When Your Spouse Isn't On Board With Buying a Dental Practice

Co-Founder, Minty Dental

In Summary

- 73% of married couples experience tension over financial decisions, with major purchases like practice acquisitions triggering the most conflict

- Spousal resistance typically falls into four categories: financial risk concerns, lifestyle impact fears, feeling excluded from planning, or doubts about the buyer's readiness

- Partners often express one concern (like debt) when the underlying issue is different (like feeling left out of decision-making)

- Research shows couples consistently underestimate how productive financial conversations can be, anticipating conflict that rarely materializes when structured properly

- The goal isn't to convince your spouse—it's to identify which specific question hasn't been answered yet and address it directly

Spousal Hesitation Usually Points to Specific, Addressable Concerns

When your spouse pushes back on buying a dental practice, the instinct is to treat it as a relationship problem. It's not. In most cases, resistance signals an unresolved question about risk, lifestyle, or process—not opposition to ownership itself.

Financial decisions are a documented source of marital tension. According to the American Institute of CPAs, 73% of married couples report ongoing strain around money, with disagreements most often triggered by needs versus wants, spending priorities, and major purchases made without discussion. A practice acquisition sits at the intersection of all three.

The stated concern often masks the real one. A partner who fixates on debt levels may actually be worried about being excluded from planning. Someone who questions your readiness might be expressing fear about lifestyle disruption.

Most resistance falls into four patterns. Financial risk concerns center on debt load, cash reserves, and what happens if the practice underperforms. Lifestyle impact fears focus on work-life balance deterioration, loss of flexibility, and the toll of ownership stress. Feeling excluded from decision-making shows up when one partner has been researching, touring practices, and running numbers without involving the other. Doubts about readiness emerge when a spouse questions clinical experience, business acumen, or timing.

One pattern worth noting: couples consistently underestimate how productive financial conversations can be. Research on relationship conflict shows partners anticipate far more tension than actually materializes when discussions are structured with clear agendas and shared information.

The shift that makes these conversations productive is reframing the goal. You're not trying to convince your spouse that buying a practice is the right move. You're trying to surface which specific question hasn't been answered yet—then answer it with data, planning, or outside perspective. The question isn't whether your spouse supports ownership in theory. It's which concrete concern needs to be addressed before they can support this decision, now, with the information currently available.

How to Address Financial Risk Concerns With Data, Not Reassurance

When a spouse expresses fear about debt or financial instability, reassurance rarely resolves anything. What shifts the conversation is replacing abstract promises with concrete numbers that show exactly how the household finances change—and what protections exist if things don't go as planned.

