When Your Parents Think Buying a Dental Practice Is Too Risky

Co-Founder, Minty Dental

In Summary

- Healthcare businesses fail at just 7.3% — nearly half the rate of restaurants and retail, which both sit at 12.8%

- Dental demand is inelastic: patients still need cleanings, fillings, and emergency care during recessions, unlike discretionary spending

- Professional licensing creates a layer of accountability unique to healthcare — a dentist who defaults risks their career, not just their credit score

- Staying an associate feels safe, but it carries its own financial risks that are easy to underestimate over a 10–15 year horizon

- Most parental concern about practice ownership comes from applying general small-business intuition to a profession that operates by fundamentally different rules

Your Parents Are Applying the Wrong Risk Framework to Dentistry

If your parents are nervous about you borrowing $800,000 to buy a dental practice, that concern comes from a reasonable place. They watched friends lose everything in 2008. They grew up with "never borrow more than you can afford to lose." They've seen restaurants close, retail shops shutter, and small businesses disappear. Their risk intuition is real — it's just calibrated for the wrong category of business.

The core issue: dental practice ownership isn't a typical small-business bet. It's a healthcare business built on essential services, operated by a licensed professional, with patient relationships that generate recurring, predictable revenue. That combination produces a fundamentally different risk profile than opening a boutique or a sandwich shop — and the data reflects it.

According to Dentistry.co.uk, healthcare businesses fail at just 7.3% — compared to 12.8% for both restaurants and retail. That's nearly half the failure rate of the industries most people picture when they hear "small business risk."

Three structural reasons explain that gap:

-

Demand is inelastic. A dental emergency doesn't wait for the economy to recover. Preventive care, fillings, and extractions continue through recessions in ways that discretionary spending simply doesn't. Patients delay vacations — they don't delay abscesses.

-

Licensing creates accountability. A dentist who defaults on a practice loan isn't just facing a credit hit — they're potentially putting their license at risk. That professional stake raises the floor on how hard an owner-operator will work to keep a practice viable. Lenders know this, which is part of why healthcare-specific financing tends to be more accessible than conventional small-business loans.

-

Patient relationships are sticky. Established practices carry years of patient history, treatment plans, and trust. That's not goodwill in the abstract — it's a revenue base that doesn't evaporate overnight.

None of this means practice ownership is without risk. The debt is real, the operational learning curve is steep, and the anxiety that comes with it is something most new owners navigate quietly. But the framing matters. When your parents say "that's too risky," they're usually picturing a restaurant on a busy street — not a healthcare business with a licensed operator, essential-service demand, and a patient base that took a decade to build.

Worth naming directly: staying an associate isn't a risk-free alternative. It's a different risk — slower, less visible, and easy to rationalize year after year. That's worth examining closely.

