What Banks Actually Look for When Financing a Dental Practice Buy

Co-Founder, Minty Dental

In Summary

- Dental lenders evaluate two separate files on every acquisition deal: your personal financial profile and the practice's financial profile — both must pass independently

- Dental practice loans default at under 1%, compared to 6–8% for general small business loans, which is why specialized lenders can offer 100% financing with no down payment required

- Specialized dental lenders treat goodwill, patient loyalty, and recurring revenue as real collateral — generic banks often don't understand this asset class

- Understanding both evaluation tracks before you apply helps you choose deals that are easier to finance and avoid surprises during underwriting

- Engaging a lender 1–2 years before you're ready to buy gives you time to strengthen your profile before a deal appears

Dental Lenders Run Two Files Simultaneously — Yours and the Practice's

Dental practice loan underwriting isn't a single credit check — it's two parallel evaluations running at the same time, and both files have to pass.

Most buyers walk into the process thinking about their credit score and debt load. Those things matter, but they're only half the picture. While a lender is assessing your personal financial profile, a second evaluation is happening simultaneously on the practice itself — its cash flow, revenue consistency, overhead structure, and patient base. A strong buyer profile won't save a deal built on a financially troubled practice, and a thriving practice won't compensate for a buyer whose personal finances raise red flags.

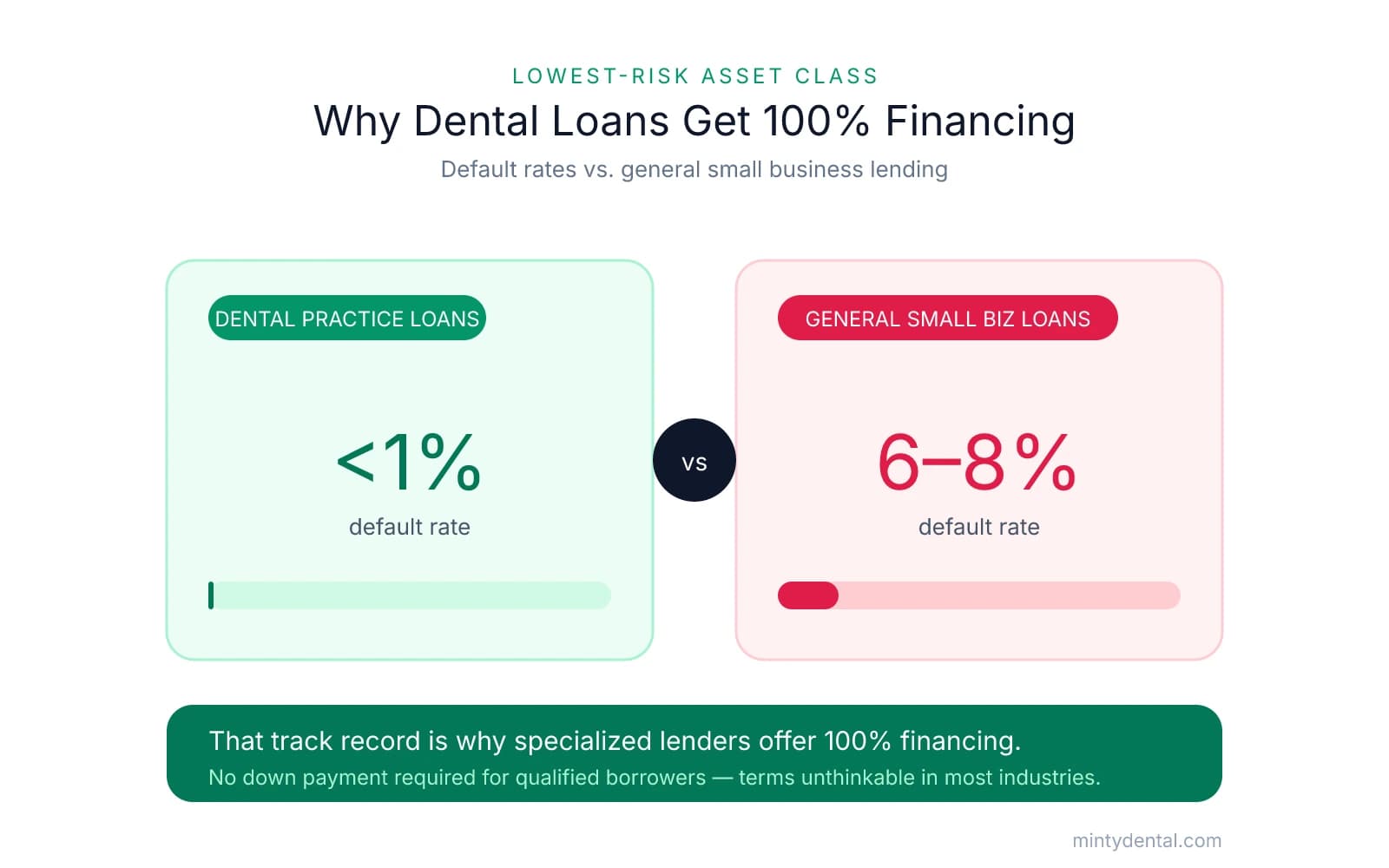

It's completely understandable to feel anxious about taking on significant debt after dental school. Many buyers carry six-figure student loans into this process and wonder whether ownership is even realistic. What tends to reassure people — once they understand the lending landscape — is that dental practices are genuinely one of the lowest-risk asset classes in all of small business lending. According to Bank of America Practice Solutions, dental practice loan default rates sit under 1%, compared to 6–8% across general small business lending. That track record is why specialized lenders exist, and why they can extend 100% financing with no down payment to qualified borrowers — terms that would be unthinkable in most other industries.

