How Dental Practice Earnouts Work for Buyers

Co-Founder, Minty Dental

In Summary

- Earnouts defer 20-40% of the purchase price, paying it only if the practice hits specific targets over 12-36 months—letting you pay for verified performance rather than projections

- You control operations after closing, which means earnout achievement reflects decisions you make, not claims the seller made before the deal

- Revenue-based metrics are cleanest and hardest to dispute; EBITDA-based structures create more calculation fights unless exhaustively defined

- "Commercially reasonable efforts" language preserves your operational freedom; "best efforts" or "operate consistent with past practice" locks you into the seller's approach

- Shorter earnout periods (12 months), single end-of-term payments, caps/floors, and offset rights all reduce dispute risk and protect your investment

Earnouts Let You Pay for Performance You Can Verify

When a seller insists their practice is worth $1.2 million but trailing profit suggests $850,000, you face a choice: walk away or structure a deal where future performance settles the disagreement. An earnout does exactly that—it defers part of the purchase price and ties it to measurable results after you take over.

The basic structure: you pay a base amount at closing, typically calculated as a multiple of historical profit. The remaining 20-40% becomes contingent, paid only if the practice hits agreed targets over 12 to 36 months. If collections grow as promised, the seller gets paid. If they don't, you avoid overpaying for growth that never materialized.

Earnouts work best when uncertainty sits at the center of valuation. If 60% of production comes from the selling dentist and you're unsure how much transfers, an earnout lets you pay for retention you can measure. If the seller claims the practice is poised for growth but data shows flat collections, an earnout shifts the burden of proof. If the asking price assumes aggressive hygiene expansion that hasn't happened yet, you're not betting capital on optimism—you're structuring a deal where performance determines price.

Earnouts bridge valuation gaps by letting both sides agree on structure even when they disagree on value. The fundamental shift that makes this work: once you close, you run the practice. You decide staffing, scheduling, marketing, and protocols. The seller may stay on in a defined capacity, but you're paying for performance you influence, not projections you have to trust.

With operational control established, negotiating earnout terms becomes as important as negotiating the base price.

