Insurance Credentialing Gap After Buying a Dental Practice

Co-Founder, Minty Dental

In Summary

- Insurance credentialing is tied to the individual dentist and the specific practice location — buying a fully credentialed practice does not transfer the seller's in-network status to you

- Even if you're already credentialed with a carrier at your current associate position, you must re-credential at the new practice address

- The typical credentialing timeline runs 60–90 days per carrier, with some taking up to 120 days

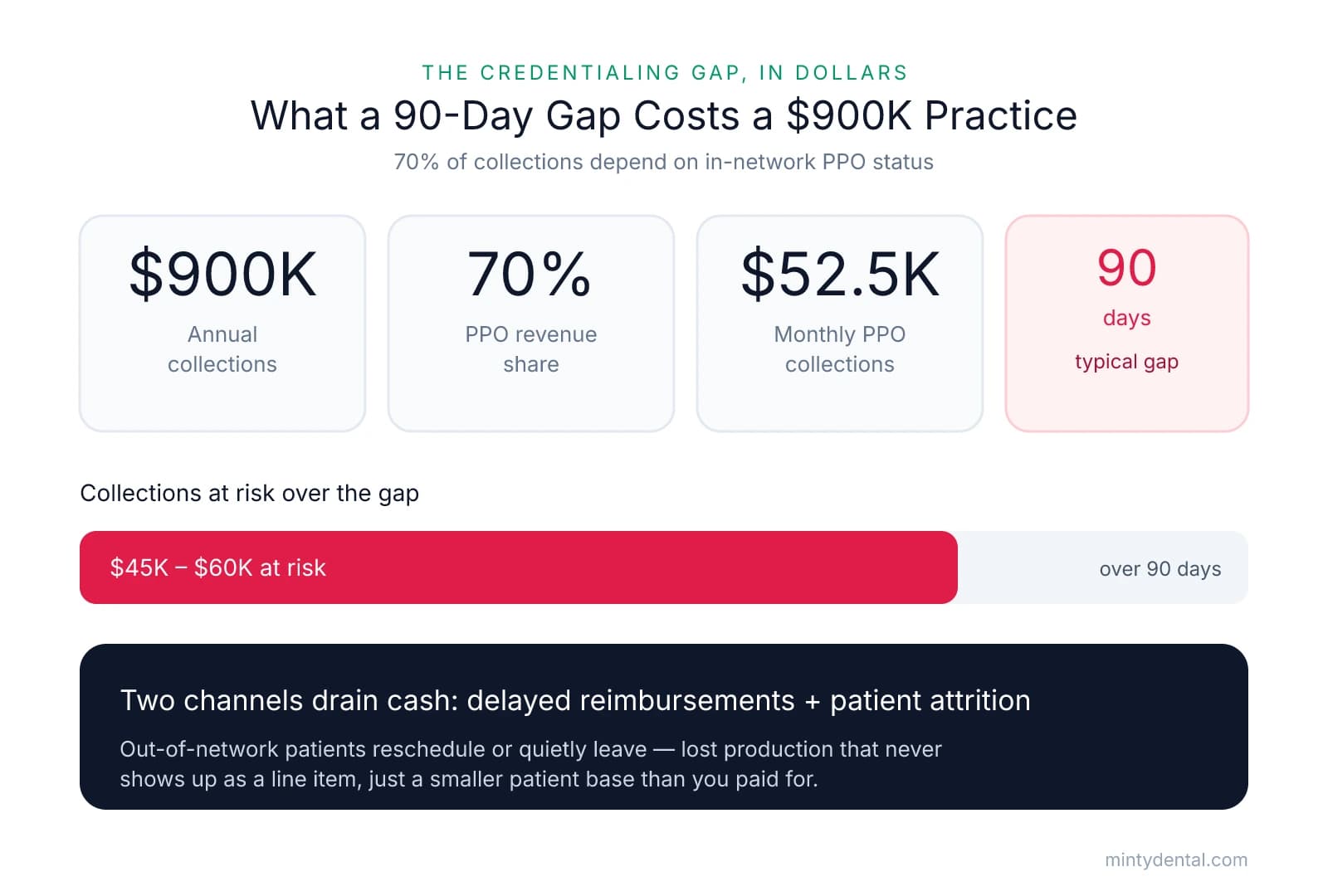

- For a practice collecting $900K/year with 70% PPO revenue, a 90-day credentialing gap can mean $45,000–$60,000 in delayed or reduced collections

