Buying a Dental Practice with No Money Saved

Co-Founder, Minty Dental

In Summary

- 100% financing for dental practice acquisitions is the industry standard, not a special promotion — lenders routinely cover the full purchase price with no down payment required

- Dental practice default rates are under 1%, which is why specialized lenders offer terms unavailable in almost any other industry

- The real requirement isn't a down payment — it's post-closing liquidity: cash sitting in your account as a buffer after the deal closes

- Working capital (typically up to 15% of the loan amount) can often be rolled into the loan, meaning your total financing can exceed the purchase price

- The gap between "no down payment" and "no money at all" is where most buyers get stuck — and this article maps out exactly what the minimums look like and how to meet them

100% Financing Is Real — But It Doesn't Mean Zero Requirements

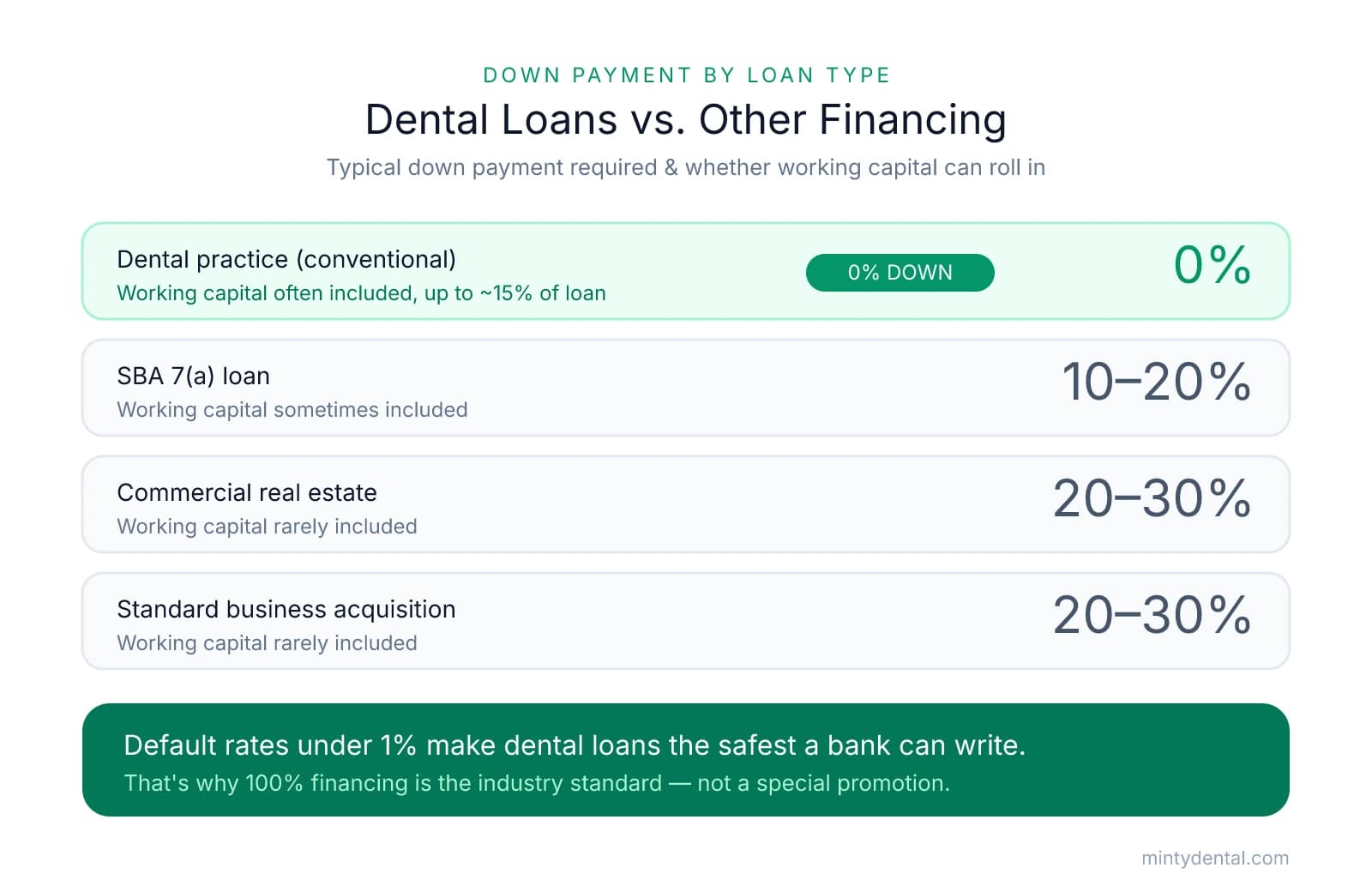

Dental practice loans: one of the only business financing products where 100% of the purchase price is routinely financed with no equity contribution required. That's not a marketing claim — it's how the industry actually works, and understanding why helps clarify what lenders are genuinely asking of you.

