Dental Practice Debt Anxiety: How New Owners Cope

Co-Founder, Minty Dental

In Summary

- The anxiety spike after closing on a dental practice is nearly universal among first-time buyers — it doesn't mean the deal was wrong or that you made a mistake

- According to the ADA's 2021 Dentist Well-Being Survey, anxiety diagnoses among dentists tripled between 2003 and 2021, rising from 5% to 16%, with financial and business pressure among the key drivers

- Dentists are trained to project competence and treat help-seeking as weakness — this makes the internal experience of debt anxiety more isolating than it needs to be

- Solo practice ownership removes the peer interaction that would otherwise normalize these feelings, compounding the psychological weight of carrying a seven-figure loan

- Debt anxiety in new owners is often a mismatch between the emotional weight of the number and the actual cash-flow math behind it — separating the two is the first step toward managing it

Debt Anxiety After Buying a Practice Is Normal — and Often Disconnected from Real Risk

Dental practice debt anxiety is the gap between the emotional weight of a seven-figure loan and the actual cash-flow math behind it. Those two things are not the same — but in the weeks after closing, they can feel identical.

If you've recently bought a practice and found yourself lying awake running numbers you've already run, you're not alone. The anxiety spike that follows closing is nearly universal among first-time buyers. It doesn't mean the deal was wrong or that you missed something — it means you're a high-achieving person who just took on the largest financial commitment of your life, and your nervous system is responding accordingly.

What makes this harder for dentists is the professional culture surrounding it. The training environment rewards certainty and penalizes doubt, so when anxiety arrives, many new owners absorb it quietly rather than name it — which only amplifies it.

The data reflects how widespread this has become. According to the ADA's 2021 Dentist Well-Being Survey, the percentage of dentists diagnosed with anxiety more than tripled between 2003 and 2021 — rising from 5% to 16% — with financial and business pressure cited among the key contributing factors. The majority of dentists also report moderate-to-severe work stress. These aren't outliers. This is the profession.

Solo ownership adds another layer. As an associate, you had colleagues in the building, a schedule someone else managed, and implicit peer accountability that made the workday feel shared. Ownership strips most of that away. The isolation that follows — which many new owners describe as surprisingly acute — creates a feedback loop where anxiety grows in the absence of anyone to normalize it.

Here's what tends to be true once new owners actually sit down with their numbers: the cash flow math is more manageable than the emotional weight of the loan suggests. Practice debt, structured correctly, is serviced by the business — not by you personally scrambling to cover a bill. That distinction matters, and it's the cognitive reframe worth building on.

