Dental Associate Buy-In vs. Buying Outside: Which Is Better?

Co-Founder, Minty Dental

In Summary

- A dental associate buy-in means purchasing a minority ownership stake — typically 10–20% — in the practice where you already work, with a phased path toward full ownership over time.

- The buy-in feels like the safer, simpler route because the practice is already familiar, but it introduces structural risks — around valuation, control, and exit terms — that a clean outside purchase avoids.

- Buying an independent practice on the open market gives you full ownership from day one, market-rate pricing, and complete autonomy over clinical and business decisions.

- Neither path is objectively better — the right choice depends almost entirely on whether the specific deal in front of you is structured in your favor. Many aren't.

- The three dimensions that matter most when comparing both paths: financial structure, control, and trajectory — where the deal actually leads over a 5–10 year horizon.

The Buy-In Isn't Always the Easier Path to Ownership

A dental associate buy-in is a transaction where an associate purchases a minority ownership stake — typically 10–20% — in the practice where they're already employed, with a structured path toward acquiring greater ownership over time. It's a form of phased succession: the seller retains income and clinical presence while the associate gradually steps into ownership.

For many associates, this feels like the obvious first move. You already know the patients, the staff, the systems, and the seller. There's no cold search process, no patient acquisition risk, and often a built-in mentor willing to walk you through the business side of ownership. Compared to buying a stranger's practice off the open market, the buy-in can feel lower-stakes almost by definition.

But "familiar" and "favorable" aren't the same thing.

The buy-in's appeal is real — lower initial capital requirements, an established revenue base, and continuity that outside buyers have to build from scratch. What's easier to miss are the structural trade-offs baked into many of these deals: minority ownership that limits decision-making authority, valuation methods that favor the seller, and partnership agreements that can leave the path to full ownership murkier than it appeared at the start.

The outside purchase path looks harder on the surface — more upfront capital, a longer search, and the willingness to walk into a practice where you're the unknown variable. But it also offers something the buy-in rarely does: full ownership from day one, a clean governance structure, and pricing set by the open market rather than a seller with a personal stake in the number. For associates weighing both options, the question of whether to buy where you work or look elsewhere often comes down to deal terms more than familiarity.

A pattern worth paying attention to: many buy-in agreements are drafted with the seller's succession timeline in mind, not the associate's ownership goals. That's not bad faith — it's incentive alignment. Associates who have navigated this firsthand note that a 10% stake often comes with little real decision-making power and compensation structures that don't meaningfully change post-buy-in — a dynamic worth pressure-testing before signing.

Throughout this article, the comparison between these two paths runs along three dimensions that tend to determine the outcome:

- Financial structure — what you're paying, what you're getting, and how the valuation was reached

- Control — what decisions you can actually make as a minority owner, and when that changes

- Trajectory — where the deal leads in five or ten years, and whether the path to full ownership is real or theoretical

Getting clear on all three — before signing anything — is what separates a buy-in that builds toward genuine ownership from one that keeps you in a permanent associate role with equity paperwork attached.

What You're Actually Paying For in a Buy-In (And Where the Price Gets Inflated)

Before evaluating any buy-in offer, it helps to understand what the purchase price is actually made of — because the composition matters as much as the number itself.

Goodwill in dental practice sales: Goodwill — the intangible value of an established patient base, reputation, and earning power — typically represents 60–80% of a dental practice's total purchase price. In a buy-in, the majority of what you're paying for is intangible. And in many cases, some of that goodwill was built by you.

This is the "double-paying" problem. If you've been producing in the practice for one or two years, your clinical work has contributed to collections, patient retention, and the revenue figures that now underpin the valuation. You helped create the goodwill — and you're being asked to buy it back. That's not necessarily a dealbreaker, but it's worth quantifying before you agree to a price.

The Valuation Method Determines the Price

How a practice is valued matters enormously, and different methodologies can produce materially different numbers. Common approaches include capitalized excess earnings, multiple-of-collections, and asset-based methods — and most formal valuations average several together to build confidence in the result.

