Should You Buy a Dental Practice with Mostly PPO Patients?

Co-Founder, Minty Dental

In Summary

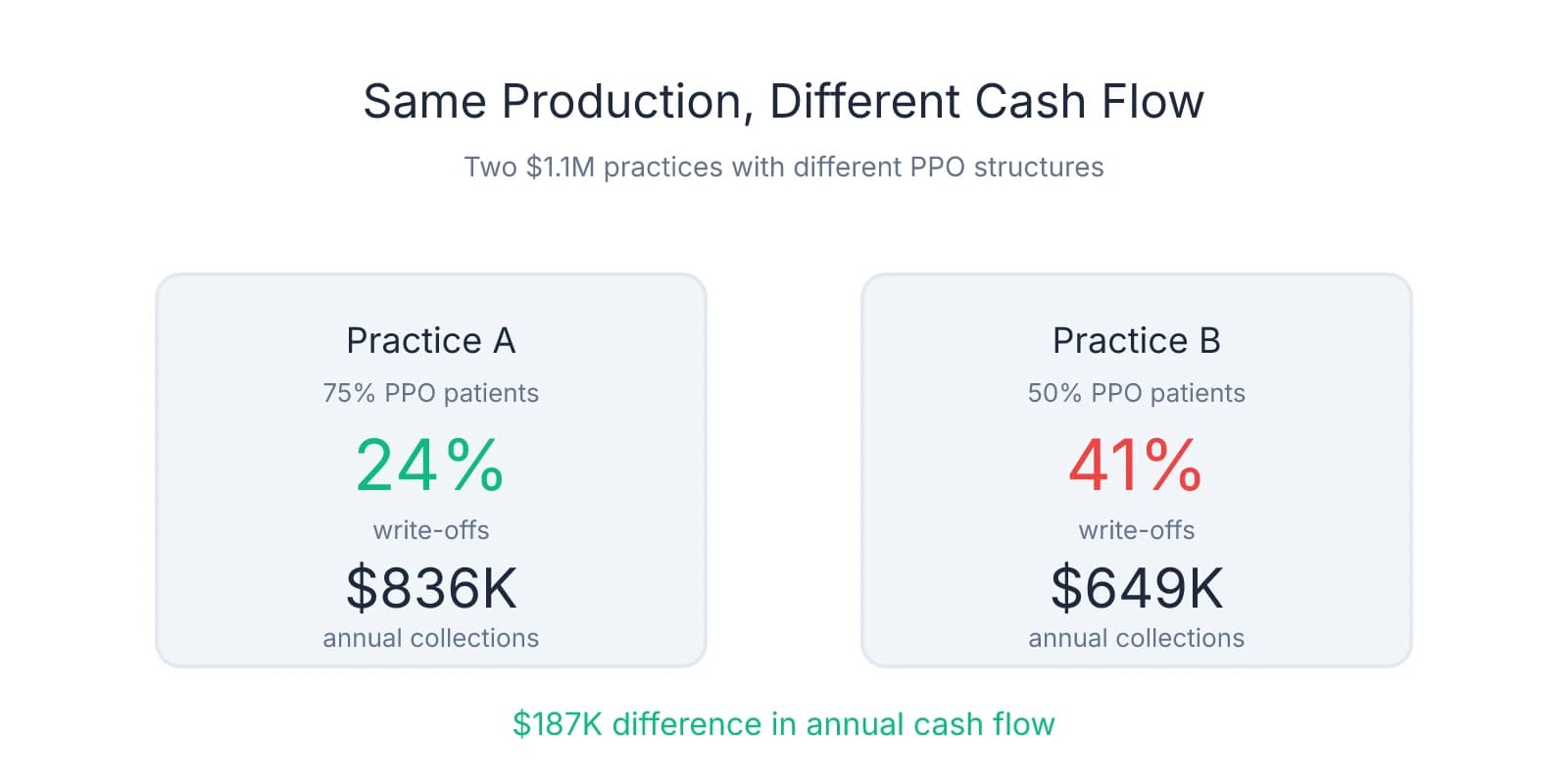

- A practice with 75% PPO patients and 24% write-offs can be more profitable than one with 50% PPO and 41% write-offs—patient mix matters less than contract quality