That specialization matters in another important way. Lenders like Bank of America Practice Solutions, Live Oak Bank, TD Bank Healthcare, and Provide have built underwriting models specifically for dental acquisitions. They understand that a practice's value isn't just its equipment or real estate — it's the goodwill, the patient relationships, and the predictability of recurring hygiene revenue. Generic banks often struggle to underwrite these intangibles, which is why buyers who approach a community bank without dental lending experience frequently run into friction or outright rejection. The decision of which loan structure fits your deal — conventional dental financing versus SBA — is worth understanding before you sit down with any lender.

The buyers who navigate this process most smoothly tend to share one habit: they engage a lender early — often 12 to 24 months before they're actively shopping. That timeline gives you room to identify gaps in your personal profile, understand what practice financials lenders want to see, and walk into a deal with a pre-qualification already in hand. When the right practice appears, speed matters, and buyers who've already had the lender conversation are in a fundamentally different position than those starting from scratch.

What Lenders See When They Look at You: The Buyer Profile

Most buyers assume the lender conversation starts and ends with their credit score. In practice, lenders are building a complete picture of who you are financially — and that picture is often more favorable than buyers expect.

Credit Score: The Floor, the Target, and What Actually Moves the Needle

The working threshold most dental lenders apply is a 680 credit score minimum, with 700+ typically unlocking better rates and smoother underwriting. If you're sitting between 680 and 700, you're not disqualified — but expect questions about what's dragging the number down.

The two factors that most reliably suppress scores are revolving debt utilization and payment delinquencies. A single 30-day late payment can follow a credit report for years and raises a specific concern for lenders: not just that you were short on cash, but that repaying obligations wasn't a priority. Both are worth addressing well before you apply.

