Bank Appraisal Came in Lower Than Dental Practice Asking Price

Co-Founder, Minty Dental

In Summary

- When a bank appraisal comes in below the agreed purchase price, your lender will only finance up to the appraised value—not the amount you offered to pay

- The appraisal gap is the difference between what you agreed to pay and what the bank says the practice is worth, and you must cover that gap with cash or renegotiate

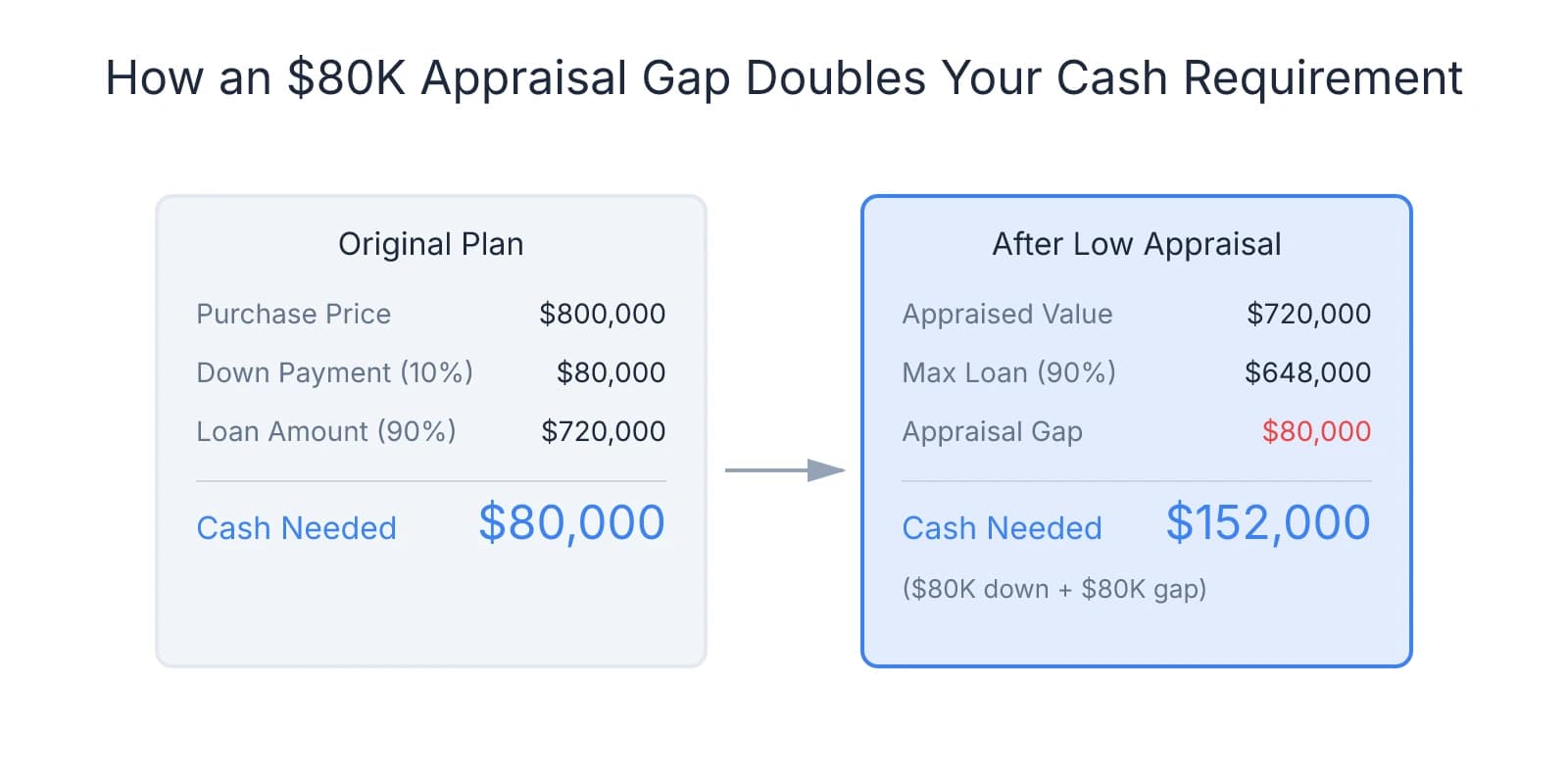

- On an $800K purchase with a $720K appraisal, you face an $80K gap that changes your down payment from $80K to $160K (assuming 10% down)