The reason banks extend these terms comes down to risk. According to the ADA, dental practices carry a default rate of less than 1% — a figure that makes them among the safest business loans a bank can write. That's why specialized dental lenders are willing to cover the full purchase price, and often roll in working capital on top of it, in a way that would be unthinkable for most other small business acquisitions.

Here's how dental practice loans compare to other common financing products:

| Loan Type | Typical Down Payment | Working Capital Included? |

|---|---|---|

| Dental practice (conventional) | 0% | Often yes, up to ~15% of loan |

| SBA 7(a) loan | 10–20% | Sometimes |

| Commercial real estate | 20–30% | Rarely |

| Standard business acquisition | 20–30% | Rarely |

So if 100% financing is real, why does it still feel like you need money? The answer is a distinction that trips up many first-time buyers: no down payment is not the same as no money needed.

Lenders aren't asking you to hand over cash at closing. What they want to see is cash sitting in your account after closing — a liquidity buffer that signals you can weather the first few months if collections run slower than projected. Think of it less as a cost of entry and more as proof of financial stability. The purchase price gets financed in full; what lenders are actually evaluating is whether you can survive a temporary dip in revenue without missing payroll or a loan payment.

Working capital — typically up to 15% of the loan amount — can often be folded into the financing itself, which means your total loan can exceed the practice purchase price. That's a meaningful detail: it's possible to walk into ownership with operating cash already in place, borrowed as part of the same deal. How that structure compares to SBA versus conventional loan options is worth understanding before you approach a lender, since the two products handle working capital and qualification criteria differently.

The instinct that brought you to this article — that ownership might be possible even without significant savings — is correct. But the path forward requires understanding exactly what "no money down" does and doesn't cover.

What Lenders Actually Require When You Have Little Saved

The distinction that matters most here isn't how much you've saved — it's what form those savings take. Specialized dental lenders don't require a down payment, but they do want to see roughly 10% of the loan amount sitting in accessible accounts after closing. On a $700,000 practice, that means $70,000 in liquid assets that remain in your accounts once the deal is done — not money you spend to close the deal.

That last part is worth pausing on. The out-of-pocket costs at closing — legal fees, due diligence, entity formation — typically run $15,000–$20,000. That's real money, but it's a fraction of the full liquidity threshold. The $70,000 isn't consumed by closing; it's a reserve the lender wants to see you keep.

What Counts as Liquid — and What Doesn't

Not all assets qualify. As the American Academy of Periodontology's lending partner Panacea explains, lenders assess liquidity as money you can access without penalty — and that distinction cuts out more than most buyers expect.

| Counts as Liquidity | Does NOT Count |

|---|---|

| Savings & checking accounts | 401(k) / Traditional IRA |

| Taxable brokerage accounts | Roth IRA |

| Money market accounts | Home equity |

| Stocks, bonds, CDs | Any account requiring penalties or waiting periods to access |

| Documented gift funds from family | Informal loans from family or friends |

Gift funds from family are worth noting specifically. As Menlo Transitions advises, the money needs to be documented as a gift — not a loan — because lenders treat undocumented family transfers as debt, which works against your application rather than for it.

Two Levers That Can Reduce the Threshold

The 10% figure isn't fixed. Two factors tend to give lenders room to flex:

-

High-income production. Associates generating $400,000 or more annually often qualify for reduced liquidity requirements — sometimes in the 5–7% range — because their income signals lower default risk.

-

The practice's own cash flow. Lenders underwrite the acquisition as much as they underwrite the buyer. A practice with 40% overhead, stable collections, and a debt service coverage ratio above 1.25x represents meaningfully less risk than a marginal practice — and lenders price that accordingly. Flexibility tends to come from pairing strong personal income with a well-performing practice, rather than trying to compensate for a weak practice with savings alone.

Understanding what banks are actually evaluating when they review your file — beyond the liquidity number — can help you position your application more strategically before you ever sit down with a lender.