- Over half of dentists cite low reimbursement rates as a top concern in 2026, yet many practices haven't renegotiated contracts in 3-7 years

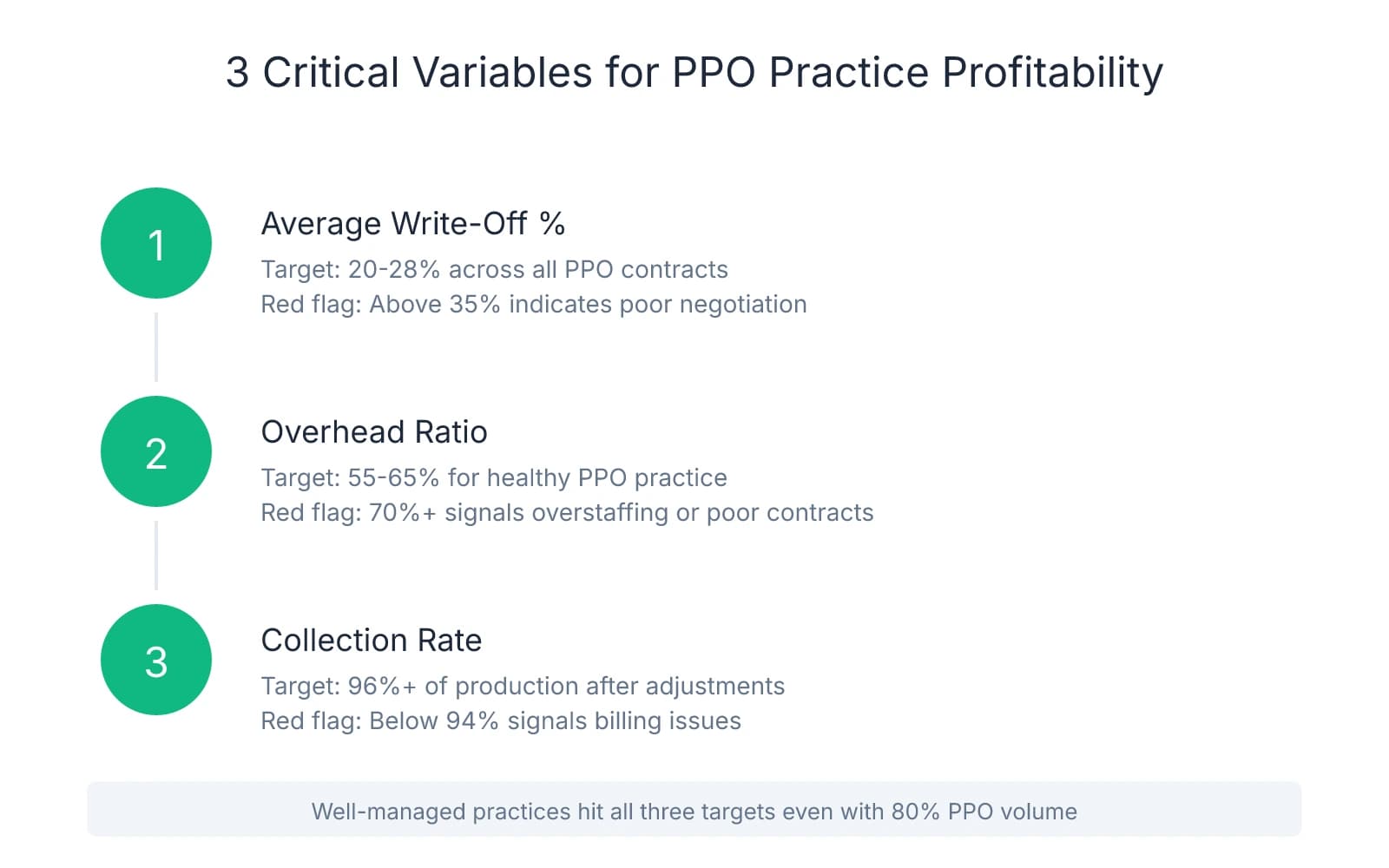

- Three critical variables determine PPO practice profitability: average write-off percentage, overhead ratio (target 55-65%), and collection rate (should be 96%+)

- Practices that actively manage PPO contracts—renegotiating rates, dropping low-performing plans, optimizing fee schedules—can maintain healthy margins even with high PPO volume

- The difference between a well-optimized PPO practice and a neglected one often shows up in EBITDA, not gross production numbers

The Real Question Isn't PPO vs. FFS—It's Whether the PPO Structure Is Optimized

Pull the P&L statements from two practices with identical $1.1M in production. One shows 75% PPO patients with 24% write-offs. The other shows 50% PPO with 41% write-offs. Which one would you buy?

Most buyers instinctively lean toward the lower PPO percentage. But the first practice—despite higher PPO volume—nets significantly more cash. The difference isn't patient mix. It's contract quality.

This pattern shows up repeatedly when buyers verify dental practice collections during due diligence. A practice with 80% PPO patients and tight contract management can outperform a 60% fee-for-service practice where the owner accepted every insurance plan that walked through the door and never looked back.

The ADA Health Policy Institute reports that more than half of dentists cite low reimbursement rates as a top concern heading into 2026. Yet many of those same practices haven't renegotiated contracts in three to seven years. The seller you're evaluating may fall into this category—accepting rates that made sense in 2018 but eroded quietly as overhead climbed.

Three variables determine whether a PPO-heavy practice is a smart acquisition or a margin trap. First: average write-off percentage. A well-managed practice typically writes off 20-28% across all PPO contracts. When write-offs push past 35%, you're looking at either poor contract negotiation or participation in deeply discounted plans that don't justify the patient volume they bring.