- Buyers who plan for the gap before closing can manage it; buyers who discover it after closing are left absorbing the cash flow hit with few options

The Credentialing Gap Is a Cash Flow Problem, Not a Paperwork Problem

Most buyers spend months analyzing EBITDA, negotiating purchase price, and stress-testing loan scenarios — then discover, weeks after closing, that they can't bill insurance. Not because anything went wrong, exactly. Because nobody told them this was coming.

The credentialing gap defined: The credentialing gap is the period between the day you take ownership of a dental practice and the day you are fully approved as an in-network provider with each insurance carrier the practice participates in. During that window, you may be treating patients but unable to collect reimbursements at contracted in-network rates.

The foundational misunderstanding that creates this gap is worth stating plainly: credentialing is tied to the individual dentist and the specific practice location — not the practice entity. When you buy a fully credentialed practice, you are buying the equipment, the patient base, and the goodwill. You are not inheriting the seller's provider agreements. As American Practice Consultants notes, even if you're already credentialed with a carrier at your current associate position, you must re-credential at the new practice address. Delta Dental at your associate office and Delta Dental at your new practice are, from the carrier's perspective, two separate credentialing relationships.

That distinction has real dollar consequences.

What the gap actually costs: According to Overjet's 2025 practice revenue data, general dentistry practices collect between $65,000 and $120,000 per month. For a practice generating $900,000 annually with 70% of revenue tied to PPO patients, roughly $52,500 in monthly collections depends on in-network status. A 90-day credentialing gap — well within the typical 60–120 day processing window most carriers require — puts $45,000 to $60,000 in collections at risk.

The gap affects cash flow through two distinct channels:

- Delayed reimbursements: Patients pay out-of-pocket and wait for their carrier to reimburse them directly. Some do. Many don't return.

- Patient attrition: Insured patients told they'll be seen out-of-network often reschedule — or quietly find another in-network provider. That lost production doesn't show up as a line item; it shows up as a patient base that's smaller than the one you paid for.

This is also one of the unexpected expenses first-year owners consistently underestimate — not because the cost is hidden, but because it arrives before the practice has had any time to build reserves.

The buyers who navigate this well aren't the ones who move fastest at closing. They're the ones who started the credentialing conversation at the letter of intent stage — before the clock was already running.

The Billing Fraud Trap: Why You Can't Just Use the Seller's NPI

Given the cash flow pressure the credentialing gap creates, it's understandable that buyers look for a workaround. One "solution" comes up constantly in practice transitions: bill under the seller's NPI and Tax Identification Number until your own credentialing comes through. It sounds reasonable. It's sometimes written into purchase agreements. And it is insurance fraud — not a gray area, not a technicality.

Why it's fraud: When a claim is submitted under a provider's NPI, it represents to the insurance carrier that that provider rendered the care. If you performed the treatment but billed under the seller's credentials, the claim misrepresents the treating provider, misrepresents the contracted party, and may collect reimbursement at a fee schedule the buyer isn't entitled to. Each element independently constitutes a false claim.

What makes this particularly dangerous is where the advice originates. According to PPO Advisors — which has worked across 2,870+ dental practices and 12,000+ credentialing applications — brokers write grace period clauses into purchase agreements, attorneys sign off on them, and office managers are left holding the bag when it unravels. The myth circulates through trusted advisors, which is exactly why so many buyers encounter it without any alarm bells going off.