What the Loan Default Data Actually Says About Dental Practices

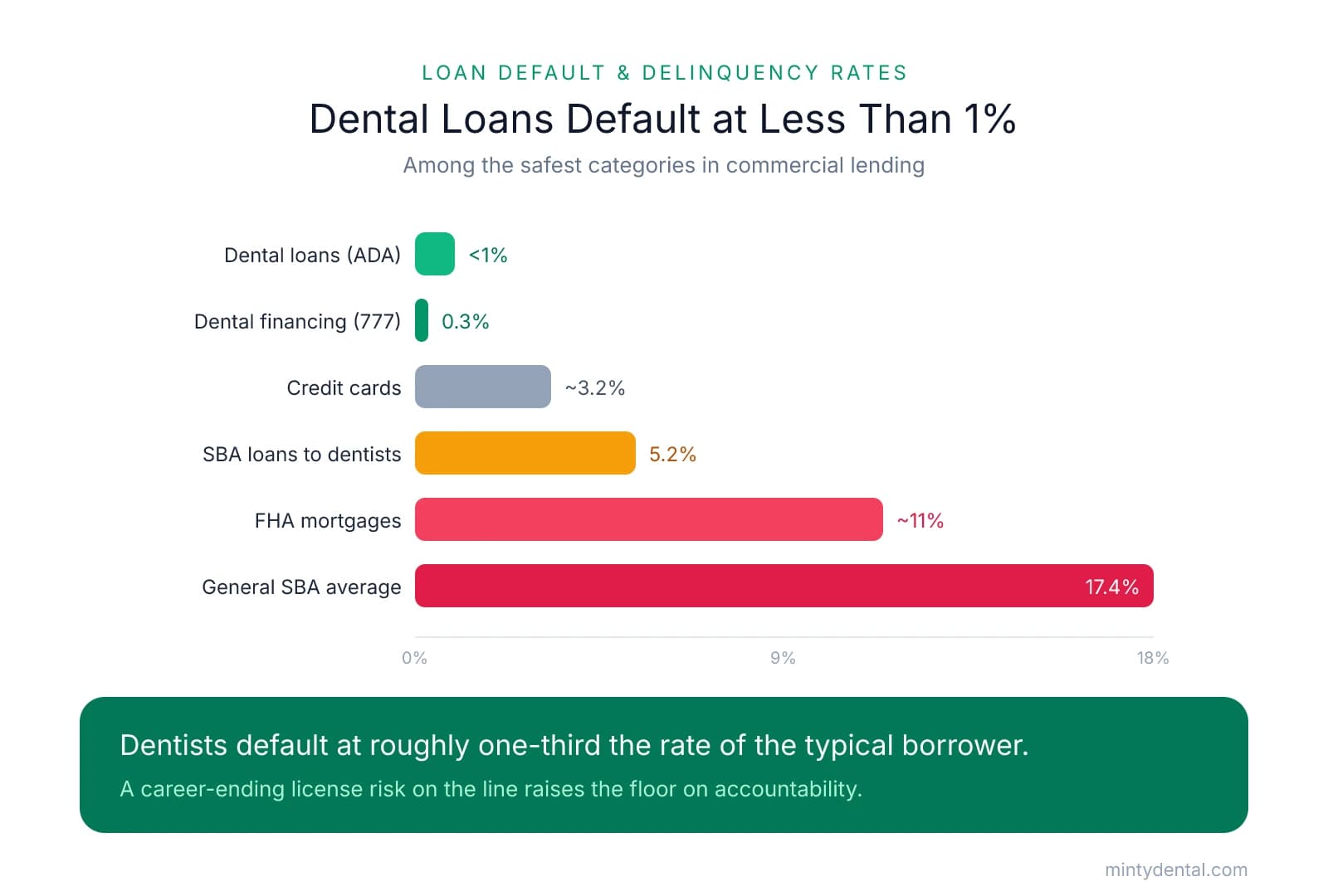

If there's one set of numbers worth putting in front of a skeptical parent, it's the default data. Not because it ends the conversation, but because it replaces intuition with evidence — and the evidence is striking.

Dental practice loan default rates: According to the ADA, dental practice loans default at less than 1%, making them among the safest investments in commercial lending. An independent analysis of 777 dental practices found a delinquency rate of just 0.3% on practice-related financing — a figure that holds up across multiple data sources.

The SBA comparison makes the picture even clearer:

| Loan / Credit Category | Default or Delinquency Rate |

|---|---|

| Dental practice loans (ADA) | < 1% |

| Dental practice financing (777-practice analysis) | 0.3% |

| SBA loans to dentists | 5.2% |

| Consumer credit cards | ~3.2% |

| FHA mortgages | ~11% |

| General SBA loan average | 17.4% |

SBA loans to dentists default at 5.2% versus 17.4% for the general SBA average — meaning dentists default at roughly one-third the rate of the typical small-business borrower. Consumer credit cards run around 3.2% delinquency. FHA mortgages sit near 11%. Dental practice loans outperform both by a wide margin.

Why the Numbers Look This Way

The low default rate isn't primarily a story about dentists being unusually disciplined borrowers. It's structural.

A dentist who defaults on a practice loan isn't just facing a damaged credit score — they're potentially triggering a state board investigation that could threaten their professional license. In most states, a pattern of financial defaults can result in license suspension or revocation. For an independent practitioner, that's not a financial setback. It's career termination. That asymmetry changes the calculus in ways that don't apply to a retail business owner or a restaurant operator.

Geographic stability reinforces this further. Dentists invest years building local patient relationships and referral networks. Walking away from a loan means walking away from everything that took a decade to build — a trade-off most owners will exhaust every alternative to avoid.

What 100% Financing Signals

One detail that often surprises families: most dental practice acquisitions are financed with no down payment. Lenders routinely cover 100% of the purchase price, plus working capital for the first few months. Understanding what banks actually evaluate when underwriting these loans helps explain why — they're not being generous, they're responding to an asset class with a track record that justifies the confidence.

When a lender extends seven figures with no money down, they're not taking a leap of faith. They're reading the same default data your parents haven't seen yet.

The Income Gap Your Parents Aren't Factoring In

The default data addresses the downside. But there's a second half of this conversation that often goes unspoken — what staying an associate actually costs over time.