Reframing the Debt: What $1 Million in Practice Loans Actually Means

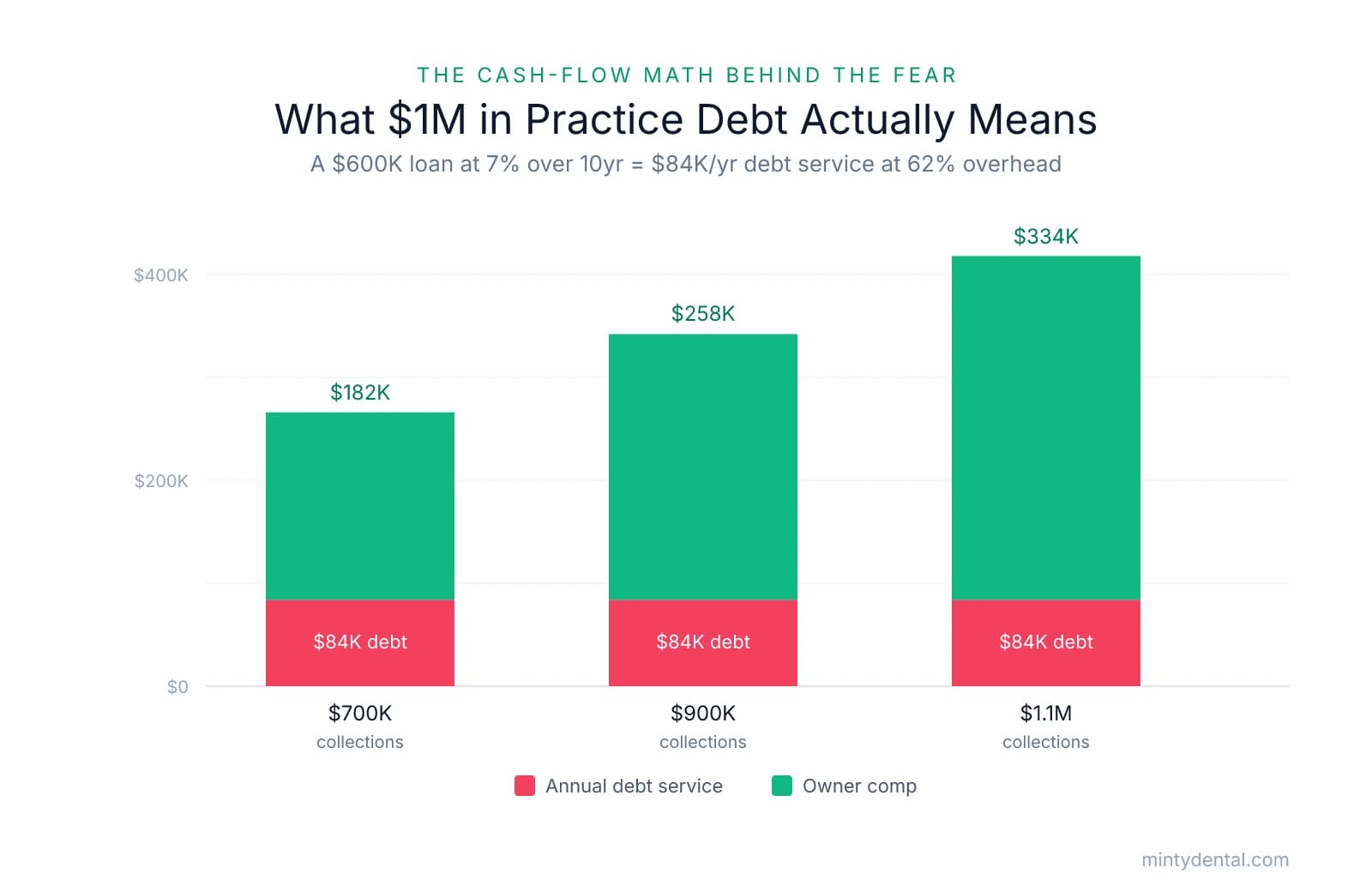

The number that tends to sit heaviest on new owners isn't the practice loan alone — it's the combined total. According to Panacea Financial via ADA News, the typical dentist entering practice ownership carries roughly $400,000 in student loans at closing, plus a practice acquisition loan that commonly runs $500,000–$700,000. Add those together and you're staring at something close to $1 million in total debt — a figure that, viewed in isolation, is genuinely alarming.

But viewed in isolation is exactly the wrong way to look at it.

Practice debt is structurally different from every other debt you've carried. Student loans funded a credential. A car loan funds transportation. A mortgage funds shelter. A practice acquisition loan funds an asset that generates the cash flow to pay for itself — which is what makes it self-liquidating in a way that consumer debt simply isn't.

The math makes this concrete. Consider a practice collecting $900,000 annually with 62% overhead — a reasonable benchmark for a general practice. That leaves roughly $342,000 for owner compensation and debt service combined. A $600,000 practice loan at 7% over 10 years runs approximately $84,000 per year, or about $7,000 per month. That's a real number — but it's a very different number when you see it against $28,000–$30,000 in monthly collections than when it exists as a standalone figure at 2 a.m.

| Annual Collections | Est. Overhead (62%) | Available for Comp + Debt Service | $600K Loan Payment (7%, 10yr) | Remaining for Owner Comp |

|---|---|---|---|---|

| $700,000 | $434,000 | $266,000 | $84,000 | $182,000 |

| $900,000 | $558,000 | $342,000 | $84,000 | $258,000 |

| $1,100,000 | $682,000 | $418,000 | $84,000 | $334,000 |

One thing worth internalizing: the lender already ran this math before approving your loan. Dental-specific lenders underwrite based on practice cash flow, not just personal income history — they model debt service coverage, stress-test collections, and assess whether the practice can carry the loan through a slow quarter. The underwriting process is itself a form of third-party validation that you likely can afford this. What banks actually look for in dental practice financing goes deeper than most buyers realize — and understanding what they already concluded about your deal is worth revisiting when doubt creeps in.

The anxiety is often a mismatch — treating practice debt emotionally like consumer debt, when the mechanics are fundamentally different. Consumer debt costs you money. Practice debt, structured well, builds equity and generates income simultaneously. That's the structural distinction that makes buying a practice with $400K in student loans more viable than most associates assume.

