Buying a Dental Practice as an Associate in the Same Office

Co-Founder, Minty Dental

In Summary

- Associates buying the practice they work in start with patient relationships and operational knowledge that external buyers spend months building, which typically reduces transition risk and patient attrition.

- Working inside the practice reveals revenue patterns and staff dynamics—but this familiarity creates dangerous blind spots during due diligence, especially around lease terms, equipment financing, and contract obligations you've never examined.

- Personal relationships with your employer can make it harder to negotiate hard on valuation or contract terms, especially when gratitude clouds judgment about fair market value.

- Most dentists eventually become practice owners, but the path now takes longer than it did for previous generations—buying from your current employer is one way to accelerate that timeline.

The Insider Advantage Cuts Both Ways

When you're already working in the practice you're considering buying, you start with advantages most external buyers would pay to have. You know which patients prefer morning appointments, which hygienist handles anxious kids best, and where the lab keeps sending margins that don't seat. You've watched revenue patterns across seasons and probably have a mental list of equipment that needs replacing. That operational fluency matters—it's the difference between walking into ownership with momentum versus spending six months just learning how the practice runs.

The patient relationships you've built as an associate are particularly valuable. When ownership transitions, patient attrition often spikes as patients follow the departing dentist or drift away during the change. But if you're already their dentist, that risk drops significantly. They're continuing with someone they already trust, which protects revenue from day one.

The same familiarity that gives you an edge also creates risk. Many associates assume they know everything about the practice because they work there. What they miss are things that don't show up in daily operations: the equipment lease that balloons in year three, the hygienist who's been interviewing elsewhere, the PPO contract with a pending rate cut, or the building lease clause that lets the landlord block an ownership transfer. You know how the practice feels—you may not know how it's actually structured.

The relationship with your current employer adds another layer of complexity. It's harder to push back on a $50,000 valuation gap when you're negotiating with someone who gave you your first job or became a friend. Gratitude and loyalty are real, but they can make it difficult to treat the transaction with the same scrutiny you'd bring to buying from a stranger. Where external buyers naturally approach negotiations as adversarial, you're trying to preserve a relationship while protecting your financial future—and those two goals don't always align cleanly.

The data suggests this path is increasingly common, even if it takes longer than it used to. Practice ownership remains the career endpoint for most dentists, but ownership timelines have stretched—particularly for dentists who graduated after 2011. Buying from your current employer can compress that timeline, but only if you navigate the insider position intentionally.

How to Evaluate Valuation Fairness When You're Already on the Inside

The most common mistake associates make is treating the seller's asking price as a starting point for gratitude rather than negotiation. Many sellers expect associates to accept their valuation without question—either because they're offering a "discount" as a favor, or because they assume loyalty means skipping the appraisal process entirely. Neither approach protects you. A below-market price can still be overpriced if the practice has structural problems you haven't seen, and a "fair" price based on the seller's calculations may not reflect what the practice would actually command in the open market.