A purchase agreement clause cannot override insurance contract law. No matter what the document says, there is no grace period — not six months, not six weeks, not six days.

The one legitimate path through this: If the seller stays on as an employed associate after closing and is the actual treating provider, claims can legitimately be billed under the seller's credentials — because the seller is the one rendering care. This is structurally different from billing under the seller's name for work the buyer performed. It's also one reason negotiating meaningful seller transition support has value beyond patient retention: when the seller is present and treating, the practice can continue billing in-network while your own credentialing processes. Structuring that transition with defined clinical responsibilities and a realistic timeline protects both the billing relationship and the patient experience.

The stock purchase exception: In a stock purchase, the legal entity transfers intact, which means existing PPO contracts may carry over without re-credentialing. As Dental Practice Insider notes, roughly 95% of dental practice sales are structured as asset purchases — in part because buyers inherit unknown liabilities in a stock deal, and most lenders prefer the cleaner asset structure. The credentialing continuity is real, but most buyers and their lenders conclude the liability tradeoff isn't worth it. The question of whether to form an LLC before making an offer intersects with this decision, since entity structure choices made early in the process can affect what's available to you at closing.

For buyers who discover this issue post-closing without a seller transition arrangement in place, the practical reality is a period of treating insured patients as out-of-network — reduced reimbursements, awkward conversations at the front desk, and some patients who won't return. It's manageable, but far easier to manage when the plan is built before closing, not after.