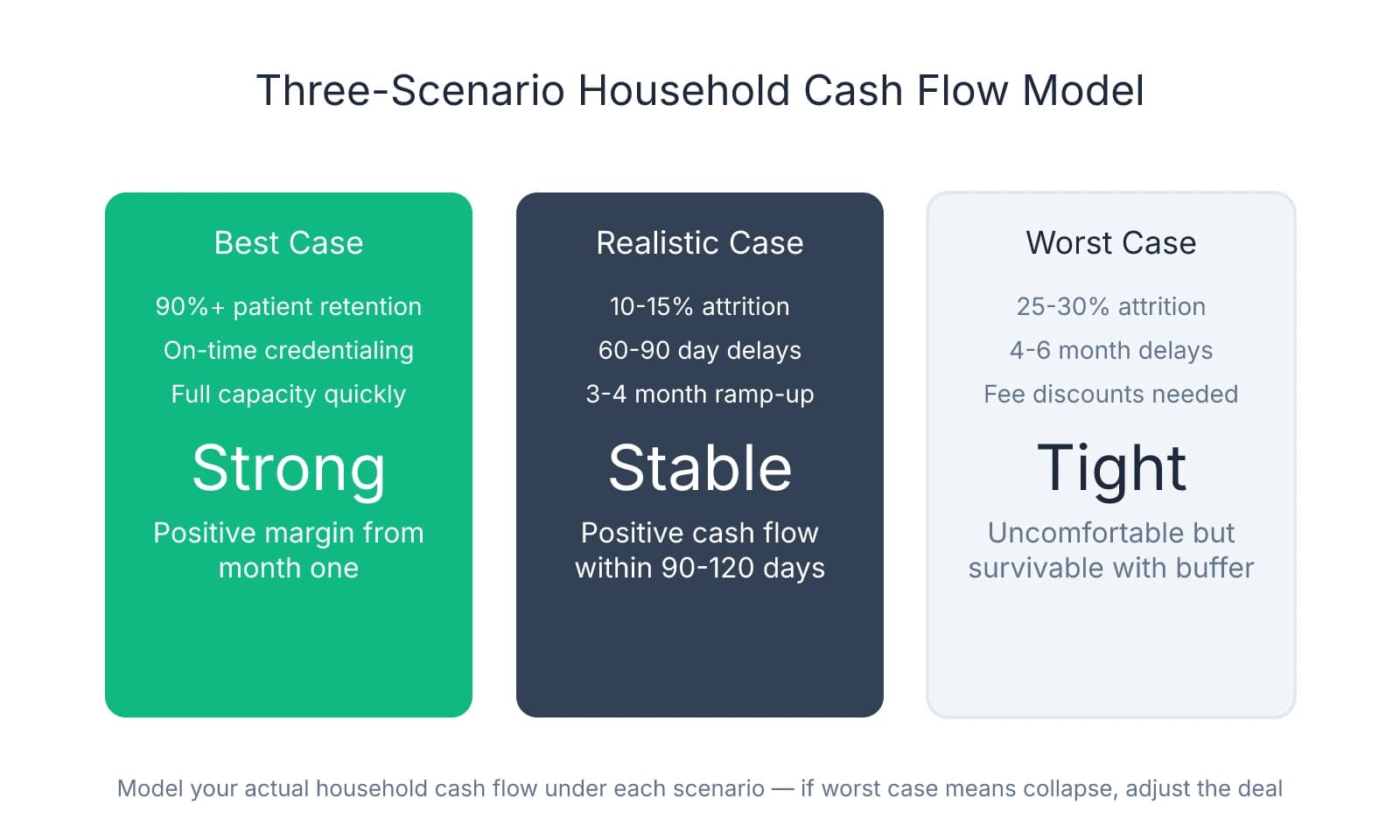

The most effective tool is a three-scenario household model. This isn't practice-level projections—it's your actual monthly household cash flow under best-case, realistic, and worst-case conditions. Start with your current baseline: combined take-home income, fixed expenses, debt payments, and discretionary spending. Then model what happens in each scenario after acquisition.

Best case assumes the practice performs at or above historical levels, you maintain 90%+ patient retention, and collections stay consistent. Calculate your monthly owner draw after loan payments, staff payroll, rent, and supplies. Add back your spouse's income if they work. Subtract your household fixed costs. What's left is your margin—the buffer that funds savings, accelerates student loan payoff, and covers unexpected expenses.

Realistic case assumes 10-15% patient attrition during transition, a 60-90 day credentialing delay with insurance plans, and 3-4 months before you're producing at full capacity. Many buyers find that even the realistic case shows positive household cash flow within 90-120 days, which often surprises a skeptical spouse.

Worst case models significant patient loss (25-30%), extended credentialing delays (4-6 months), and the need to discount fees or offer promotions to stabilize the schedule. This scenario should be uncomfortable but survivable. If worst-case still results in financial collapse, that's a signal the deal structure needs adjustment—more working capital, a smaller acquisition, or a longer associate period to build reserves.

One concern that surfaces repeatedly is student debt. Many spouses see practice loans as "more debt on top of debt" without understanding the income dynamics. Practice ownership typically increases household income by $100,000-150,000 annually compared to associate work within 18-24 months. That delta accelerates student loan payoff rather than delaying it. A $400,000 student loan balance that would take 15 years to eliminate on an associate salary can often be cleared in 7-9 years with owner income—even while servicing practice debt.

The working capital question deserves explicit attention because it's where most spousal anxiety concentrates. Working capital in dental practice loans covers payroll, rent, and supplies during the gap between closing and when insurance reimbursements start flowing. Most lenders structure $75,000-150,000 in working capital as part of the acquisition loan, but buyers often don't explain this protection to their spouse. When a partner understands that payroll is covered even during credentialing delays, the fear of immediate cash flow collapse dissipates.