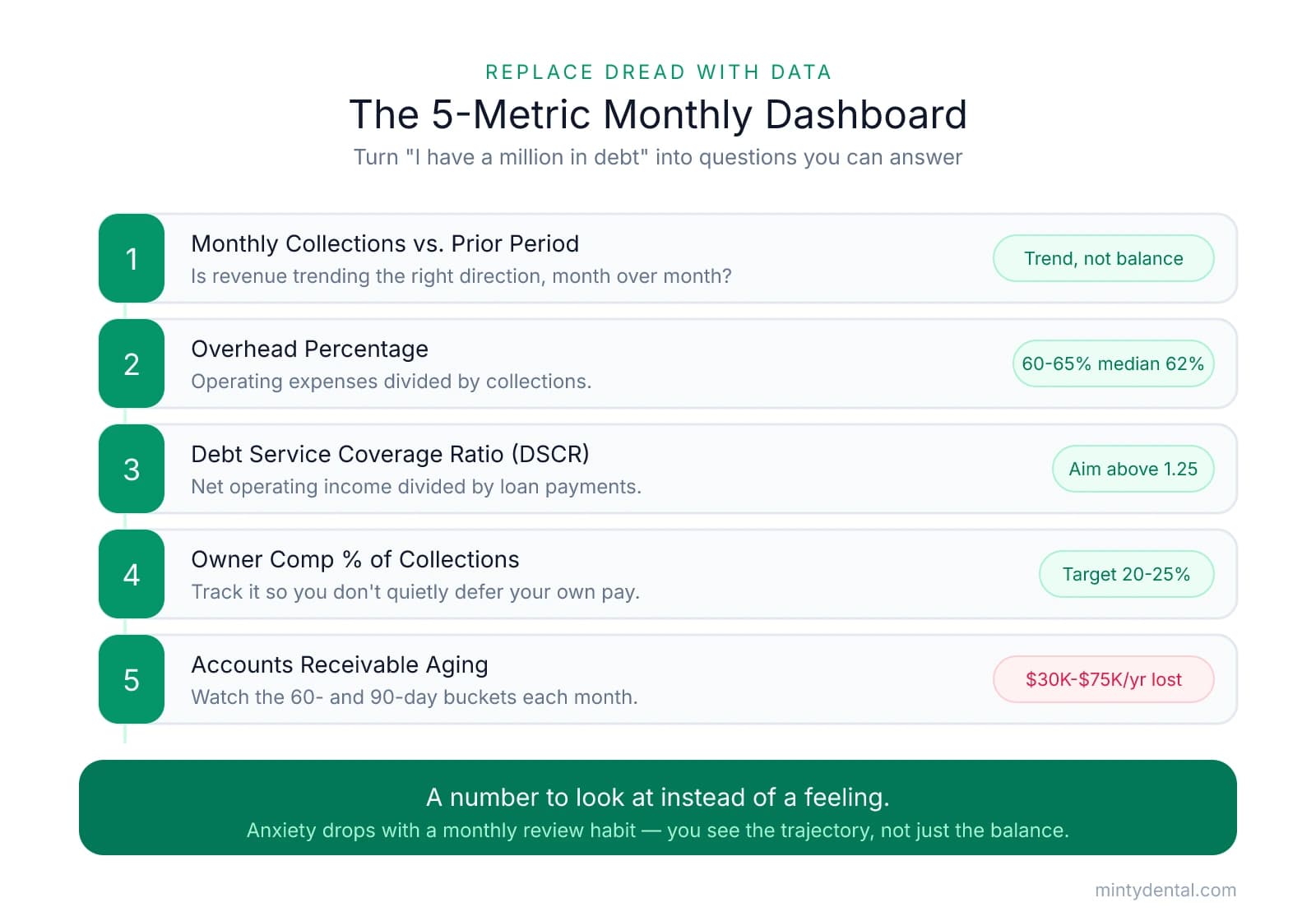

The Financial Dashboard That Replaces Dread with Data

Vague anxiety thrives in the absence of information. When the only number you're checking is your bank balance, you're left with either relief or panic — neither of which tells you whether your practice is actually healthy. What tends to shift the experience for new owners isn't that the debt gets smaller; it's that they stop navigating by feeling and start navigating by data.

The five metrics below form a simple monthly dashboard. Together, they convert "I have a million dollars in debt" into a set of operational questions you can actually answer.

1. Monthly Collections vs. Prior Period Is revenue trending in the right direction? Compare this month's collections to last month and to the same month last year. A practice that collected $72,000 in January and $78,000 in February is telling you something meaningful, even if neither number feels large enough yet.

2. Overhead Percentage Divide total operating expenses (everything except your own compensation) by total collections. According to the American Dental Association, the national benchmark sits at 60–65%, with the median around 62%. The gap between a 62% and 70% overhead practice collecting $1 million annually is roughly $80,000 in take-home income. Many new owners discover unexpected first-year expenses that temporarily push this number higher — knowing the benchmark helps you distinguish a short-term adjustment from a structural problem.