A Pre-Closing Credentialing Checklist: What to Start at LOI, Not After Closing

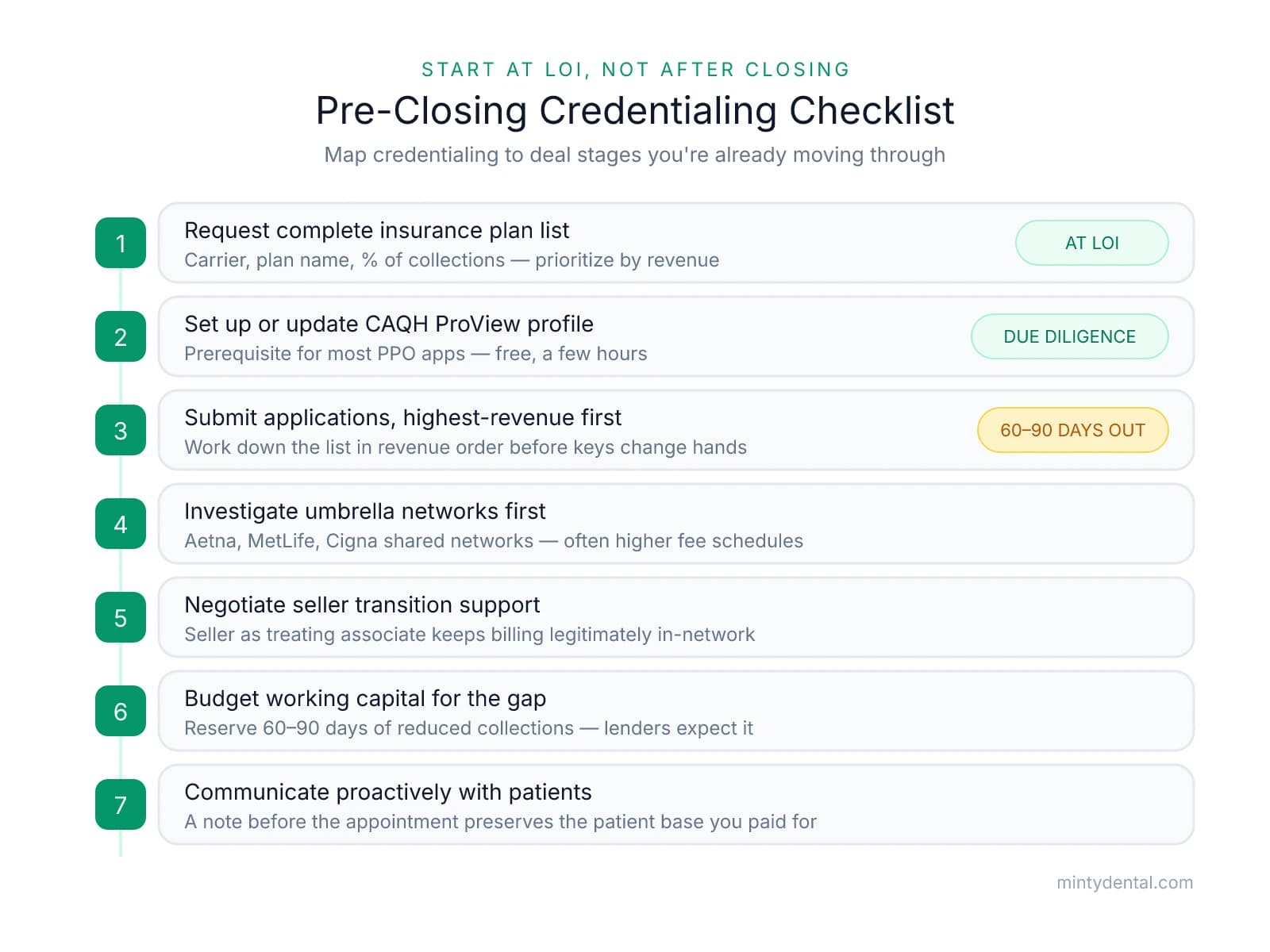

The buyers who come through a practice acquisition with minimal credentialing disruption aren't doing anything exotic — they're simply starting earlier than everyone else. The checklist below maps the process to the deal stages you're already moving through, so credentialing is on the timeline before closing is.

Step 1: At LOI — Request the Complete Insurance Plan List from the Seller

Before you can credential with anyone, you need to know who you're credentialing with. As part of your letter of intent, request a full list of every insurance plan the practice participates in, including the plan name, carrier, and approximate percentage of collections each plan represents. This becomes the foundation of your credentialing plan — and tells you immediately which carriers to prioritize based on revenue concentration.

Step 2: During Due Diligence — Set Up or Update Your CAQH ProView Profile

CAQH ProView is the central credentialing database most major carriers draw from when processing applications. A complete, attested profile is the prerequisite for the majority of PPO applications — without it, many carriers won't begin reviewing your submission. If you already have a CAQH profile from your associate position, update it to reflect your new practice address and entity information. This step costs nothing and takes a few hours; skipping it adds weeks to every application downstream.

Step 3: 60–90 Days Before Target Close — Submit Applications, Highest-Revenue Plans First

As Dental Buyer Advocates recommends, applications should be submitted during due diligence — not after you have keys in hand. Start with the carriers that represent the largest share of the practice's PPO revenue. If Delta Dental and BlueCross account for 60% of collections, those go first. Work down the list in revenue order so that if any applications run long, the lower-revenue plans are the ones still pending at closing.

Step 4: Investigate Umbrella Networks Before Submitting Individual Applications

Some carriers — including Aetna, MetLife, and Cigna — participate in shared network arrangements where credentialing with one may pick up others, often at higher fee schedules than direct contracting. These arrangements vary by state and zip code and change frequently, so a conversation with a credentialing specialist before submitting individual applications is worth the time. Getting this wrong means leaving money on the table from day one.

Step 5: Negotiate Seller Transition Support in the Purchase Agreement

A seller who stays on as an employed associate for 60–90 days after closing isn't just a goodwill gesture — it's a billing continuity mechanism. When the seller is the actual treating provider, claims can legitimately be submitted under their credentials. Structuring this with defined clinical responsibilities and a clear timeline protects the practice's in-network revenue while your own applications process.