Most parents frame this as: ownership is risky, employment is safe. What that framing misses is that "safe" has a price tag, and over a career, it's a significant one.

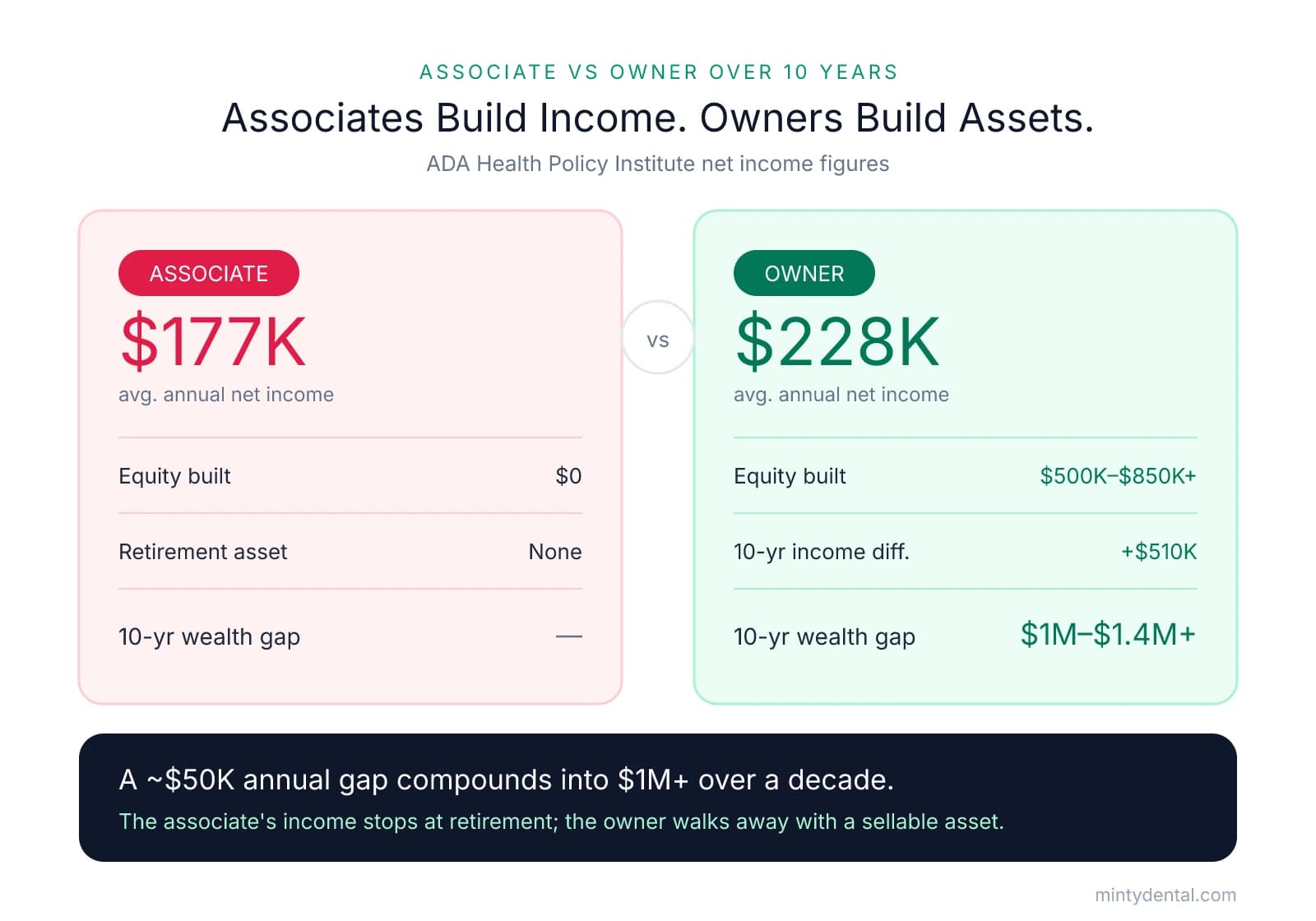

The $50K Annual Gap

According to the ADA Health Policy Institute, owner general practitioners averaged approximately $228,000 in net income compared to $177,000 for employed general dentists — a gap of roughly $50,000 per year. That figure comes with more responsibility, yes. But it's worth understanding where that responsibility leads financially.