3. Debt Service Coverage Ratio (DSCR) DSCR: Divide monthly net operating income by monthly loan payments. A ratio above 1.25 generally indicates the practice is generating enough cash flow to cover its debt with room to spare. Below 1.0 means the practice isn't covering its own payments — which warrants immediate attention. This single number answers the question most new owners are really asking at 2 a.m.

4. Owner Compensation as a Percentage of Collections A pattern worth watching: many new owners defer their own compensation during slow months without tracking it. A reasonable target is 20–25% of collections. If that number is consistently near zero, the practice's financial structure deserves a closer look.

5. Accounts Receivable Aging The gap between what you've produced and what you've collected is often where cash flow problems hide. Pull your AR aging report monthly and look at what's sitting in the 60- and 90-day buckets. Per Red Bike Advisors, top-performing practices collect 98–99% of adjusted production — most practices quietly lose $30,000–$75,000 annually in that gap. Understanding your AR position after acquisition is especially important in the first year, when collection patterns from the previous owner may still be working through the system.

The goal isn't a perfect score every month — it's having a number to look at instead of a feeling. Most new owners find their anxiety decreases meaningfully once they establish a monthly review habit, not because the numbers are always good, but because they can see the trajectory instead of just the balance.

One of the highest-ROI investments in your first 12 months is a dental-specific CPA or financial advisor who can help you build this habit and interpret what you're seeing. A generalist accountant can file your taxes; a dental-focused advisor can tell you whether your overhead percentage is a staffing issue or a supply cost issue — and that distinction is worth more than their fee.

When the Numbers Are Fine but the Anxiety Isn't: Getting the Right Support

Here's a pattern that shows up more than most new owners expect: you run the numbers, confirm the practice is healthy, watch the dashboard metrics trend in the right direction — and still feel anxious. That's not a financial problem anymore. It's a psychological one, and it deserves the same direct attention you'd give a collections shortfall.

The professional culture dentists train in doesn't make this easy. The expectation — absorbed over years of clinical education — is that competent people handle pressure quietly and independently. That conditioning is useful in an operatory. It becomes a liability when it prevents you from reaching for support that would genuinely help.

One of the most underused resources in the profession is peer connection. The ADA Dentist Well-Being Program connects owners with state-level peer support through confidential channels — both members and non-members can access the directory. According to the ADA's 2021 Dentist Well-Being Survey, only 46% of dentists were even aware of their state's program. Awareness is the first barrier. Dentist-specific peer groups and mastermind communities serve a similar function — they normalize the experience of ownership in a way that no amount of solo reflection can replicate.

A financial advisor with dental-specific expertise offers a different kind of grounding: external validation that the math is working, delivered by someone who understands practice cash flow, debt service cycles, and the income trajectory that ownership typically follows. When anxiety is whispering that something must be wrong, a dental-focused advisor can look at your actual numbers and tell you, specifically, whether it is.

And when anxiety persists despite healthy numbers and good advisors, a mental health professional — ideally one with experience working with high-achieving professionals — can help break the pattern. State dental associations maintain confidential referral programs for exactly this. Seeking that support isn't a sign of failure; it's a sign that you understand the difference between a problem you can spreadsheet your way out of and one that requires a different tool.

The goal was never to eliminate financial vigilance entirely — some of that vigilance is what keeps you watching the dashboard and staying engaged with the business. The goal is to keep anxiety from making decisions that the data should be making. Owners who feel a flash of worry and then check their DSCR are using anxiety productively. Owners who feel that same worry and quietly spiral are letting it run the practice.

If you've built the monitoring habits above and still find yourself second-guessing a deal the numbers support, that's useful information — and it points toward support, not more spreadsheets.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Dentist Health and Well-Being Survey Report finds ... - ADA News— adanews.ada.orgIndustry

- Ask the Expert: How much debt is too much when buying a dental ...— adanews.ada.orgIndustry

- Average Dental Practice Overhead: Benchmarks and Insights - Overjet— www.overjet.comIndustry

- What Are the Most Important Financial KPIs for a Dental Practice?— redbikeadvisors.comIndustry

- [PDF] 2021 Dentist Well-Being Survey Report - American Dental Association— ada.orgIndustry

Ready to own a debt-free dental practice?

New practice owners often inherit significant debt and financial stress. Minty's acquisition experts guide you through every step of buying a practice, helping you understand the true financial picture and negotiate terms that work for your situation.