Step 6: Budget Working Capital to Cover the Gap

Even with applications submitted early, some carriers will still be pending at closing. Building working capital reserves to cover 60–90 days of reduced collections is a legitimate use of practice acquisition financing — and lenders expect it. If you're still calibrating how much cash you need going into a purchase, the breakdown in how much money to have saved before buying a practice is worth reviewing before you finalize your financing structure.

Step 7: Communicate Proactively with Patients

Patients told at checkout — after treatment — that their insurance wasn't accepted rarely return. Patients who receive a brief, professional note explaining that the new owner is in the process of joining their networks, with clear options for how to proceed, tend to stay. A short letter or email at the transition point goes a long way toward preserving the patient base you paid for.

Managing the Gap You Couldn't Prevent: Patient Communication and Cash Flow

Even buyers who execute the pre-closing checklist carefully will often face some credentialing gap. Carriers have processing backlogs. Applications get lost in provider relations queues. Closing dates shift and throw off timing you planned around. Everything covered in this article is aimed at shrinking that gap — but it's worth being direct: you may not eliminate it entirely, and that's okay. What separates buyers who come through the first year intact from those who don't isn't whether they faced a gap. It's whether they had a plan for it.

Patient communication is the highest-leverage action you can take during the gap. The attrition risk isn't primarily about insurance — it's about surprise. Patients who discover at checkout that their coverage wasn't accepted feel misled, even when nothing dishonest happened. Patients who received a brief, professional note before their appointment — explaining that the new owner is actively joining their networks, providing a realistic timeline, and offering to help them understand their out-of-pocket benefits — tend to stay. The message doesn't need to be elaborate. It needs to arrive before the appointment, not after.

On the cash flow side, a working capital line of credit is the right tool for bridging the gap period — and it works best when arranged before closing, not when collections have already dropped. Most practice lenders expect buyers to carry working capital reserves; the credentialing gap is exactly the scenario those reserves exist for. As Ignite DDS notes, delayed or denied reimbursements can have serious consequences for your practice's cash flow. If the broader picture of first-year financial exposure is still coming into focus, the breakdown of unexpected expenses new owners consistently underestimate is worth reviewing before you finalize your financing structure.

Two operational habits that matter during the gap: follow up weekly with each carrier's provider relations line, document every contact with a date and representative name, and escalate applications that go quiet past 90 days. Credentialing delays often stall not because of a problem with your application, but because no one is actively pushing it forward.

Finally, when approval arrives — negotiate before you sign. The fee schedule in the initial offer is rarely the best available, and the moment of approval is your highest point of leverage. Once you're signed and listed in the directory, that leverage disappears.

The buyers who handle this well share one mindset: they treat the credentialing gap as a known, plannable cost of acquisition — not a surprise that destabilizes their first year. Model it into your cash flow projections before closing, communicate proactively with patients during it, and negotiate aggressively when it ends. That's preparation, not optimism.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- The Hidden Challenge in Dental Practice Transitions — Insurance ...— ameriprac.comIndustry

- What Is the Average Dental Practice Revenue in 2025? - Overjet— overjet.comIndustry

- Billing During Practice Transition: 5 Critical Rules to Avoid Fraud— ppoadvisors.comIndustry

- Asset Vs Stock Purchase: Dental Practice Acquisition (2026 Tax + ...— dentalpracticeinsider.orgIndustry

- [PDF] Provider User Guide | CAQH— caqh.orgIndustry

- Credentialing for Dental Practice Insurance— www.dentalbuyeradvocates.comIndustry

- Insurance Credentialing as a New Dental Practice Owner - ignitedds— ignitedds.com

Avoid Credentialing Gaps When Buying Your Practice

Insurance credentialing delays can cost thousands in lost revenue during practice transitions. Minty's Operations team handles all billing and credentialing logistics, so you can focus on patient care from day one.