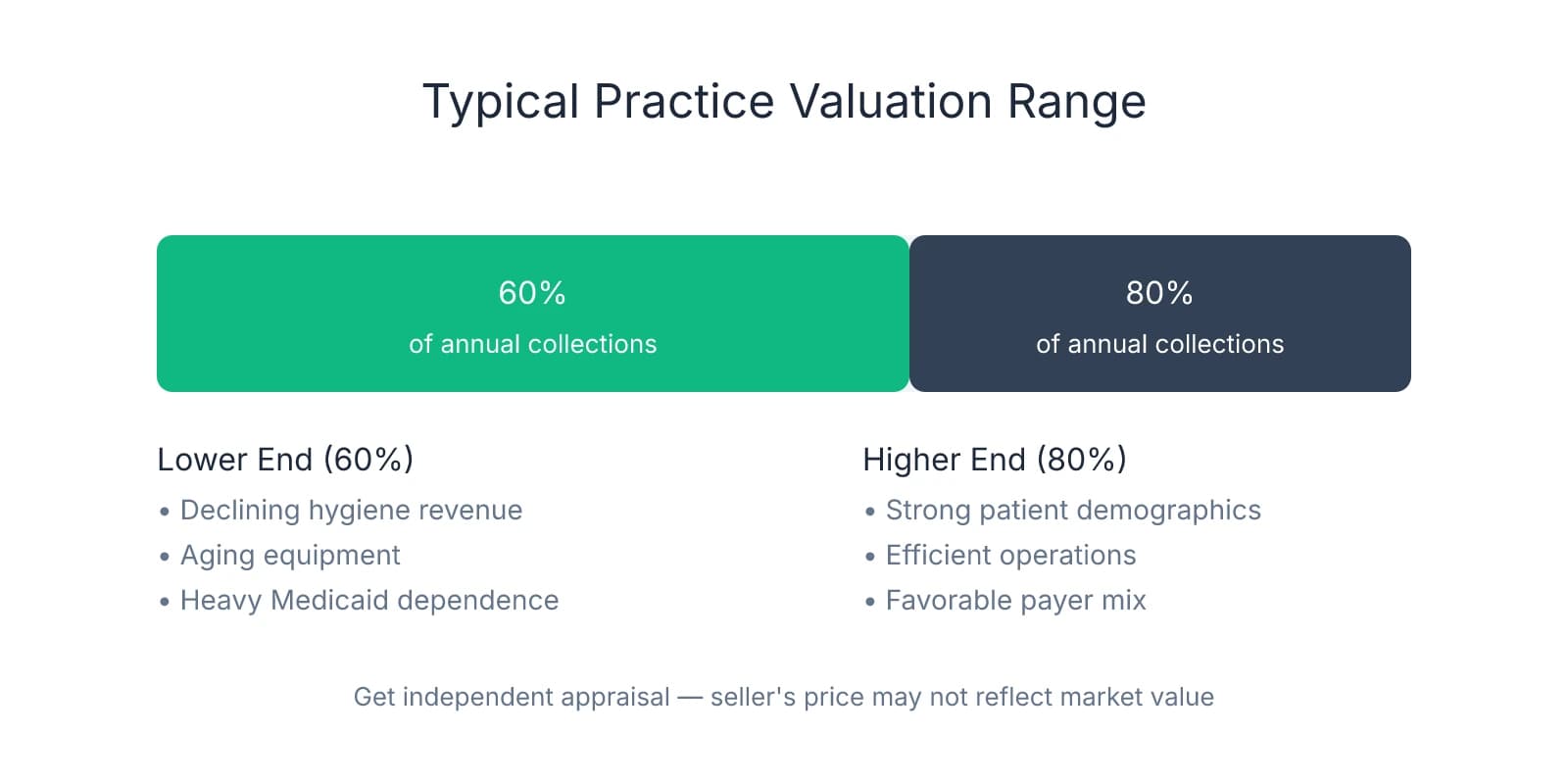

One protection many buyers overlook is getting a third-party valuation from a dental practice appraiser who has no relationship to either party. The appraiser should evaluate the practice using the same methodology they'd apply to any other transaction: collections, profitability, patient demographics, payer mix, and operational efficiency. Practices typically sell for 60-80% of annual collections, but that multiple depends on factors that have nothing to do with your relationship with the seller. A practice with declining hygiene revenue, aging equipment, or heavy Medicaid dependence sits at the lower end of that range regardless of how long you've worked there.

When the seller's asking price sits significantly above the appraised value, many buyers assume they need to either walk away or accept the gap. A third option worth considering is structuring part of the purchase price as an earnout tied to future performance. Instead of paying a premium upfront based on the seller's optimistic projections, earnouts let future results determine the final price—if the practice grows as the seller claims it will, they receive the additional payment. If it doesn't, you avoid overpaying for performance that never materializes.

The hardest part of this process isn't the math—it's the conversation. Questioning your employer's valuation feels like questioning their integrity, especially if they've framed the sale as doing you a favor. One framing that helps is treating the appraisal as protection for both parties. An independent valuation ensures the deal is sustainable—that you're not overleveraged from day one, that the bank will approve financing, and that the practice can support the debt service without forcing you to cut staff or defer maintenance. If the seller genuinely wants you to succeed, they should want the same thing.

Where buyers often get burned is assuming the seller's numbers are accurate because they've seen the practice from the inside. You've seen daily operations—you haven't seen the P&L, the tax returns, the payer contracts, or the equipment depreciation schedule. Get the independent appraisal, compare it to market benchmarks for similar practices in your region, and negotiate from data rather than sentiment.

The Due Diligence You Can't Skip—Even When You Think You Know Everything

The most dangerous assumption associates make is that working there for two or three years means they've already completed due diligence. You know the patient flow, the staff dynamics, the clinical systems—but you've never seen the lease agreement, the equipment financing terms, the accounts receivable aging report, or the vendor contracts that transfer to you at closing.

Start with the lease, even if you've worked in the same building for years. Many associates assume the lease transfers automatically because they're already practicing there. In reality, most commercial leases require landlord approval for assignment, and landlords can block the transfer entirely or demand new terms as a condition of approval. Pull the lease agreement and confirm three things: the remaining term, the assignment clause, and any personal guarantees the current owner signed. Then contact the landlord directly—not through the seller—to confirm they'll approve the assignment and under what conditions.

Next, request three years of financial statements, tax returns, and production reports, and have a dental CPA verify that collections match what you've observed. This step feels redundant when you've been watching the schedule fill for months, but reported collections and actual collections often diverge once you account for write-offs, insurance adjustments, and uncollected accounts receivable. One pattern worth paying attention to is whether the seller's tax returns show significantly lower income than the financial statements they're using to justify the asking price.