Over ten years, a $50,000 annual gap compounds into something harder to ignore:

| Associate | Owner | |

|---|---|---|

| Annual income (avg.) | $177,000 | $228,000 |

| 10-year income differential | — | +$510,000 |

| Equity built | $0 | $500K–$850K+ |

| Total 10-year wealth gap | — | $1M–$1.4M+ |

That equity column is where the real divergence happens.

Associates Build Income. Owners Build Assets.

An associate earns well — until they stop working. There's no asset accumulating in the background, no balance sheet entry that grows as the practice grows. When an associate retires, the income stops.

Owners build something different. A practice collecting $1M annually typically sells for 50–85% of annual collections at exit — meaning $500,000 to $850,000 in realized wealth at retirement, independent of whatever income was earned along the way. That's a retirement asset the associate model simply doesn't produce. For a clearer picture of how your current compensation stacks up against what ownership could generate, the associate pay calculator makes the comparison concrete.

Tax treatment widens the gap further. Practice owners can access Section 179 equipment deductions, defined benefit retirement plans, and a range of business deductions that employed dentists can't touch. The after-tax income difference between an owner and an associate tends to be larger than the gross figures suggest.

The "Safe" Path Is Shifting

There's one more variable worth naming. The associate track is changing in ways that make the traditional safety argument harder to sustain.

ADA data shows that 27% of dentists less than 10 years out of dental school are now DSO-affiliated, up from 24% in 2023. As corporate dentistry consolidates, associate compensation tends to compress and clinical autonomy narrows. The employment market your parents picture — stable, independent, professionally fulfilling — looks different than it did a decade ago.

Ownership isn't the only path. But the income gap, the equity gap, and the shifting employment landscape together suggest that the "safe" choice carries more long-term financial risk than it appears on the surface.

How to Have This Conversation With Your Family

Armed with that data, the harder task is translating it into a conversation with people who love you and are genuinely worried. This isn't a debate to win — it's a perspective to share, with the goal of redirecting concern toward the variables that actually determine success.

Three Reframes Worth Having

"You're taking on $800,000 in debt." A more accurate framing: the practice generates enough cash flow to service that debt and pay a salary — and the bank verified this before approving the loan. Lenders don't extend seven figures on optimism. They model the practice's revenue against the debt obligation and only approve when the numbers work. If the cash flow didn't support it, the loan wouldn't exist.

"What if it fails?" Dental practices fail at roughly half the rate of restaurants — and the dentist operating one has a professional license on the line. Default isn't just a credit event; in many states it can trigger a board review that threatens the license entirely. That asymmetry creates structural accountability that doesn't exist in most small businesses. The incentive to make it work is built into the profession itself.

"You already have student loans." Lenders don't evaluate acquisition debt against total debt load the way a parent might. They evaluate whether the practice's cash flow covers the acquisition debt — and if it does, student loans don't disqualify the deal. If you're navigating this specific concern, the nuances of buying a practice with significant student debt are worth walking through together.

What Your Parents Are Right About

Here's where it's worth agreeing with them: due diligence matters, practice selection matters, and having an advisory team — a dental CPA, an attorney, a broker who represents buyers — genuinely changes outcomes. Their instinct that something requires careful attention is correct. The ADA's guidance on purchasing with confidence makes the same point: building your team of lawyers and accountants before you find the practice — not after — is what allows a transaction to move smoothly when the right opportunity appears. The goal is to redirect that attention toward variables that are actually controllable.

If you're still working through whether the timing is right professionally, clinical readiness is a real question worth answering honestly before moving forward.

The Cost of Waiting Is Also Real

The dentists who wait for certainty often wait too long. Every year as an associate is a year without equity accumulating, without the income differential compounding, and without the retirement asset growing in the background. The risk of ownership is visible and easy to name. The cost of delay is quieter — but over a decade, it's just as significant.

The data doesn't promise a perfect outcome. It does suggest that the risk your parents are imagining and the risk that actually exists are two different things.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Why dental practice ownership is safer than you think - Dentistry.co.uk— dentistry.co.ukNews

- Dentist compensation: what every dental associate should know— ada.orgIndustry

- Dentists Default at 0.3% - Arvind Murthy— arvindmurthy.com

- Dentist Salaries in 2025: Comparing DSO vs. Dentist-Owned Practices— www.whitecoatinvestor.comIndustry

- How to purchase with confidence | American Dental Association— www.ada.orgIndustry

Turn Dental Practice Ownership Into Your Reality

Buying a dental practice doesn't have to be a solo journey filled with uncertainty. Minty provides hands-on guidance from your first search through closing, with no upfront fees—giving you and your family the confidence that comes with expert support every step of the way.