The problem in a buy-in context: the seller typically selects the methodology, and sellers naturally gravitate toward the approach that produces the highest number. A multiple-of-collections calculation on a high-revenue practice can generate a valuation that looks very different from a capitalized earnings approach on the same practice. Neither is inherently wrong — but the spread can represent hundreds of thousands of dollars in purchase price.

Understanding how a patient base is priced into that goodwill figure is one way to stress-test whether the number you're being quoted reflects real transferable value or optimistic assumptions.

The Appraisal Gap

In an outside purchase, independent appraisal is standard. A buyer commissions their own valuation, compares it against the asking price, and negotiates from there. In a buy-in, many associates skip this step — not because they don't know better, but because asking for a second opinion feels like an accusation.

It isn't. According to the ADA, what's included in the valuation — goodwill, equipment, accounts receivable, real estate — must be explicitly defined, and ambiguity here is a consistent source of post-closing disputes. Getting an independent appraisal is the same due diligence any outside buyer would conduct as a matter of course.

Buy-In vs. Outside Purchase: Key Financial Dimensions

| Dimension | Associate Buy-In | Outside Purchase |

|---|---|---|

| Valuation methodology | Seller-selected; often favors higher result | Negotiated; buyer can commission independent appraisal |

| Goodwill exposure | May include goodwill the associate helped build | Priced at arm's length; no prior contribution |

| Independent appraisal | Often skipped due to relationship dynamics | Standard practice |

| Market leverage | Associate is typically the only buyer | Buyer can compare multiple practices and walk away |

| Financing options | Sometimes seller-financed with less lender scrutiny | Full range of SBA and conventional lending available |

The financing dimension is worth pausing on. Outside purchases typically go through formal lender underwriting — which, while more rigorous, also means a bank independently validates that the price makes sense. In a buy-in, seller financing can bypass that check entirely, leaving the associate without the market signal that lender scrutiny provides. A practice purchase price allocation calculator can help model the downstream tax and loan implications before you commit to a number.

The Control Problem: What Minority Ownership Actually Means Day-to-Day

Buying into a practice at 20% doesn't mean 20% of the decisions. In most buy-in structures, the senior partner retains majority control — and with it, the authority to override the junior partner on nearly every significant operational and financial choice. The gap between ownership on paper and authority in practice is one of the most important things to understand before signing.

The friction tends to concentrate in three areas:

- Capital expenditures — new equipment, technology upgrades, facility renovations. These decisions affect overhead and cash flow directly, but in most agreements, the senior partner controls them.

- Hiring and staffing — who gets hired, who gets let go, and at what compensation. A minority owner who disagrees with a staffing decision often has no formal mechanism to block it.

- Clinical systems — scheduling philosophy, fee schedules, insurance participation, and the overall patient experience. These shape the practice's culture and revenue model, but they're rarely within a minority owner's authority to change unilaterally.

The result is a position that can feel more like a well-compensated associate than a genuine owner — until the buyout of the remaining interest is complete.

Dental partnerships fail at a higher rate than solo practices, according to Ideal Practices, and the most common causes aren't financial — they're structural. Ambiguous decision-making frameworks create slow-building resentment. Production imbalances, where one partner generates significantly more revenue but both share overhead equally, create a different kind of friction. Neither problem is obvious at signing. Both tend to surface within a few years.

Profit distribution compounds this. Some agreements split profits proportionally to ownership percentage; others split equally regardless of production; others split by collections. Each model creates different incentives and different pressure points. An associate producing 60% of collections but receiving 20% of profits will eventually do the math — and that math tends to surface at the worst possible time.

The Path to Full Ownership Must Be Written In — Not Assumed

Many associates enter a buy-in assuming the path to full ownership will unfold naturally as the senior partner ages toward retirement. In practice, that transition requires a pre-agreed timeline, a defined valuation methodology for the future buyout, and explicit language about what triggers the option. Without those terms in the original agreement, the senior partner has no contractual obligation to sell.