Second: overhead ratio. Target 55-65% for a healthy PPO practice. If overhead sits at 70% or higher, the practice is either overstaffed, underproducing, or locked into contracts that don't cover the cost of delivering care. This is where buyers often miss the real profitability picture—gross production looks strong, but net income tells a different story.

Third: collection rate. A well-run practice collects 96% or more of what it produces after contractual adjustments. Anything below 94% signals billing inefficiencies, poor follow-up, or unresolved claims the seller stopped chasing. This number matters more than production—it's what hits the bank account.

Practices that actively manage their PPO relationships—renegotiating rates every 2-3 years, dropping plans that don't meet minimum thresholds, adjusting fee schedules to maximize reimbursement—can maintain healthy margins even with 80% PPO volume. The ones that don't accept whatever rates the insurance companies offer and wonder why profitability stagnates.

When you're evaluating a PPO-heavy practice, the question isn't whether PPO patients are profitable. It's whether the seller treated their contracts as negotiable business terms or immovable facts. One approach builds equity. The other erodes it slowly until someone like you shows up to buy.

Calculate What the Practice Actually Collects Per Dollar of Production

Request a breakdown of write-offs by insurance carrier during due diligence. This single document reveals more about practice profitability than gross production ever will. When write-offs exceed 35% with any major carrier, you're looking at outdated contracts or participation in plans that reimburse below the cost of delivering care.

Calculate the practice's collection rate by dividing total collections by gross production. Healthy practices collect 96-98% of production after contractual adjustments. Anything below 90% signals either poor contract structure or billing inefficiencies that haven't been addressed. This calculation takes five minutes and tells you whether the practice converts production into revenue.