Present the break-even timeline realistically. Most acquisitions break even in 3-7 years, meaning the cumulative cash invested (down payment, working capital, transaction costs) is recovered through owner draws that exceed what you would have earned as an associate. Promising immediate returns or claiming you'll be "making more from day one" erodes trust when the first few months are tight. A spouse who expects a 5-year payback and sees it happen in 4 years feels validated. One who expects immediate returns and faces 90 days of financial stress feels misled.

Where financial conversations stall is when they stay between the two of you. One step many buyers find valuable is involving a third party—a financial adviser, CPA, or dental-specific consultant who can validate the numbers and answer questions without the emotional weight of a marital conversation. A spouse who hears "this deal structure is conservative" from a neutral expert often accepts it more readily than the same statement from their partner.

Addressing Lifestyle and Work-Life Balance Fears

The fear that ownership means losing your partner to 70-hour weeks and perpetual stress is legitimate—and dismissing it as unfounded creates exactly the resentment you're trying to avoid. The first 90 days after closing are legitimately demanding. Pretending otherwise sets false expectations that erode trust when reality hits.

What actually happens in those first three months: you're learning a new patient base, navigating staff dynamics, troubleshooting systems the seller never documented, and handling the inevitable surprises that surface post-transition. The first 90 days after closing typically require 50-60 hour weeks—not because you're inefficient, but because you're building relationships, establishing credibility, and stabilizing operations simultaneously. A spouse who expects normal hours during this period will feel abandoned. One who knows the timeline and sees progress toward the other side stays engaged.

Many buyers frame ownership as universally more demanding than associate work. The data doesn't support that. Burnout affects roughly 40% of dentists, but the drivers differ significantly between associates and owners. High-volume associateships—where you're producing $80,000-100,000 monthly to hit production bonuses—often generate more sustained stress than ownership with proper systems. The difference is control. As an owner, you set the schedule, choose the patient mix, and decide when to block time off.

Many successful owners work 3-4 clinical days per week within 2-3 years of acquisition. That flexibility doesn't happen automatically—it requires intentional planning from day one. The path there starts with defining non-negotiable family commitments before you close, not after you're overwhelmed.

One framework that works: identify 3-5 specific, recurring commitments that matter most to your household. These might include Tuesday/Thursday dinners at home, no clinical work on Saturdays, being present for kids' bedtime routine, or protecting two weeks of vacation annually. Write them down. Share them with your practice manager during the transition planning phase. When you're building the schedule for your first 90 days, those anchors stay fixed—everything else flexes around them.

The mental load of ownership deserves explicit discussion because it's the part that comes home even when you're physically present. An associate clocks out and leaves work behind. An owner fields staff texts about supply orders, thinks through next quarter's marketing strategy during dinner, and wakes up at 3 a.m. worrying about a patient who left a negative review. Naming this reality upfront—and planning for how to manage it together—prevents the slow erosion of presence that many spouses describe.

Some strategies that help: designate a specific time each week (Sunday evening, Wednesday after the kids are in bed) to discuss practice issues, so they're contained rather than surfacing randomly. Use a shared calendar that shows both clinical days and administrative blocks, so your spouse knows when you're genuinely unavailable versus when you're choosing to work. Commit to a weekly check-in where you ask your partner how they're experiencing the transition—not just how the practice is performing.

Staff retention during ownership transition directly impacts your workload in those early months. When key team members leave, you're not just replacing skills—you're absorbing their responsibilities until replacements are trained. Protecting staff stability protects your time, which protects your family commitments.

The conversation with your spouse should include what support looks like during the intense early phase. This might mean your partner handles more of the household logistics for 90 days, or it might mean hiring help—a house cleaner, meal delivery service, or childcare coverage—to reduce the non-practice load on both of you. A $400/month house cleaning service that preserves your Saturday mornings together is a rounding error in a practice budget.

Where lifestyle fears often resolve is when the buyer demonstrates that ownership can provide more flexibility than associate work—but only with intentional planning. A spouse who sees you actively working toward that balance, rather than just promising it will happen eventually, gains confidence that the sacrifice is temporary, not permanent.

