down principal aggressively without penalty, refinance if rates drop further, or pay off the loan entirely if you sell the practice earlier than planned. That flexibility doesn't exist with SBA loans, where prepayment penalties in the first three years can cost $15,000-25,000 on a $500,000 loan.

The shorter term options—typically 7-15 years—build equity faster and reduce total interest paid, but they do require higher monthly payments. A 10-year loan at 5.5% on $500,000 carries a monthly payment around $5,400, compared to $3,900 for a 25-year SBA loan at 8%. That $1,500 monthly difference is significant, but many buyers with strong cash flow prefer to pay down debt faster and own the practice outright within a decade.

Where conventional loans struggle is with buyers carrying heavy student debt loads or practices that don't meet traditional underwriting criteria. If your debt-to-income ratio exceeds 45% or the practice has characteristics lenders flag as risky—high Medicaid mix, aging patient base, seller transition concerns—conventional financing may not be available regardless of your credit score.

For buyers who qualify, conventional financing delivers predictability, speed, and lower total cost. If interest rates drop further, you can refinance without penalty. If cash flow exceeds projections, you can accelerate principal payments and own the practice outright years ahead of schedule.

How to Choose: Match the Loan to Your Profile and the Deal

The financing decision starts with an honest assessment of where you sit today—not where you hope to be in two years. Three variables determine whether you're choosing between loan types or whether the choice has already been made for you: your credit score, your debt-to-income ratio, and the timeline the deal requires.

If your credit score sits below 680 or your debt-to-income ratio exceeds 45%, start with SBA lenders who specialize in dental practice acquisitions. Conventional lenders typically won't approve buyers outside those thresholds regardless of how strong the practice looks. Banks like Live Oak Bank, Huntington Bank, and Celtic Bank have dedicated SBA dental teams that understand how to structure loans for buyers carrying $300K-400K in student debt.

If your credit score is 700+ and your total debt service stays below 40% of gross income, conventional loans typically save $100,000-200,000 over the loan's life compared to SBA financing. Specialized dental lenders like Bank of America Practice Solutions and Wells Fargo Practice Finance can pre-qualify you in 48-72 hours, which tells you immediately whether conventional financing is realistic.

Your timeline matters more than most buyers realize. If the seller has multiple offers and expects to close within 30-45 days, conventional loans move fast enough to meet that deadline—SBA underwriting typically requires 60-90 days. The two-week approval difference can be the factor that wins a competitive deal.

Consider your exit strategy before you sign loan documents. If you're buying a practice where you expect to sell within 5-7 years—either to relocate, upgrade to a larger practice, or transition to ownership of multiple locations—SBA prepayment penalties can cost $15,000-25,000 when you pay off the loan early. Conventional loans let you exit cleanly without penalty, which matters if your ownership timeline is shorter than the loan term.

Talk to both loan types early in your search—ideally before you make your first offer. Pre-qualification from a conventional lender tells you whether SBA financing is necessary or optional, which changes how you structure offers and negotiate timelines. Some buyers discover they qualify for conventional financing but choose SBA anyway because the longer term and lower monthly payment preserve first-year cash flow when margins are tightest.

One pattern worth noting: some buyers start with SBA financing to get into ownership, then refinance to conventional after 2-3 years once they've built practice equity and improved their debt-to-income ratio. After 24-36 months of on-time payments and practice cash flow that exceeds projections, refinancing to a fixed-rate conventional loan can save $80,000-120,000 in total interest over the remaining loan term. The SBA prepayment penalty in year three is only 1%, which makes refinancing economically viable if rates have dropped or your financial profile has strengthened significantly.

Get pre-qualified with both a conventional lender and an SBA specialist before you start making offers. That clarity changes how you evaluate practices, structure LOIs, and negotiate closing timelines—and it prevents you from losing a deal because you assumed one financing path was your only option.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Terms, conditions, and eligibility | U.S. Small Business Administration— www.sba.govGovernment

- Bank of America: Dental Practice and Commercial Real Estate ...— www.wsda.orgIndustry

- SBA 7(a) Loans for Dental Practice Acquisitions - Polished Legal— polishedlegal.comIndustry

- SBA vs. Traditional Lending for Dentists: Which Loan Fits the Need?— drilldownsolution.com

Frequently Asked Questions

Ready to finance your dental practice?

Whether you're comparing SBA loans or conventional financing, finding the right practice is the first step. Explore available dental practices nationwide and connect with acquisition experts who can guide you through every financing option.