Student loans are a different story entirely. As NDP Transitions notes, lenders familiar with the dental industry "consider student debt as productive and a career investment" — not a liability in the same category as consumer debt. A buyer carrying $300K in dental school loans is not viewed the same way as a buyer carrying $50K in credit card balances. If you've been hesitant about ownership because of your loan balance, the deeper picture on buying with significant student debt is worth understanding — the math tends to be more workable than it first appears.

| Debt Type | How Dental Lenders Treat It |

|---|---|

| Student loans | Expected; treated as productive career investment |

| Credit card balances | Scrutinized; high utilization is a yellow flag |

| Car loans / mortgages | Reviewed in context of income and overall DTI |

| HELOCs | Flagged if drawn heavily relative to income |

Liquidity: More Than a Down Payment Signal

Cash reserves communicate something beyond your ability to cover closing costs. Lenders read liquidity as evidence that you live within your means — and as a buffer if the practice underperforms in year one. The question of how much you actually need saved is more nuanced than a single number, but the principle is consistent: more available cash signals less risk, and that translates directly into rate and terms.

The Lifestyle-vs-Income Check

One area many buyers don't anticipate is the behavioral read lenders do on spending patterns. Interest-only mortgages, elevated credit card balances, or significant discretionary purchases made close to closing are yellow flags — not because any one of them is disqualifying, but because together they suggest a buyer who may struggle when practice cash flow is uneven in the early months. Dental lenders are specifically watching for lifestyle expenses that outpace income as a signal of financial discipline risk.

Professional Experience and Clinical Fit

Lenders also want confidence that you can perform the dentistry the practice generates. Production history, procedure mix, and years of associateship all factor in. A buyer whose clinical background aligns with the practice's revenue mix is a meaningfully lower risk than one who would need to refer out a significant portion of existing production.

One pattern worth noting: experienced dentists with weak personal financials often face more scrutiny than recent graduates. Lenders expect that someone ten years into their career has had time to build savings and reduce consumer debt — a thin financial profile at that stage raises more questions than the same profile would for a new graduate.

What Lenders See When They Look at the Practice: The Deal Profile

If the buyer profile is about trust — can this person handle debt responsibly? — the practice profile is about math. Lenders are asking one central question: does this practice generate enough cash flow to cover its own overhead, service the acquisition debt, and support the buyer's personal financial obligations, with room to spare?

The DSCR Threshold: The Number Every Deal Lives or Dies By

Debt Service Coverage Ratio (DSCR) is the core metric lenders use to evaluate practice cash flow. According to Bank of America Practice Solutions, lenders typically require a DSCR of at least 1.20x — meaning the practice must generate $1.20 in cash flow for every $1.00 in combined practice overhead and buyer personal debt service. Many lenders set the bar at 1.25x. Anything below that range, and the deal faces serious headwinds regardless of how strong the buyer profile looks.

What makes this calculation more nuanced is how lenders arrive at the cash flow number. They don't take the seller's reported income at face value — they normalize the financials by adding back discretionary or one-time expenses (charitable contributions, personal entertainment, owner perks, above-market compensation) to arrive at true adjusted cash flow. This process often improves the picture meaningfully, which is worth understanding before you assume a practice's numbers are too thin to finance.

Why Recent Trend Outweighs the Historical Average

A pattern that catches many buyers off guard: lenders weight recent performance far more heavily than multi-year averages. A practice that collected $1M annually for five years but dropped to $850K last year will face real scrutiny — even if the three-year average still looks healthy. As the section on collections vs. production explores, a declining trend in the last one to two years signals something lenders need explained: patient attrition, a departing associate, reduced hours, or early signs of a market shift.

Lenders don't finance potential. A practice that recently expanded or invested in new equipment won't receive credit for that investment until collections actually reflect it — and that gap is a risk lenders won't absorb on your behalf.

Practice Risk Factors That Shape Lender Confidence

Beyond the DSCR calculation, lenders are reading several qualitative signals:

- Staff tenure: Long-tenured staff correlates with patient retention stability. High turnover raises questions about practice culture and whether patients will follow the transition.

- Equipment age: Aging equipment signals near-term capital expenditure that will compress cash flow after closing.

- Seller transition plan: A seller who commits to a structured handoff — ideally 60–90 days with defined clinical responsibilities — reduces the risk that production walks out the door at closing.

