When Is the Right Time to Buy a Dental Practice?

Co-Founder, Minty Dental

In Summary

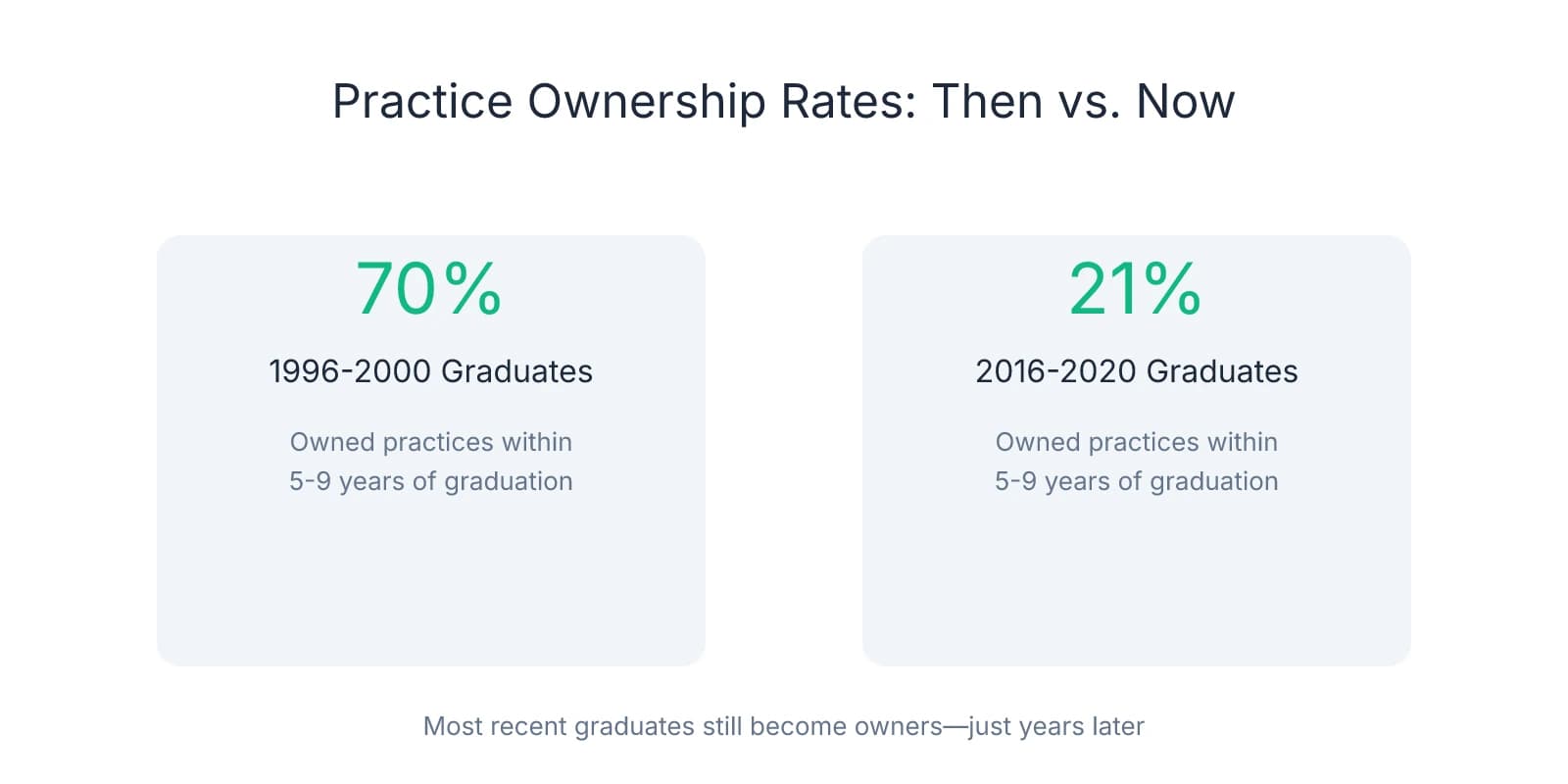

- Only 21% of dentists who graduated between 2016-2020 own practices 5-9 years into their careers, compared to 70% of 1996-2000 graduates at the same stage—most eventually become owners, just years later than previous generations.

- The delay costs more than time: buyers who purchase earlier consistently report wishing they'd started sooner, citing years of lost equity and autonomy they can't recover.

- Student debt, lack of experience, and waiting for ideal market conditions are common reasons for postponing ownership, but these rarely resolve on their own—readiness comes from meeting specific clinical, financial, and personal markers, not waiting for perfect circumstances.