The Metrics That Determine Earnout Payments

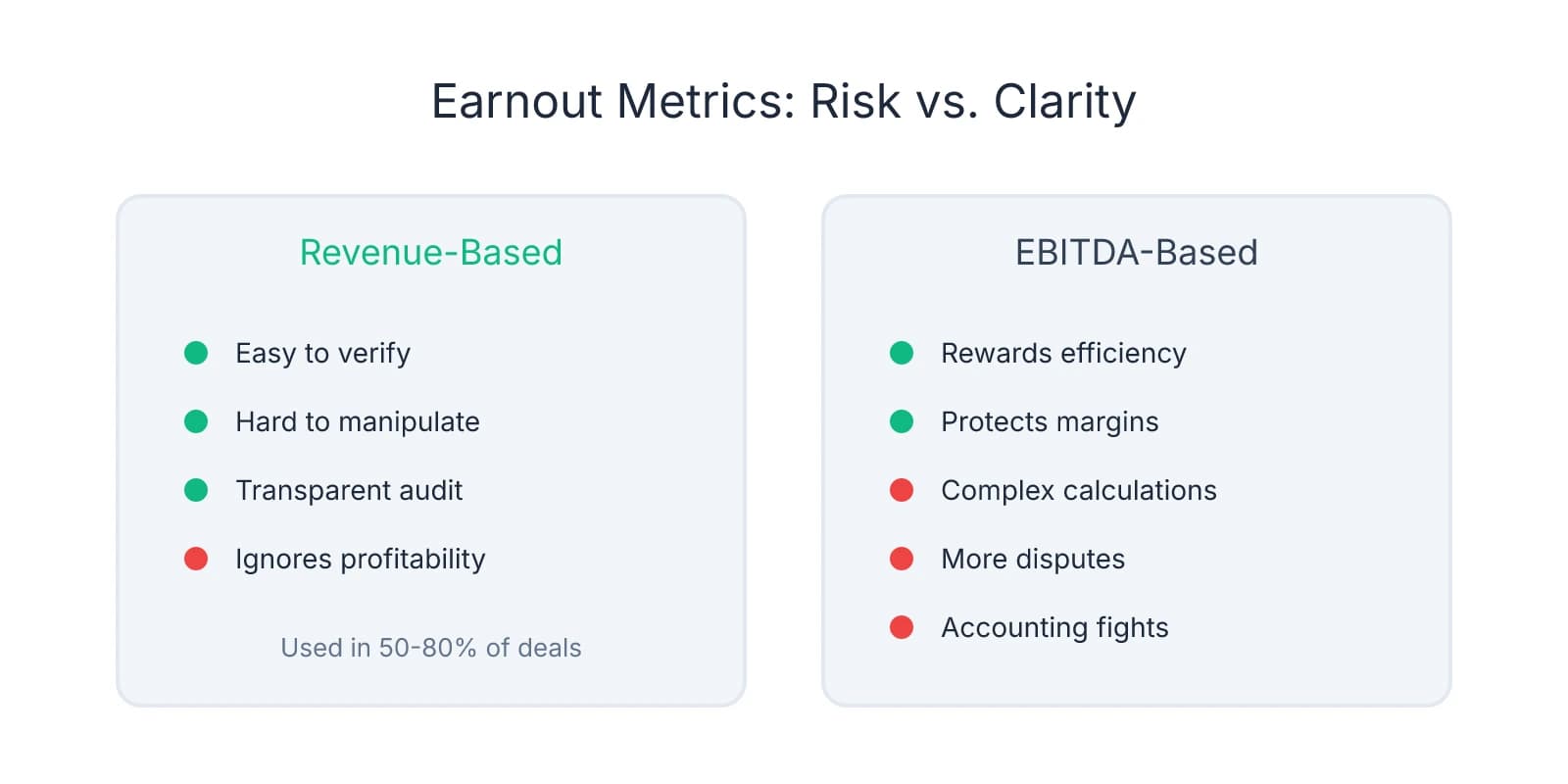

The metric you choose determines whether disputes arise 18 months later or whether both sides verify performance with a single spreadsheet. Revenue-based earnouts dominate because they're harder to manipulate and easier to audit—but each metric shifts risk differently.

Revenue or collections-based earnouts tie payments to top-line performance. If the agreement specifies "$300,000 contingent on annual collections exceeding $1.2 million," you pull deposit records, add up the numbers, and determine whether the threshold was met. This favors buyers because it's transparent and difficult to distort. The seller can't inflate it by cutting expenses; you can't suppress it by reallocating overhead. The tradeoff: revenue-based earnouts don't account for profitability changes. If collections hit target but you hired two additional hygienists to get there, the earnout pays out even though margins compressed.

Most earnouts in private M&A use revenue or EBITDA as the benchmark, with revenue-based structures appearing in 50-80% of contingent consideration agreements. The reason is simplicity—both sides verify the number without arguing over accounting methods.

EBITDA-based earnouts reward efficiency rather than just growth. If payments tie to adjusted profit, the seller benefits when you maintain margins, not just collections. This sounds appealing until you realize how many judgment calls go into calculating EBITDA. Do you allocate corporate overhead to the acquired practice? How do you treat one-time equipment purchases? What happens if you change the lab vendor and reduce COGS by 15%—does that count toward the earnout, or is it excluded as a post-closing operational change?

Disputes over expense allocation and accounting methods are the most common source of earnout litigation, and EBITDA-based structures create more of them than revenue-based ones. The buyer advantage: you control post-closing expense allocation, staffing levels, and capital investments that directly affect EBITDA.

Patient retention metrics protect against seller-dependent practices where relationships don't transfer. If 40% of active patients came specifically for the selling dentist, an earnout tied to retention rates ensures you're not paying full price for a patient base that evaporates. A retention-based earnout might specify: "Contingent payment of $200,000 if 75% of active patients schedule at least one appointment within 12 months of closing."

This works when verifying whether collections are sustainable is harder than verifying whether patients return. The risk: retention can be influenced by factors outside your control—insurance changes, local competition, or economic conditions. If using this metric, define "active patient" precisely (e.g., "patients with at least one visit in the 24 months prior to closing") and specify how you'll measure retention.

Production targets appear in deals where the seller stays on as an associate and continues producing. The earnout might specify: "Seller receives $100,000 if their personal production exceeds $400,000 in year one post-closing." This aligns incentives when the seller's clinical output is critical, but creates a different risk—you're now dependent on the seller's continued engagement, which limits operational flexibility.

Earnout disputes most often originate from vague language around calculation methods. If the agreement says "earnout based on EBITDA" without defining which expenses are included, how overhead is allocated, or what accounting standards apply, you're setting up a fight.

The protection is specificity. Define the metric with the same precision you'd use in a loan covenant. If it's revenue-based, specify whether you're measuring gross production, net collections, or adjusted collections after refunds and write-offs. If it's EBITDA-based, attach a schedule listing every expense category, how overhead will be allocated, and which accounting method applies. If it's retention-based, define the patient cohort, measurement period, and threshold for counting a patient as "retained."