- Procedure mix alignment: Lenders ask whether you can perform the dentistry generating the practice's revenue. A general dentist acquiring a practice with heavy implant or orthodontic production may face questions about whether that revenue is genuinely transferable — closely related to the clinical readiness question that shapes how lenders assess buyer fit.

A Quick Pre-Screen Framework

Before going deep on due diligence, run this four-point check to assess whether a practice is likely to be lender-friendly:

- Collections trend: Are the last two years flat or growing? A declining trend needs a clear, documentable explanation.

- Overhead ratio: Does overhead sit in the 55–65% range? Practices running above 70% leave little margin for debt service.

- Seller dependency: What percentage of production comes directly from the seller? High concentration is a transferability risk.

- Procedure mix fit: Can you perform — or credibly retain — the procedures driving top-line revenue?

If a deal clears these four filters, it's worth the deeper financial analysis. If it doesn't, understanding why a bank appraisal might come in below asking price becomes a very real conversation to prepare for.

How to Use This Framework Before You Make an Offer

The two-track structure covered here gives you something most buyers don't have going into their first lender conversation: a clear map of what's being evaluated and why. The practical question is how to use it before you're deep in due diligence on a specific deal.

Two Questions Worth Answering Before You Make Any Offer

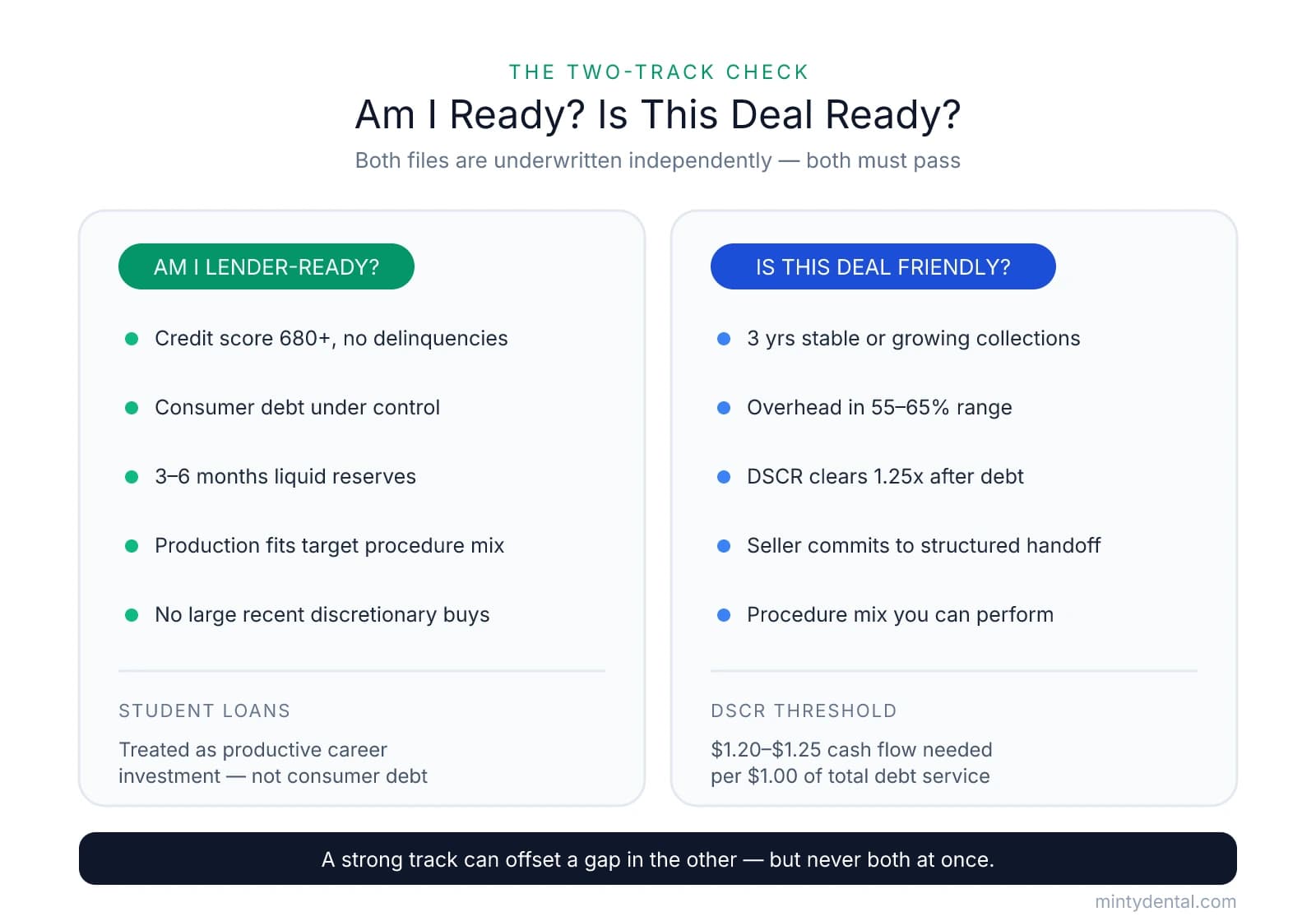

Run through both columns honestly. Weaknesses in one track don't automatically kill a deal — but they're worth knowing about before a lender finds them first.

Am I lender-ready?

- Credit score at or above 680, with no recent delinquencies

- Consumer debt (credit cards, HELOCs) under control relative to income

- 3–6 months of liquid reserves beyond closing costs

- Production history that aligns with the procedure mix of practices you're targeting

- No large discretionary purchases in the months approaching an application

Is this deal lender-friendly?

- Three years of stable or growing collections

- Overhead in the 55–65% range for a general practice

- A DSCR that clears 1.25x after your personal debt obligations are factored in

- A seller committed to a structured transition — not just a handshake agreement

- A procedure mix you can credibly perform or retain