- Most dentists who delay ownership do so not because they lack the fundamentals, but because they're uncertain what readiness actually looks like in practical terms.

Most Dentists Wait Longer Than They Need To—And Regret It

Pull up the career timelines of dentists who graduated in the late 1990s and compare them to those who finished school in the last decade. The contrast is stark: 70% of 1996-2000 graduates owned practices within 5-9 years, while only 21% of 2016-2020 graduates hit that milestone at the same career stage. The gap isn't about ambition or capability—it's about timing. Most dentists in the more recent cohort still become owners eventually. They just wait longer to do it.

That delay has a cost. Talk to buyers who purchased practices in their late twenties or early thirties, and a pattern emerges: nearly all of them wish they'd done it sooner. Not because the deal was easy, but because the years spent as an associate—earning someone else's profit margin, building someone else's patient base—are years they can't get back. Equity compounds. Clinical autonomy shapes how you practice. The longer you wait, the more of both you leave on the table.

The reasons for postponing ownership sound rational on the surface. Student debt sits in the six figures for most new graduates. Clinical experience feels thin after two years of associateship. Market conditions shift, interest rates fluctuate, and the idea of taking on more debt to buy a practice can feel overwhelming when you're still paying down loans from school. But here's what those reasons often mask: uncertainty about what readiness actually looks like. It's not that you lack the fundamentals—it's that you're not sure which fundamentals matter, or how to measure whether you've cleared the threshold.

The dentists who move into ownership earlier aren't necessarily more confident or better capitalized. What separates them is clarity around three core areas: clinical competence, financial positioning, and personal circumstances. They know what procedures they need to handle independently, what their debt-to-income ratio should look like, and whether their life situation can absorb the demands of ownership. They're not waiting for perfect conditions—they're checking whether they meet the markers that make ownership viable.

One pattern worth noting: the "right time" rarely announces itself. You won't wake up one day feeling fully ready. What changes is your ability to assess readiness using concrete criteria rather than vague feelings of preparedness. That shift—from waiting for confidence to evaluating specific markers—is what moves most buyers from consideration to action.

Three Readiness Markers That Matter More Than Market Timing

Most buyers treat readiness as a feeling—something they'll recognize when it arrives. In practice, it's a checklist. Three areas determine whether you're positioned to own: clinical competence, financial capacity, and personal circumstances. These aren't aspirational goals. They're threshold criteria. Once you meet them, waiting doesn't improve your position.

Clinical Readiness: Can You Sustain What You're Buying?

The core question isn't whether you're a skilled clinician—it's whether you can maintain the revenue stream that justifies the purchase price. Lenders and sellers both want to see that you can produce at roughly 80% of the seller's historical output. That benchmark accounts for the reality that some patients will leave during any ownership transition, and your hand speed in the first year will likely trail an experienced owner who's been in the chair for decades.

What gets you to that 80% threshold? Three things: procedural confidence, production history, and speed. You need to handle the procedures that generate the majority of the practice's revenue—crowns, endodontics, extractions, and basic surgical work—without referral delays that disrupt patient flow. You need a track record showing you can generate sustainable collections, typically demonstrated through 12-24 months of consistent associate production. And you need the hand speed that comes from repetition, which for most strong producers develops within 1-2 years post-graduation.

If you're fresh out of residency, that timeline matters. A buyer who graduated 18 months ago and is producing $400,000 annually as an associate is often in a stronger position than someone five years out who's been working part-time or in a low-volume setting. Clinical readiness isn't about years since graduation—it's about procedural volume and revenue consistency.

Financial Positioning: Less Cash Than You Think, More Structure Than You Expect

The assumption that ownership requires massive liquid reserves keeps more buyers on the sidelines than any other misconception. In reality, most lenders want to see $50,000 in savings or 10% of the purchase price, whichever is less. A $600,000 practice doesn't require $60,000 down—it requires $50,000. A $400,000 practice needs $40,000. The cash requirement is a credibility signal, not a down payment in the traditional sense.

Credit matters more than cash reserves in most cases. Lenders typically look for scores around 680-700 as a baseline, though stronger credit can offset thinner production history or higher debt-to-income ratios. If your score sits below that range, the fix is straightforward: pay down revolving balances, avoid opening new credit lines, and let time resolve any past late payments. Six months of disciplined credit management can shift your financing options significantly.

The third component—production history—overlaps with clinical readiness but serves a different function here. Lenders want to see that you've generated consistent revenue over at least 12 months, ideally in a setting that mirrors the practice you're buying. If you've been producing $35,000 monthly as an associate and the practice you're evaluating collects $50,000 monthly, the math works. If your production has been sporadic or part-time, expect lenders to ask more questions about sustainability.