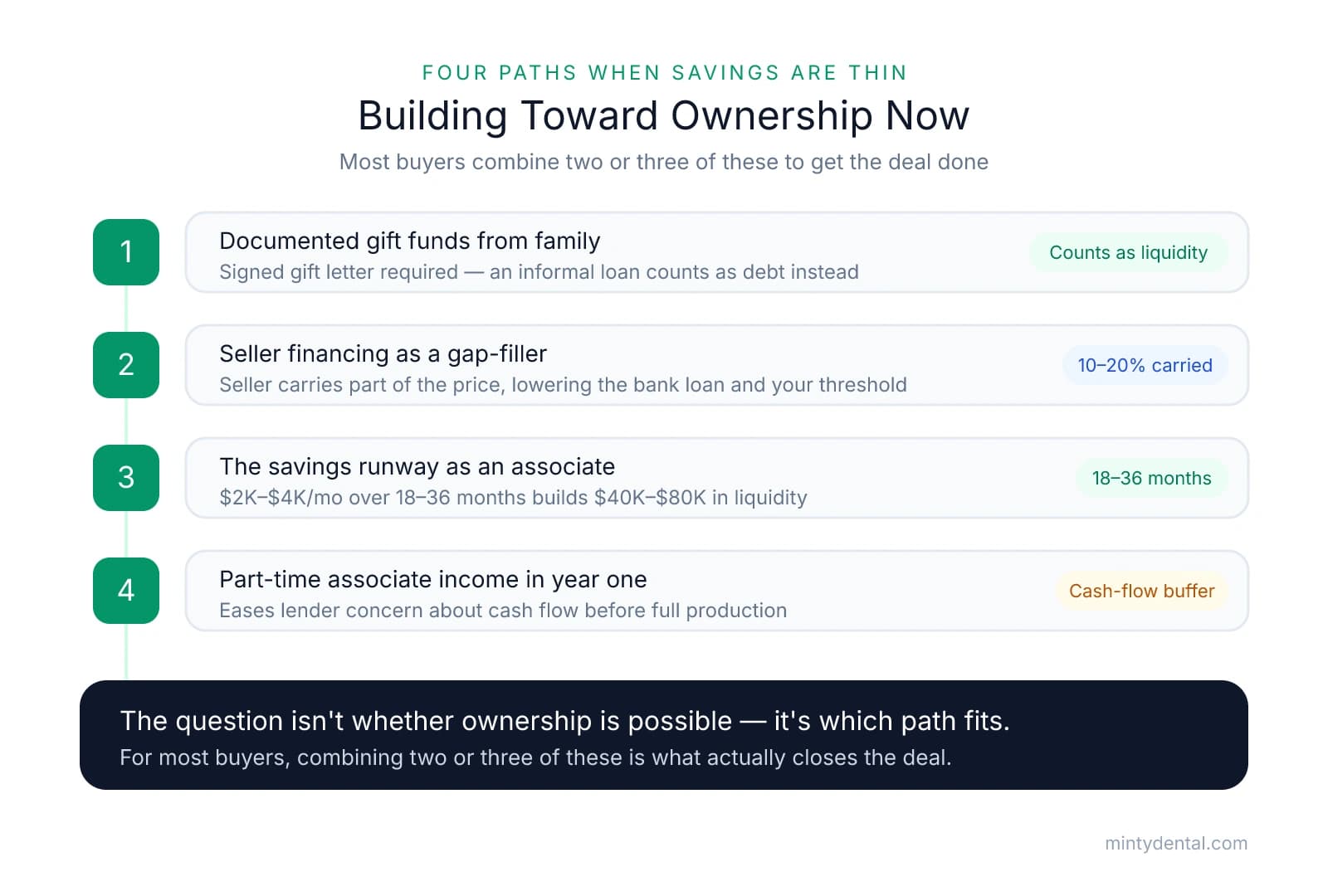

Paths Forward When You Genuinely Haven't Saved Yet

"Save more" is technically correct advice — and also the least useful thing to hear when you're trying to figure out whether ownership is possible now. What follows are four concrete paths buyers actually use when savings are thin, along with what each requires to work.

1. Documented Gift Funds from Family

Most dental lenders will accept gift funds from family members as qualifying liquidity — the key word being documented. A signed gift letter confirming that no repayment is expected is typically required, because lenders treat undocumented family transfers as debt. A $30,000 gift that's properly documented counts toward your liquidity threshold; the same $30,000 framed as an informal loan works against your application.