The metric should match the uncertainty you're protecting against. If the risk is inflated projections, use revenue. If the risk is margin compression, use EBITDA but define it exhaustively. If the risk is patient attrition, use retention rates.

Operational Control: What You Can and Can't Do During the Earnout Period

The tension at the center of most earnout disputes isn't the metric—it's who controls the practice while it's being measured. You own the asset and want full discretion. The seller wants assurances you won't make decisions that tank their earnout. The language that resolves this determines whether you retain operational freedom or spend two years operating under constraints.

Most purchase agreements include operational covenants defining your obligations during the earnout period. The spectrum runs from "no specific commitments" (full discretion) to "commercially reasonable efforts" (operate in good faith but prioritize your business interests) to "best efforts" or "operate consistent with past practice" (constrained by how the seller ran the practice).

"Commercially reasonable efforts" is the standard that favors buyers. Courts interpret this as allowing decisions that serve your broader business interests, even if those decisions reduce earnout achievement. If you merge the acquired practice into your existing location during the earnout period and that temporarily disrupts collections, commercially reasonable efforts doesn't prevent you—it just requires you didn't act in bad faith or with specific intent to sabotage the earnout. When buyers commit to commercially reasonable efforts, they retain broad discretion, including strategic changes that may affect earnout metrics.

Under commercially reasonable efforts, you can reduce marketing spend if consolidating practices and shifting patient acquisition to a centralized budget. You can adjust staffing if patient volume doesn't support the existing team. You can defer equipment purchases if capital is better deployed elsewhere. These are normal operational choices.

"Best efforts" or "maximize earnout" language creates higher standards and more dispute risk. If the agreement requires you to "use best efforts to achieve earnout targets" or "operate the practice to maximize earnout payments," you're obligated to prioritize earnout achievement over your strategic interests. You can't reduce marketing spend even if inefficient. You can't adjust staffing even if patient volume drops. You can't integrate the practice if doing so might disrupt collections.

This doesn't just limit flexibility—it creates litigation exposure. If the earnout isn't achieved and the seller believes you didn't prioritize it, they'll argue you breached your obligation. The dispute becomes subjective, expensive, and distracting. If targets aren't met, you have to demonstrate you did everything possible to achieve them, not just that you operated in good faith.

"Operate consistent with past practice" is the most restrictive standard. This requires maintaining the same staffing levels, marketing budgets, clinical protocols, and operational structure the seller used. If they employed three hygienists, you can't reduce to two. If they spent $5,000 monthly on marketing, you can't cut it to $3,000.

The problem: this assumes the seller's operational decisions were optimal—and in most cases, they weren't. You bought the practice because you saw opportunities to improve efficiency, reduce overhead, or reallocate resources. "Operate consistent with past practice" prevents you from making those changes during the earnout period.

One protection many buyers overlook is the absence of explicit restrictions. Unless the purchase agreement specifically limits your operational discretion, you retain full control post-closing. Buyers typically maintain broad authority over business decisions unless the earnout agreement explicitly restricts them. If the agreement says nothing about staffing, you can adjust it. If it says nothing about marketing, you can reallocate the budget. If it says nothing about integration, you can merge the practice.

The seller will often request specific operational commitments to protect earnout achievement:

- Maintain staffing levels — "Buyer agrees to employ at least two full-time hygienists and one full-time front desk associate during the earnout period."

- Preserve marketing budgets — "Buyer agrees to spend no less than $4,000 per month on patient acquisition and retention marketing."

- Operate as a standalone entity — "Buyer agrees not to merge the acquired practice with any other dental practice or DSO entity during the earnout period."

- Maintain insurance participation — "Buyer agrees to remain in-network with all PPO plans the practice participated in as of the closing date."

Each commitment limits flexibility and transfers risk. If patient volume drops and you're locked into three hygienists, you're carrying excess labor cost. If marketing ROI deteriorates and you're required to maintain spend, you're burning cash on ineffective channels.

The commitments you should resist are ones that prevent responding to changing conditions. If the agreement locks you into specific staffing levels and patient volume drops 20%, you can't adjust. If it requires maintaining marketing spend and the local market shifts, you can't reallocate to more effective channels.

Where buyers get burned is accepting vague operational language that sounds reasonable but creates enforcement risk. "Buyer agrees to operate the practice in good faith" sounds harmless, but if earnout targets aren't met, the seller will argue any decision you made—staffing changes, marketing cuts, fee adjustments—violated good faith.

Unless the agreement explicitly restricts you, you retain broad discretion over operations post-closing. Courts generally hold that buyers are entitled to operate acquired businesses in ways that serve their strategic interests, even when those decisions affect earnout payments, as long as the buyer didn't act in bad faith or with specific intent to avoid the earnout.