Examine all vendor contracts, equipment leases, and insurance participation agreements. These obligations transfer to you at closing and directly affect profitability. Where buyers often get burned is discovering post-closing that the digital radiography system is leased at $1,800/month for another four years, or that the practice is locked into a PPO contract with reimbursement rates 20% below regional averages. Request copies of every recurring contract and calculate the total monthly obligation.

Check for deferred maintenance, pending litigation, or regulatory compliance issues that the seller may not have disclosed. Walk through the office with a critical eye: HVAC systems that struggle in summer, operatory chairs with worn upholstery, sterilization equipment nearing end-of-life. On the compliance side, request documentation of OSHA training, infection control protocols, and any correspondence with state dental boards or health departments over the past three years. Regulatory violations or pending investigations can follow the practice through ownership transitions.

Finally, verify the active patient count and hygiene recall system independently. Don't rely on the seller's numbers without cross-checking against the practice management software. Pull a report showing patients seen in the past 18 months, then filter for patients with scheduled future appointments or active hygiene recall. Many sellers count every patient in the database as "active," including patients who haven't been seen in five years. The difference between 1,200 active patients and 800 active patients is the difference between a sustainable practice and one that needs immediate growth investment.

Structuring the Transition to Protect Both the Deal and the Relationship

The transition period is where most associate buyouts either solidify or unravel. You've negotiated the price, completed due diligence, and secured financing—but the deal's success depends on how the first 60–90 days unfold.

One protection many buyers overlook is negotiating a structured transition period with defined responsibilities, not just a vague agreement that the seller will "help out for a while." The transition clause should specify how many days per week the seller will be present, what their clinical role will be, and how they'll introduce you to patients as the new owner. Most buyers find 60–90 days sufficient for patient handoff and operational transfer, but the timeline should match the practice's complexity.

The seller's role during transition should focus on patient introduction and operational handoff—not continued full-time clinical production. Where transitions often go sideways is when the seller continues practicing at full capacity, creating confusion about who actually owns the practice. Structure the transition so the seller's schedule gradually decreases while yours increases, giving patients a clear signal that leadership has changed hands.

Consider seller financing or an earnout structure if the asking price stretches your cash reserves. Seller financing typically covers 10–30% of the purchase price, with the seller receiving monthly payments over 3–5 years rather than full payment at closing. This reduces your upfront cash requirement while aligning the seller's incentives with the practice's continued success. Earnouts work similarly, tying a portion of the purchase price to future revenue benchmarks.

Communicate the ownership change to staff early and clearly, ideally before closing. Your existing relationships with the team are an advantage, but staff need to understand the new dynamic before the transition begins. Schedule a team meeting where you and the seller jointly announce the change, outline the transition timeline, and address compensation or role changes. Staff uncertainty drives turnover, and losing your front desk coordinator or lead hygienist during the first 90 days can destabilize operations faster than any other factor.

Plan patient communication carefully. Most patients already know you, but they need reassurance that care quality and office culture will remain consistent. The seller should send a letter or email introducing you as the new owner, emphasizing continuity rather than change. For patients who haven't seen you yet, the seller's personal introduction during their next appointment carries more weight than any written communication.

Start the conversation with your employer early, but don't commit to terms until you've completed due diligence and secured financing approval. Many associates feel pressure to agree quickly out of fear the seller will list the practice publicly or pursue another buyer. Express serious interest, request the financial documents you need for evaluation, and make it clear you're moving forward in good faith—but don't sign a letter of intent until you've done the work to confirm the deal makes sense.

If you're considering this path, the first step is requesting a current profit-and-loss statement, the lease agreement, and a list of all active vendor contracts. That request signals intent without commitment, and the seller's response tells you whether they're prepared for a serious transaction or still treating the idea as hypothetical. From there, engage a dental-specific CPA and attorney to guide the process—your relationship with the seller is an asset, but it shouldn't replace the professional advisors who protect your interests when the relationship complicates negotiation.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- patient attrition often spikes— ncbi.nlm.nih.gov

- What Went Wrong: We Disagreed on the Value of the Practice— ada.orgIndustry

- What Went Wrong: We Disagreed on the Value of the Practice— ada.orgIndustry

- Earnouts in dental practice acquisitions: What you need to know— www.oralhealthgroup.comIndustry

- reported collections and actual collections often diverge— dentaleconomics.com

- What Went Wrong: We Disagreed on the Value of the Practice— ada.orgIndustry

- Associate Buy-In Guide: Essential Steps For a Smooth Transition ...— www.dmcounsel.com

Frequently Asked Questions

Ready to transition from associate to owner?

Buying your employer's practice is a significant step that requires expert guidance. Minty Plus provides hands-on support throughout the acquisition process and beyond, helping you navigate the transition from associate to practice owner with confidence.