If family support is a realistic option, it's worth having that conversation early — and looping in your lender before the funds move, so the documentation is in place from the start.

2. Seller Financing as a Gap-Filler

In some deals, the seller agrees to carry a portion of the purchase price — typically 10–20% — as a seller note. This reduces the bank loan amount, which in turn lowers the liquidity threshold the lender requires of you.

A pattern worth understanding: seller financing tends to appear when a practice has characteristics that make conventional lenders cautious — a rural location, a specialty mix with thin reimbursement, or declining collections. That doesn't automatically make it a bad deal, but it's worth asking why the seller is willing to carry a note. When the answer is tax strategy or a genuine desire to support the buyer's success, seller financing can work well for both sides. When it's because the bank won't fully fund the deal, that's a signal to dig deeper into the financials before proceeding.

3. The Savings Runway: 18–36 Months as an Associate

This is the path lenders tend to respect most, and the one that produces the smoothest closings. Associates who spend 18–36 months saving $2,000–$4,000 per month can realistically build the $40,000–$80,000 in liquidity most lenders want to see for a $500,000–$800,000 acquisition. That's not an indefinite delay — it's a defined window with a clear endpoint.

One nuance lenders pay attention to: consistent saving over time carries more weight than a large deposit that appears shortly before application. A pattern of steady accumulation signals financial discipline in a way that a sudden balance spike doesn't.

4. Maintaining Part-Time Associate Income in Year One

Some buyers negotiate to keep a part-time associate position during their first year of ownership. This doesn't solve the liquidity question at closing, but it can meaningfully reduce lender concern about personal cash flow — particularly in the months before the acquired practice reaches full production. It also provides a buffer against the unexpected first-year expenses that catch many new owners off guard.

If your savings are genuinely minimal today, the question isn't whether ownership is possible — it's which of these paths fits your timeline. For most buyers, a combination of two or three of them is what actually gets the deal done.

How to Assess Whether You're Ready to Approach a Lender Now

Everything covered in this article comes down to one practical question: where do you stand today, and what should you do next? Here's a concrete framework — the four criteria lenders actually evaluate, and a decision rule for what to do based on where you land.

The four things lenders look at:

- Credit score — 700+ is the comfortable range. Below 680 creates friction and may require explanation, but it's not automatically disqualifying — lenders weigh it alongside the other three factors.

- Post-closing liquidity — roughly 10% of the loan amount sitting in accessible accounts after closing. As covered earlier, this threshold can flex downward for high-income producers or particularly strong practices.

- Income and production history — lenders want evidence you can replicate the seller's production. Two years of W-2s or 1099s is the standard ask, and higher personal production gives you more negotiating room on liquidity.

- Practice quality — a debt service coverage ratio above 1.25x, overhead under 65%, and stable or growing collections. Lenders are underwriting the practice as much as they're underwriting you.

The decision rule:

- 3 of 4 criteria met — talk to a lender now. You're likely closer to approval than you think, and a lender conversation will tell you exactly what the remaining gap looks like.

- 2 or more criteria are gaps — a 12-month preparation plan is more realistic. Focus first on whichever gap is most closable: credit score improvements typically take 3–6 months; liquidity gaps respond to the savings runway approach outlined in the previous section.

One thing the ADA recommends is speaking with at least three dental-specific lenders before beginning your search — their flexibility on liquidity, credit, and structure varies more than most buyers expect, and a lender who passes on your file may simply have tighter internal guidelines than a competitor.

The most underused move in this process is talking to a lender before you find a practice. That conversation is free, takes less than an hour, and ends with a precise picture of what you need to qualify. Many buyers who go through it discover they're already at 3 of 4 — and that the 10% liquidity requirement sounds large until they realize it stays in their account. If the financial weight of a $700,000–$1M loan feels daunting, that early lender conversation tends to replace anxiety with a specific target — which is a much more useful thing to carry into your search.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Demystifying the Practice Loan Process | American Dental Association— ada.orgIndustry

- What Is Liquidity & Why Is It Important For Practice Ownership?— members.perio.orgIndustry

- Credit and Liquidity Tips for Dental Practice Buyers— www.menlotransitions.comIndustry

- debt service coverage ratio— sba.gov

- What Dentists Need to Know About Seller Financing— www.dentalbuyeradvocates.comIndustry

Ready to buy without savings?

Acquiring a dental practice without substantial savings is possible with the right guidance and financing strategies. Minty's acquisition experts help you navigate the entire process from search to closing, with no upfront fees required.