Two practices producing $1.1M can differ by $187,000 in annual collections based solely on PPO structure. A practice with 24% write-offs collects roughly $836,000. One with 41% write-offs collects around $649,000. Same production number. Wildly different cash flow. The seller's P&L might show identical gross revenue, but one practice deposits nearly $16,000 more per month.

Overhead benchmarks shift when PPO volume increases. The average dental practice runs at 60-65% overhead, but PPO-heavy practices need to stay closer to 55-60% to maintain profitability. When overhead climbs to 68% and write-offs sit at 38%, the practice operates on razor-thin margins—or worse, loses money on certain procedures while appearing profitable on paper.

Check whether the seller has renegotiated PPO contracts in the past three years. If not, you're inheriting either hidden revenue opportunity or hidden risk. Contracts signed in 2021 don't reflect 2025 overhead costs. Practices that haven't updated their fee schedules or challenged reimbursement rates often leave 8-12% of potential collections on the table—money that could have covered rising lab fees, staff wages, or supply costs.

Pull the aging report alongside the write-off analysis. If 15% of accounts receivable sits past 90 days and the collection rate hovers at 92%, the practice isn't just accepting low PPO rates—it's failing to collect what those contracts allow. This pattern compounds quickly. A practice that writes off 32% and collects 93% of what remains is functionally operating at a 38% revenue loss before overhead.

Compare the practice's effective collection rate to its stated EBITDA. When collections run at 88% and overhead sits at 67%, the seller's profitability claims deserve scrutiny. The numbers might reconcile on the P&L, but the underlying structure suggests the practice can't sustain those margins without significant operational changes—changes you'll be funding post-acquisition.

Identify Which PPO Contracts Are Worth Keeping—and Which Ones to Drop

Within your first 90 days of ownership, run a report showing patient count and total write-offs by carrier. This breakdown tells you exactly what you're paying for each PPO relationship. When a plan brings 50 patients but requires $30,000 in annual write-offs, you're spending $600 per patient for access—often more expensive than direct marketing, referral programs, or local partnerships that bring full-fee patients through the door.

Calculate the cost-per-patient for each carrier by dividing total annual write-offs by active patient count. Plans with high write-offs—40% or more—and low patient volume become immediate candidates for termination or renegotiation. A carrier that discounts your fees by 45% while representing 3% of your patient base isn't a strategic relationship. It's a margin drain you inherited from the previous owner.

Prioritize renegotiation with high-volume carriers first. A 5% improvement on a plan that represents 30% of your patient base generates far more revenue than dropping three small plans entirely. Many buyers focus on eliminating the worst contracts when the bigger opportunity sits with the plans that drive the most volume. Practices that renegotiate their top three carriers often recover 6-10% of annual write-offs without losing significant patient volume.

Network sharing and third-party administrator (TPA) contracts expose you to dozens of low-reimbursement plans you didn't directly sign. If the seller contracted with a TPA like Dentemax or Connection Dental, you may be in-network with 50-200 additional plans—each with different fee schedules, claim processes, and reimbursement rates. Review these arrangements during due diligence. Some TPAs share fee schedules across multiple carriers, meaning a single contract can make you in-network with plans you've never heard of.

Check your Explanation of Benefits statements to identify which fee schedules insurance plans are accessing. The contract you signed may say one thing, but the reimbursement you receive often tells a different story. If you're contracted with Aetna, you may also be in-network with Ameritas, Assurant, Principal, and Guardian through network sharing—each potentially reimbursing at different rates despite using the same base contract.

Practices transitioning from PPO to fee-for-service typically retain 60-75% of patients, and because full-fee patients generate higher margins, you need fewer appointments to maintain revenue. If you drop a plan that brings 100 patients at 40% write-offs, retaining 70 of those patients at full fee often produces more net revenue than keeping all 100 under contract. The math shifts dramatically when you stop discounting every procedure by nearly half.