- You have four options: renegotiate the price, cover the gap with cash, challenge the appraisal, or walk away using your financing contingency

A Low Appraisal Means Your Lender Won't Finance the Full Purchase Price

An appraisal gap occurs when the bank's professional valuation of a dental practice comes in below the purchase price you agreed to pay. The gap is the dollar difference between these two numbers, and it creates an immediate financing problem: your lender will only approve a loan up to the appraised value, leaving you to cover the shortfall or renegotiate the deal.

Lenders use appraisals to protect against lending more than the collateral is worth. Appraisers follow strict valuation rules, and lenders cannot interfere with their professional judgment—the appraised value stands as the ceiling for your loan amount, regardless of what you offered.

Here's how the math works. You agree to buy a practice for $800,000 with 10% down. You expect to put down $80,000 and finance $720,000. The bank appraisal comes back at $720,000—an $80,000 gap. Now the lender will only approve a $648,000 loan (90% of $720,000). You need $152,000 in cash at closing: the original $80,000 down payment plus the $80,000 gap. Your cash requirement just doubled.

This rule applies across lender types. SBA lenders, conventional banks, and specialty dental practice lenders all cap financing at appraised value. The American Dental Association notes that lenders evaluate practice history, patient volume, and financial performance when structuring loans—but the appraisal sets the hard limit on how much they'll lend.

The gap doesn't mean the deal is dead. It means you're navigating a pricing misalignment between what the seller wants and what the market supports. If you're already concerned about securing financing with existing student debt, a low appraisal compounds that pressure. But the appraisal gap is a negotiation reset, not a rejection.

Why Bank Appraisals Come in Below Asking Price

A low appraisal usually means the seller's asking price wasn't anchored to the methodology lenders require. Bank appraisers follow conservative, income-focused frameworks that often yield lower values than the market-based comparisons sellers use when setting their price.

Income-based methodology compresses values through conservative assumptions. Most bank appraisers use the income approach, which calculates value by capitalizing the practice's net cash flow. They start with annual collections, subtract overhead expenses and a standard doctor compensation rate (typically 30% of production), then apply a capitalization rate—usually between 20-35%—to the remaining cash flow. This income approach examines the monetary benefit of ownership rather than what similar practices sold for.

If the appraiser assumes higher overhead percentages or applies a 35% cap rate instead of 25%, the final value drops significantly. A practice generating $100,000 in net cash flow might appraise at $400,000 with a 25% cap rate, but only $286,000 at 35%. Sellers rarely account for this variability when pricing their practice—they look at what neighboring practices sold for and assume the same multiple applies.

Recent comparable sales may not support the asking price. The market approach compares the subject practice to recent sales of similar practices in the area. When appraisers can't find enough comparable transactions—or when the comps that do exist sold for less than the seller's asking price—the appraisal comes in low. Professional valuations establish a baseline, but the practice is worth whatever a buyer will actually pay.

This happens frequently when sellers list during a hot market and anchor their price to optimistic projections rather than closed transactions. A seller who bought their practice at 75% of collections in 2019 may assume they can sell at 80% in 2024—but if recent sales in the region show practices closing at 65-70%, the appraisal won't support the higher multiple.

Practice-specific risk factors reduce bankability even when collections look strong. Appraisers adjust values downward when they identify characteristics that increase operational risk or limit transferability. High PPO participation rates compress profit margins and reduce the practice's ability to generate cash flow under new ownership. Fee-for-service practices typically appraise higher because they offer more pricing control and better margins.