Creating Shared Ownership of the Decision

The shift from "your practice decision" to "our practice decision" doesn't happen through a single conversation—it happens through a series of structured touchpoints where your spouse feels genuinely included in the process, not just informed after decisions are made. Many buyers involve their partner by presenting conclusions: "I found a great practice," "The numbers look solid," "I think we should move forward." That's reporting, not collaborating. Real inclusion means your spouse has input at decision points, not just visibility into outcomes.

One pattern that consistently improves outcomes: scheduled financial conversations rather than reactive ones. Research on couples and financial communication shows that partners who set regular times to discuss money report significantly less conflict and better alignment than those who only talk about finances when a bill arrives or a decision looms. For practice acquisition, this might look like a standing Sunday evening check-in where you review the week's progress, upcoming decisions, and any concerns either of you have surfaced.

The structure of these conversations matters as much as the frequency. Start each session by reviewing what's already been decided and what's still open. Then identify the next decision point and establish explicit veto power for both partners. This isn't symbolic—it means either of you can stop the process if a fundamental concern remains unaddressed. Many spouses describe their anxiety not as fear of the practice itself, but fear of being swept along in a process they can't control.

Before you tour a single practice, define success together. What household income would make ownership "worth it" for both of you? What work schedule protects the family commitments that matter most? What lifestyle outcomes—paying off student loans faster, funding kids' college, taking real vacations—would validate the risk? These aren't aspirational goals to revisit later; they're the criteria you use to evaluate whether a specific opportunity aligns with your household priorities.

Involve your spouse in major milestones without requiring them to analyze every financial detail. Most partners don't want to review three years of P&L statements or compare hygiene production across practices—but they do want to meet the seller, tour the physical space, and understand why this practice rather than another. These moments give your spouse a tangible sense of what you're buying into and create shared memory around the decision.

One decision point that deserves explicit discussion: reviewing the letter of intent together before you sign. The LOI locks in purchase price, deal structure, transition terms, and contingencies—the framework for everything that follows. This is the moment to surface any remaining concerns, because once you're in due diligence, momentum builds quickly.

What happens when you've addressed every specific concern—financial modeling, lifestyle planning, transition support—and your spouse still isn't supportive? That outcome signals something deeper than practice ownership. It might reflect fundamental differences in risk tolerance, where one partner is wired to pursue opportunity and the other to protect stability. It might point to misalignment about life priorities, where ownership competes with other goals like relocating, starting a family, or pursuing a different career path. Or it might indicate timing issues, where your spouse isn't opposed to ownership but believes now isn't the right moment.

These deeper misalignments don't resolve through better spreadsheets or more reassurance. They require honest conversation about whether this decision fits your relationship's trajectory or whether proceeding would create lasting resentment. Some buyers move forward despite spousal hesitation and build successful practices—but those outcomes typically involve explicit acknowledgment that one partner is taking on more risk and responsibility, with clear agreements about how that imbalance gets addressed.

The strongest acquisitions happen when both partners feel invested in the outcome, even when only one is clinically involved. Investment doesn't mean equal enthusiasm—it means shared understanding of the risks, aligned expectations about the path forward, and confidence that concerns are being managed rather than dismissed. A spouse who feels heard, included in key decisions, and equipped with realistic timelines becomes an advocate rather than an obstacle. That shift doesn't happen by accident. It happens when you treat the decision as genuinely joint from the beginning, with structured conversations, explicit veto power, and a clear definition of what success looks like for your household—not just your career.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Financial decisions are a documented source of marital tension— aicpa.org

- When couples fight about money, what do they fight about? - PMC— pmc.ncbi.nlm.nih.govGovernment

- Demystifying the Practice Loan Process | American Dental Association— ada.orgIndustry

- Balancing act: Young owners share how they juggle being a boss ...— adanews.ada.orgIndustry

- [PDF] Couples Underestimate the Benefits of Talking About Money - CEPR— cepr.orgIndustry

Frequently Asked Questions

Ready to navigate practice ownership together?

Buying a dental practice is a major decision that affects your whole family. Minty Plus provides expert guidance through every step of acquisition, helping you and your spouse understand the financial and operational realities before committing.