Calculate how many patients you can afford to lose before dropping any plan. If a carrier represents 15% of your patient base but accounts for 28% of your total write-offs, losing half those patients while collecting full fees from the remainder often improves cash flow. This isn't about maximizing patient count—it's about maximizing the value of each patient relationship.

One decision framework many practices find useful: rank each PPO contract by write-off percentage, patient volume, and administrative burden. Plans that score poorly across all three categories—high discounts, low volume, complex claims processes—become your first targets for termination. Plans that score well on volume but poorly on reimbursement become renegotiation priorities. Plans that score well across all three stay in place while you optimize the rest of your payer mix.

Build Your Post-Acquisition PPO Strategy Before You Close

Request copies of all active PPO contracts and credentialing documentation during due diligence—not after closing. Missing or outdated credentials can delay revenue for months while you work through re-credentialing processes with carriers who don't prioritize new ownership transitions. One pattern that surfaces repeatedly: sellers who haven't updated their credentialing in years, leaving you to discover mid-transition that half your contracts require re-application before you can bill under your NPI.

Negotiate a structured transition period where the seller walks you through which carriers generate the most profit and which relationships are worth maintaining. This isn't about general handoff conversations—it's about sitting down with the seller and reviewing reimbursement data, claim denial patterns, and which plans they would have dropped if they weren't selling. Most sellers know exactly which contracts are problematic. They just never had the incentive to fix them.

Map your first 90 days before you close. Month one is for data gathering: analyze write-offs by carrier, patient volume by plan, overhead allocation, and collection efficiency. Month two is for renegotiation outreach—contact your top three carriers by volume and request fee schedule reviews. Month three is for implementation—drop the plans that don't meet your minimum thresholds, finalize renegotiated contracts, and communicate changes to patients who need to transition.

If the practice has neglected PPO management for years, factor renegotiation opportunity into your valuation. A practice with 35% write-offs that could be optimized to 25% through contract updates and selective plan termination is undervalued—you're buying a revenue stream the seller left on the table. This is where asking the right questions during acquisition conversations separates buyers who overpay from those who identify hidden upside.

The strongest acquisition strategy isn't avoiding PPO practices—it's identifying practices where the PPO structure is fixable and the seller has left money on the table. When you find a practice with strong patient volume, solid clinical systems, and neglected PPO contracts, you're looking at an opportunity to improve EBITDA by 8-12% without changing anything except the contracts you inherited. That improvement doesn't require new patients, expanded hours, or additional services. It just requires treating PPO contracts as negotiable business terms rather than permanent fixtures.

Build your renegotiation timeline into your acquisition financing plan. If you know you'll need 90 days to optimize contracts and another 60 days to see the revenue impact, structure your debt service expectations accordingly. Lenders who understand dental practice acquisitions recognize that PPO optimization takes time—but they also recognize that practices with clear renegotiation plans carry less risk than practices where the buyer assumes inherited contracts are permanent.

The time to plan your PPO strategy is during due diligence, when you still have leverage to negotiate seller support, request documentation, and walk away if the contracts are unfixable. Six months into ownership, when you're managing staff, learning clinical workflows, and handling patient relationships, PPO renegotiation becomes one more thing you don't have time for. The practices that succeed post-acquisition are the ones where the buyer treated PPO optimization as part of the purchase process—not an afterthought.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Dear ADA: Reimbursement rates | American Dental Association— adanews.ada.orgIndustry

- Average Dental Practice Overhead: Benchmarks and Insights - Overjet— overjet.com

- What Buyers Must Review Before Acquiring a Practice— pponegotiationsolutions.comIndustry

- How To Successfully Drop PPO Contracts - Burkhart Dental Supply— www.burkhartdental.com

Frequently Asked Questions

Ready to evaluate your next PPO practice?

Finding the right PPO-heavy practice requires expert guidance on patient mix, reimbursement rates, and long-term profitability. Minty Plus connects you with acquisition specialists who help you navigate these complexities and build a sustainable practice.