Aging equipment, outdated technology, or deferred maintenance also lower appraised value. If the buyer will need to invest $75,000-$100,000 in equipment upgrades within the first year, the appraiser factors that capital requirement into the valuation. Revenue concentration creates similar risk—when one hygienist generates 40% of production or a handful of patients account for a disproportionate share of collections, the appraiser sees key person risk and adjusts accordingly.

Your Four Options When the Appraisal Comes in Low

When the appraisal lands below your agreed purchase price, you're navigating a decision tree with four branches. Your choice depends on three variables: how much liquidity you have available, how much leverage the appraisal gives you with the seller, and whether you believe the appraised value accurately reflects the practice's market position.

Renegotiate the purchase price to match the appraisal

This is the most common resolution—the appraisal gives you objective third-party evidence that the asking price exceeded what the market supports. Many buyers hesitate to push back on price after signing an LOI, assuming the seller will view it as bad faith negotiation. In practice, sellers understand that bank appraisals carry weight.

Frame the conversation around the appraisal's findings rather than your financing constraints. Instead of "I can't afford the gap," try "The bank appraisal came in at $720K, and the report shows recent comparable sales averaging 68% of collections rather than the 75% we used in our original pricing." This shifts the discussion from your cash position to market reality.

One pattern worth paying attention to: sellers who resist repricing often reveal something about their urgency or flexibility. If the seller immediately agrees to match the appraised value, they likely priced optimistically and expected negotiation. If they dig in and refuse to budge, you're either dealing with someone who has other interested buyers or someone anchored to an unrealistic number.

Cover the appraisal gap with additional cash

If you have the liquidity and strong conviction in the practice's upside, paying the gap keeps the deal on track without renegotiation. This makes sense when the appraisal reflects conservative assumptions you believe undervalue the practice—for example, if the appraiser used a 35% cap rate in a market where recent sales suggest 28% is more accurate.

The tradeoff is straightforward: you're increasing your total out-of-pocket investment, which reduces the cash reserves you'll have available during the first 6-12 months of ownership. On an $80K gap, you're not just adding $80K to your down payment—you're also reducing the buffer you'd planned to use for working capital, unexpected repairs, or staff retention bonuses. Many first-time buyers underestimate how much cash they'll need in the first year.

Where this option makes sense: you've already built strong conviction through due diligence, the practice has clear growth levers you can pull in year one, and you have enough reserves beyond the gap to operate comfortably for six months without drawing a full salary.

Request a reconsideration of value to challenge the appraisal

Filing a reconsideration of value (ROV) through your lender gives you a structured path to contest the appraisal when you believe it contains factual errors or missed relevant market data. The ROV process allows borrowers to submit supporting documentation and ask the appraiser to review specific concerns—but it's not a negotiation tool.

The most effective ROV requests focus on verifiable gaps in the appraisal report: incorrect square footage, missing equipment that affects value, or comparable sales the appraiser overlooked. If three practices within five miles sold in the past 18 months at higher multiples than the comps used in your appraisal, that's actionable data.

What doesn't work: arguing that your $40K buildout should add $40K to the appraised value, or claiming the practice "feels" worth more based on patient loyalty. Federal guidance on ROV procedures emphasizes that reconsiderations must be based on objective evidence, not subjective disagreement with methodology.

The timeline matters—an ROV typically adds 5-10 days to your closing schedule while the appraiser reviews your submission and either revises the report or explains why the original value stands.

Walk away using your financing contingency

Most LOIs and purchase agreements include a financing contingency that protects you if the appraisal kills your ability to secure a loan. If the appraisal comes in low enough that you can't cover the gap and the seller won't renegotiate, you can typically exit the deal and recover your deposit without penalty.