If both columns are mostly green, you're in a strong position. If one has gaps, the question becomes whether the other track is strong enough to offset them. A buyer with thin liquidity may still qualify if the practice's cash flow is exceptionally strong. A practice with a recent collections dip may still be financeable if you can document the cause clearly — a temporary reduction in hours, a departing associate, a one-time disruption — and show that the trend has stabilized.

Get Pre-Approved Before You Start Searching

As both the ADA and Dental Buyer Advocates emphasize, pre-approval isn't just a formality — it's a competitive signal. Sellers and brokers take pre-approved buyers more seriously, and in multi-offer situations, financing readiness is a real edge.

Talk to at least three specialized dental lenders before committing to any one of them. Rates, terms, and risk appetite vary meaningfully across institutions, and the first offer is rarely the best. Starting those conversations 12–24 months before you plan to buy gives you time to address any gaps and builds a relationship that accelerates approval when the right deal appears.

Use the associate pay calculator to model whether your current income supports the liquidity and debt service thresholds lenders will evaluate — it's a useful reality check before you sit down with a bank. And if you've already been turned down, the path forward on a denied application is more navigable than it might feel in the moment.

The lender relationship you build now is a long-term asset. A lender who knows your profile, your goals, and your clinical background can move faster — and advocate harder internally — when the right practice appears.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Dental Practice Loans 2026: Lender Comparison + Rates [7-10%]— dentalpracticeinsider.orgIndustry

- What do lenders really look for in dental loans? - Instagram— www.instagram.com

- Buying a Dental Practice: Top Tips for a Successful Dental Practice ...— business.bankofamerica.comIndustry

- Talk to 3 Banks: The First Step in Buying a Dental Practice— ada.orgIndustry

- Financing a Dental Practice - Dental Buyer Advocates— www.dentalbuyeradvocates.comIndustry

Frequently Asked Questions

Ready to secure financing for your practice?

Understanding lender requirements is just the first step. Minty guides you through the entire acquisition process, from identifying the right practice to closing the deal with confidence and no upfront fees.