Personal Timing: Life Stage and Geographic Commitment

Ownership doesn't require you to have your entire life mapped out, but it does require clarity on two fronts: where you're willing to commit geographically, and how ownership fits into your near-term personal plans.

The geographic question is simpler than it sounds. Can you commit to staying in the area for at least five years? That's the timeframe most lenders use when evaluating risk, and it's roughly how long it takes to stabilize a practice post-acquisition, build patient loyalty, and position yourself for a profitable exit if you choose to sell. If you're uncertain whether you'll stay in the region, ownership introduces risk that an associateship doesn't.

Family planning sits in the same category. Ownership in your late twenties or early thirties often means navigating the first two years of practice ownership—the period with the steepest learning curve and longest hours—while also managing young children or planning for them. Neither path is wrong, but the timing affects your capacity to handle the operational demands that come with being both clinician and business owner. Many buyers find that purchasing before starting a family or after children reach school age reduces the strain on both fronts.

Work-life balance expectations need recalibration in the first 24 months. New owners typically work longer hours than they did as associates, not because the clinical schedule is heavier, but because administrative responsibilities—payroll, supply ordering, staff management, marketing—don't pause when you leave the operatory.

These markers aren't perfection standards. They're threshold criteria. Once you meet them, additional waiting rarely strengthens your position. Market conditions fluctuate—interest rates rise and fall, practice availability shifts by region—but those variables matter far less than whether you're clinically capable, financially positioned, and personally ready to absorb what ownership requires.

What Waiting Actually Costs You

Every year you spend as an associate is a year you're not building equity. That's not a motivational platitude—it's a mathematical reality that compounds over the length of your career. A practice owner who buys at 30 and sells at 60 builds 30 years of equity appreciation, patient base growth, and operational improvements that translate directly into sale proceeds. An associate who waits until 40 to purchase cuts that equity-building window in half, and there's no mechanism to recover those lost years.

The income differential tells the same story. Owners consistently report higher lifetime earnings than long-term associates, with the gap widening as careers progress. Part of that comes from profit margins—owners capture the full revenue from their clinical work minus overhead, while associates typically earn 30-35% of their production. But the larger driver is equity accumulation. When you sell a practice, you're liquidating decades of value creation that associates never participate in. A buyer who purchases at 32 and sells at 62 might walk away with $800,000-$1.2 million in sale proceeds on top of 30 years of higher annual income. An associate who retires at the same age walks away with nothing beyond their final paycheck.

One scenario that keeps buyers waiting longer than necessary: the belief that student debt needs to drop significantly before ownership makes sense. For most graduates carrying $300,000-$400,000 in loans, aggressive repayment could take 10-15 years. That's a decade or more of your most productive earning years spent as an associate, during which you're building zero equity and deferring the income upside that comes with ownership. The math rarely supports this approach. Practice loans and student debt can coexist—lenders evaluate your debt-to-income ratio and production capacity, not whether your student loans are paid off.

Interest rate timing follows a similar pattern. Buyers who postpone purchases waiting for rates to drop are making a bet on macroeconomic conditions they can't control or predict. Rates in the 1980s and 1990s regularly hit 8-15% for practice acquisitions, and dentists still built successful practices during those periods. Current rates—even when elevated compared to the historically low environment of the 2010s—remain well below the long-term average. More importantly, rates are refinanceable. The practice you buy today at 7.5% can be refinanced at 5% if conditions shift in three years. The equity you didn't build while waiting for that rate drop? That's gone permanently.

The professional development cost is harder to quantify but no less real. Business management skills—hiring, firing, financial planning, marketing, patient communication systems—develop through ownership, not observation. Leadership experience comes from managing a team, not working alongside one. Clinical autonomy expands when you're making treatment decisions without needing to justify them to a practice owner whose risk tolerance or clinical philosophy differs from yours. These capabilities don't emerge from waiting. They emerge from doing.

Where buyers often miscalculate: they treat "feeling ready" as a prerequisite rather than a byproduct. Confidence doesn't arrive before you buy a practice. It develops after you've navigated your first payroll cycle, handled your first difficult employee conversation, and managed your first month where collections dip below projections. Waiting to feel fully prepared means waiting indefinitely, because the skills that generate confidence can only be developed through ownership itself.

The pattern that emerges across buyers who purchased earlier rather than later: very few regret the timing. Most regret not starting sooner. The learning curve feels steep regardless of when you buy—whether that's at 29 or 39—but the financial and professional upside compounds more aggressively when you start earlier. Break-even timelines for practice purchases typically run 3-5 years, meaning a buyer who purchases at 30 is cash-flow positive by 35 and building equity for another 25-30 years. A buyer who waits until 40 doesn't break even until 45, cutting their equity-building window significantly and reducing the compounding effect of ownership income over time.