Menlo Transitions identifies ambiguous agreements as the most common cause of buy-in failures — not bad intentions, but vague terms that leave critical questions unanswered until they become disputes.

This is where an outside purchase offers something that doesn't show up in any price comparison: autonomy from day one. When you buy an independent practice, you set the clinical culture, choose the staff, control the schedule, and determine the growth strategy. For associates thinking through whether they're ready to step into that full decision-making role, the clinical readiness framework is worth working through before either path gets too far along.

A well-structured buy-in with a seller who genuinely wants to exit can absolutely work — the key word is "structured," with governance terms, a buyout timeline, and a pre-agreed valuation formula that protects both sides from the ambiguity that ends most partnerships early.

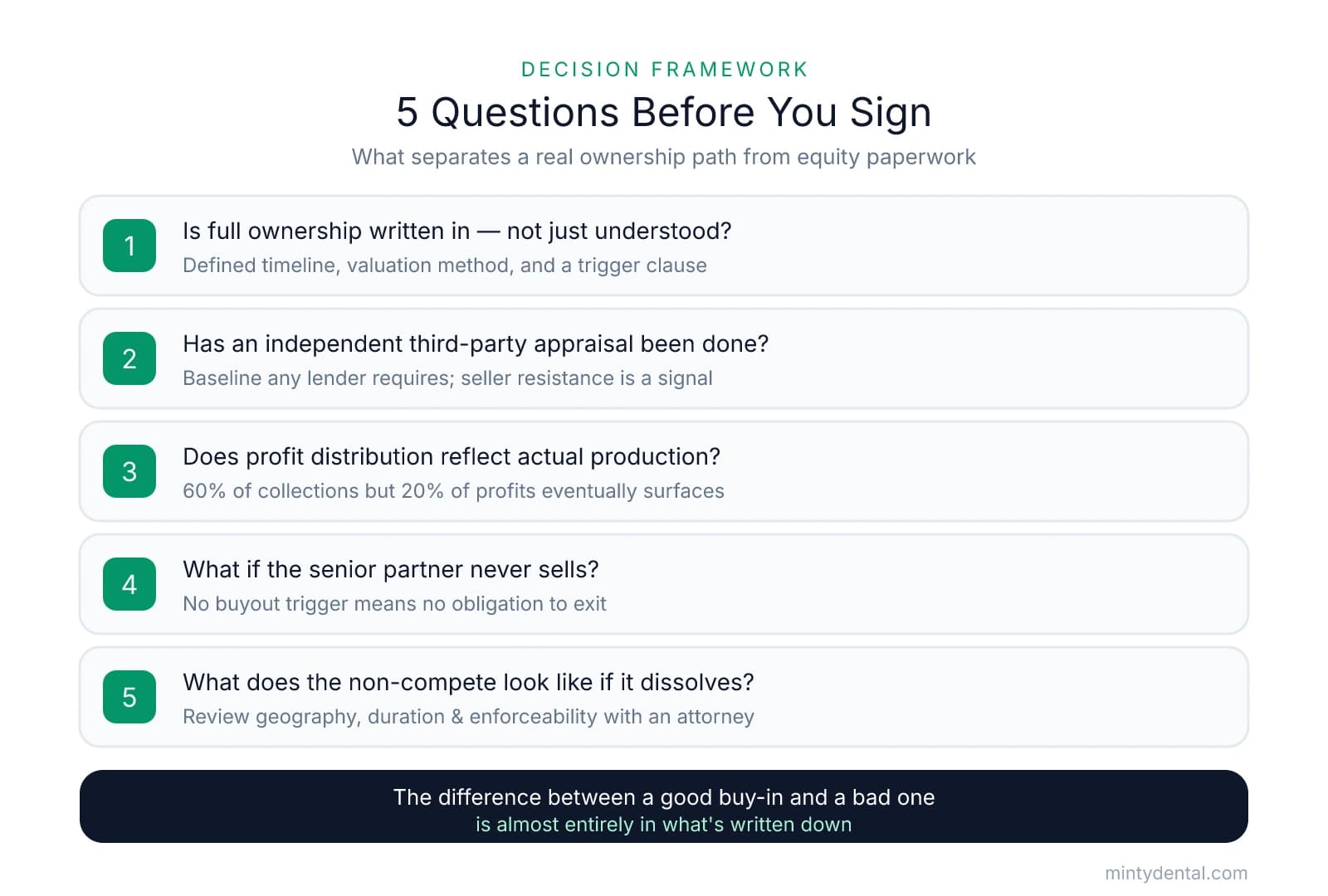

How to Decide: A Framework for Evaluating the Buy-In Deal in Front of You

Everything covered above comes down to one practical question: is the specific deal in front of you worth taking, or is the open market a better move?

These five questions tend to separate a well-structured buy-in from one that keeps you in a permanent associate role with equity paperwork attached.

1. Is the path to full ownership written into the agreement — not just understood? A verbal commitment from a seller you trust is not a buyout timeline. Confirm that the agreement specifies a defined timeline for the senior partner's exit, a pre-agreed valuation methodology for the future buyout, and a trigger clause that compels the sale if the senior partner doesn't act. Without these, you have goodwill — not a contract.

2. Has an independent third-party appraisal been completed? The relationship with the seller doesn't change what the practice is worth. Requesting an independent appraisal isn't adversarial — it's the baseline any lender would require on an arm's-length transaction. If the seller resists it, that's a signal worth taking seriously.

3. Does the profit distribution model reflect actual production? Run the numbers on your current collections relative to what you'd receive under the proposed split. The associate pay calculator is useful here for comparing your current compensation against projected ownership income under different distribution structures.