Structuring Earnout Terms to Minimize Dispute Risk

The earnout terms you negotiate determine whether contingent payments function as intended or become a source of conflict. The structure—duration, payment timing, caps, offset rights, and dispute resolution—either protects your investment or creates ambiguity that leads to litigation.

Earnout duration directly affects uncertainty and seller involvement. Most dental practice earnouts run 12 to 24 months, with 12-month structures favoring buyers. The shorter the period, the faster you eliminate contingent liability. A 12-month earnout means calculating performance once, making a single payment, and closing the book. A 24-month earnout means two years of tracking metrics, maintaining documentation, and managing seller expectations.

Longer earnout periods create friction through extended seller involvement. If the earnout runs 24 months and the seller stays on as an associate, you're managing their engagement for two full years. If they lose motivation or reduce hours after the first year, earnout achievement becomes harder to predict. A 12-month period compresses that risk.

The tradeoff: shorter earnouts require higher thresholds to trigger payment. If measuring performance over 12 months instead of 24, the target needs to account for seasonal variation and ramp-up time.

Payment timing and frequency shift cash flow risk. You can structure earnout payments as a single lump sum at the end of the measurement period or as annual installments tied to interim milestones. A single payment at the end of a 24-month earnout means you're not making contingent payments until all performance data is in, reducing the risk of overpaying early. Annual payments mean making interim payments based on partial data, creating reconciliation risk if year two underperforms.

The payment structure that favors buyers defers the largest portion until the end of the measurement period. If paying $200,000 contingent on 24 months of performance, structure it as a single payment due 30 days after final calculation, not as two $100,000 payments at the end of year one and year two.

Caps and floors reduce dispute frequency and limit exposure. A cap sets the maximum earnout amount the seller can receive, even if performance exceeds targets. A floor sets a minimum threshold below which no earnout is paid. If collections need to exceed $1.2 million to trigger any payment, and actual collections come in at $1.15 million, the seller receives nothing. Floors eliminate small-payment disputes where the seller argues they came close enough to deserve partial payment.

Earnout agreements that include both caps and floors reduce post-closing disputes by eliminating ambiguity around payment amounts.

Offset rights let you deduct indemnification claims and working capital adjustments from earnout payments. If the seller breached a representation about accounts receivable and you're owed $40,000 in indemnification, offset rights allow you to deduct that amount from the next earnout payment rather than pursuing separate collection.

The language that protects buyers is explicit: "Buyer may offset any amounts owed to Buyer under the indemnification provisions, working capital adjustment, or any other claim arising under this Agreement against any earnout payment due to Seller."

Where offset rights matter most is in deals where working capital adjustments hit 90 days after closing and earnout payments come due 12 to 24 months later. If the working capital adjustment results in the seller owing you $30,000, and the first earnout payment is $100,000, offset rights let you pay $70,000 and close both obligations simultaneously.

Dispute resolution mechanisms determine how calculation disagreements get resolved. The cleanest structure specifies an independent accountant to review earnout calculations and resolve disputes, with both sides bound by the accountant's determination. If you calculate the earnout at $280,000 and the seller calculates it at $310,000, you submit both calculations to the independent accountant, who reviews the data and issues a binding determination within 30 days.

This avoids litigation and keeps disputes out of court. Independent accountant review is the preferred dispute resolution mechanism because it's faster, cheaper, and leverages expertise in financial calculations rather than legal arguments.

The language should specify what triggers independent review, who selects the accountant, what standard the accountant applies, and how fees are allocated.

Earnouts let you defer payment until performance is proven, but only if the terms protect your control and limit ambiguity. Shorter durations reduce uncertainty. Single payments at the end reduce cash flow risk. Caps and floors eliminate small disputes. Offset rights let you net obligations. Independent accountant review keeps disputes out of court. Each structural element shifts risk away from litigation and toward clean execution.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Earn-Outs in M&A: Key Deal Tool or Source of Post-Closing Disputes?— www.kroll.com

- Considerations for Earnouts in Acquisitions - BMO— commercial.bmo.comIndustry

- Buyer obligations in earnout negotiations - Hogan Lovells— www.hoganlovells.com

- Earnouts in M&A Transactions: Structuring, Risks, and Best Practices— lindenlawpartners.comIndustry

Frequently Asked Questions

Navigate Your Dental Practice Earnout Successfully

Understanding earnout structures is crucial when acquiring a dental practice. Minty Plus provides expert guidance through complex deal negotiations and post-close management to ensure you maximize your investment.