How to Assess Your Position and Move Forward

Start with the three readiness markers and turn them into questions you can answer with specific numbers. For clinical readiness: pull your production reports from the past 12 months and calculate your average monthly collections. Compare that figure to the practices you're considering—can you sustain 80% of the seller's historical production based on your current output? List the procedures you handle independently versus those you refer out. If you're sending most endo or surgical cases elsewhere, that's a gap worth closing before you buy a practice where those procedures drive significant revenue.

For financial positioning: check your credit score today, not when you're ready to apply for financing. If it sits below 680, you have a concrete action item—pay down revolving balances and avoid opening new credit lines for the next 6-12 months. Calculate your liquid savings and compare it to the $50,000 threshold most lenders expect. If you're short, that's a timeline question, not a capability question. Saving $2,000 monthly gets you there in two years. Review your debt-to-income ratio by adding up all monthly debt payments (student loans, car payments, credit cards) and dividing by your gross monthly income. Most lenders want to see this below 43% after factoring in the practice loan payment, and they typically look for the practice and doctor's personal income to cash flow at a rate of 1.20x—meaning the practice generates $1.20 in revenue for every $1 spent between practice expenses and personal expenses.

Personal circumstances require a different kind of assessment. Write down where you're willing to live for the next five years—specific cities or regions, not vague preferences. If that list has more than three locations, you're probably not geographically committed enough to make ownership work yet. Consider your 3-5 year life plans: are you planning to start a family, relocate for a partner's career, or pursue additional training? None of these disqualify you from ownership, but they affect timing.

Where gaps exist, the fix is usually straightforward. If clinical skills need development, focus on the high-value procedures that drive practice revenue—crown and bridge work, molar endo, surgical extractions. Many buyers spend 6-12 months deliberately building procedural volume in these areas before starting their practice search. If your financial position is weak, the timeline extends but the path is clear: build credit, accumulate savings, and track your production consistently so lenders can see revenue stability. If personal timing feels uncertain, the work is clarifying your 3-5 year commitments rather than waiting for life to settle into perfect alignment.

For buyers who meet the readiness markers, the next steps are operational, not aspirational. Connect with a dental-specific lender and get pre-qualified—this gives you a concrete financing range and identifies any underwriting issues before you're negotiating with a seller. Understanding realistic loan timelines prevents you from losing deals because you underestimated how long funding takes. Assemble your advisory team now: a dental-specific attorney who handles practice transactions, a CPA familiar with practice valuations and tax structuring, and a broker if you're searching in an unfamiliar market. These relationships take time to build, and you don't want to be interviewing attorneys when you've found a practice and need to move quickly.

Start evaluating practices in your target markets, even if you're not ready to make an offer immediately. Reviewing listings builds pattern recognition—you'll start noticing what strong financials look like, which seller claims need verification, and what questions reveal the most about practice health. Many buyers spend 3-6 months observing the market before they find a practice worth pursuing seriously. That window isn't wasted time—it's calibration.

The shift that moves most buyers from waiting to acting: reframing the question from "when will I be ready?" to "what specific gaps do I need to close?" The first question has no answer because readiness feels subjective and infinite. The second question generates a list you can work through systematically. If the gap is procedural confidence, you know what to practice. If it's savings, you know what to accumulate. If it's geographic commitment, you know what decision to make.

One pattern worth recognizing: many buyers who meet all three readiness markers still hesitate, not because they lack capability but because ownership represents a commitment that feels permanent. That hesitation isn't a readiness gap—it's fear of making the wrong choice. The distinction matters. If you're clinically competent, financially positioned, and personally ready but still waiting, you're not preparing—you're avoiding. Most first-time buyers face similar concerns, and the ones who move forward aren't necessarily more confident. They've just accepted that certainty comes from action, not analysis.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- HPI: Younger dentists still become practice owners, just later in ...— adanews.ada.orgIndustry

- Tips for Transitioning to Dental Practice Ownership— panaceafinancial.comIndustry

- Ask the Expert: What are my financial paths to practice ownership?— adanews.ada.orgIndustry

- Delay Dental Practice Purchase Because of High Interest Rates?— engageadvisors.comIndustry

- Buying a Dental Practice: Top Tips for a Successful Dental Practice ...— business.bankofamerica.com

Frequently Asked Questions

Ready to Find Your Ideal Practice?

Whether you're convinced the timing is right or still weighing your options, exploring available practices is the first step toward ownership. Minty's marketplace connects you with vetted dental practices nationwide, while our expert guidance helps you navigate the acquisition process with confidence.