4. What happens if the senior partner never sells the remaining stake? If the agreement doesn't include a buyout trigger — a clause that compels the sale under defined conditions — the senior partner has no contractual obligation to exit. Confirm this language exists before assuming the transition will happen naturally.

5. What does the non-compete look like if the partnership dissolves? A restrictive non-compete can effectively trap you in a market if the partnership falls apart. Review the geography, duration, and enforceability carefully — ideally with a dental attorney — before signing.

When the Outside Purchase Is the Stronger Move

Three signals tend to indicate that going to market is the better path:

- The buy-in price is at or near what an independent practice of comparable size would cost on the open market

- The path to full ownership is described in general terms rather than written into the agreement with a timeline and methodology

- The senior partner has no defined exit date and isn't genuinely planning to leave within a horizon you can accept

The buy-in isn't inherently the worse option. A well-structured deal with a seller who genuinely wants to exit — and has committed to a clear timeline, pre-agreed buyout terms, and a fair independent valuation — can be an excellent path to ownership. The difference between a good buy-in and a bad one is almost entirely in what's written down. The ADA recommends building your legal and accounting team early in the process — before you find the practice — so you're positioned to evaluate contracts without pressure when the right opportunity appears. The associate who goes in knowing what to negotiate is in a fundamentally different position than one who assumes the deal is fair because the relationship is good.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Should I buy in for 10% as an associate? : r/Dentistry - Reddit— www.reddit.com

- Dental Practice Goodwill: How It's Valued and Why It Matters— www.usdentalpractices.comIndustry

- A dentist's guide to dental practice valuation methods | Baker Tilly— www.bakertilly.comIndustry

- Buying or Selling a Dental Practice, Start with an Accurate Valuation— ada.orgIndustry

- Dental Partnership Contracts: What Associate Dentists Must ...— idealpractices.comIndustry

- Common Mistakes in Dental Associate Buy-Ins— www.menlotransitions.comIndustry

- How to purchase with confidence | American Dental Association— www.ada.orgIndustry

Ready to own your dental practice?

Whether you're considering buying in as an associate or purchasing independently, finding the right practice is the first step. Explore available dental practices nationwide and connect with ownership opportunities that match your goals.