Where buyers get stuck is treating the financing contingency as a last resort rather than a legitimate option. If the appraisal revealed structural issues you missed in due diligence—high overhead that won't support the debt service, aging equipment that requires immediate capital investment, or revenue concentration that creates key person risk—walking away may be the right call even if you could technically cover the gap.

One decision framework that helps: calculate what your debt service coverage ratio would be at the appraised value versus the asking price. If the appraisal drops your projected DSCR from 1.4x to 1.1x, you're entering ownership with much thinner margins for error.

How to Decide Whether to Move Forward or Walk Away

The appraisal gap forces a decision most buyers aren't prepared for: do you adjust your terms and move forward, or do you walk away and start over? The answer depends less on whether you can technically afford to cover the gap and more on whether the practice still meets your financial goals at the appraised value.

Start by recalculating your debt service coverage ratio at the appraised value. If you were planning to finance $720K at the original purchase price, you're now financing $648K (90% of the $720K appraisal). That lower loan amount reduces your monthly debt service, which improves your coverage ratio—but only if you're not draining your working capital to cover the gap. Run the numbers both ways: if you renegotiate the price down to $720K, your debt service drops and your cash position stays intact. If you cover the $80K gap with savings, your debt service stays the same but your liquidity buffer shrinks significantly.

The threshold that matters is whether your DSCR stays above 1.25x after accounting for realistic overhead and a market-rate doctor salary. Walk through the appraisal report with your accountant or advisor and verify that the cash flow projections align with what you observed during due diligence. If they don't, the appraisal may be overly conservative—but if they do, the practice won't support the debt load you were planning to take on.

Evaluate whether covering the gap leaves you with adequate working capital for the first 6-12 months. A pattern many first-time buyers miss: the appraisal gap doesn't just increase your down payment—it reduces the cash reserves you'll need when the HVAC system fails in month three or when you need to offer retention bonuses to keep key staff.

The rule of thumb worth paying attention to: plan for 3-6 months of operating expenses in accessible cash after closing. If your monthly overhead runs $55K, that's $165K-$330K in reserves—and that's before accounting for equipment repairs, staff turnover, or the revenue dip that often happens during ownership transition. If covering the gap pushes you below that threshold, you're increasing your risk significantly.

Treat the appraisal as a data point that protects you from overpaying, not an obstacle to overcome. The appraiser has no incentive to lowball the value—they're following standardized methodology and analyzing comparable sales data you didn't have access to when you made your offer. If the appraisal came in 10% below asking price and the seller won't budge, that's not the appraiser being conservative—it's the seller being anchored to an unrealistic number.

One question that clarifies the decision: if you were evaluating this practice for the first time today and the asking price was the appraised value, would you still make an offer? If the answer is yes, the deal makes sense at the lower price and you should push for renegotiation. If the answer is no—if the practice only looked attractive at the higher valuation because you were modeling aggressive growth or optimistic overhead assumptions—the appraisal just saved you from overpaying.

If the seller won't renegotiate and the appraisal feels defensible, walking away may be the right move. The financing contingency exists specifically for this scenario: when the bank's valuation reveals a pricing misalignment that kills the deal economics. Many buyers hesitate to walk away because they've already invested time, due diligence costs, and emotional energy into the transaction. That's sunk cost thinking—the question isn't whether you've already invested in this deal, it's whether moving forward at the revised terms still makes financial sense.

If you do walk away, you're not starting from zero. You've learned what due diligence looks like, you've built relationships with lenders and advisors, and you've clarified what financial metrics matter most. Other practices will come along, and the next one may appraise at or above asking price because the seller priced it more conservatively from the start.

Your next steps depend on where you land in this decision tree. If you're leaning toward renegotiation, talk to your lender first—confirm that the appraised value is final and ask whether they see any path to additional financing if the seller meets you halfway. If you're considering covering the gap, review the appraisal report with your accountant and model out your first-year cash flow with the reduced liquidity buffer. If you're thinking about walking away, verify your contingency deadline and make sure you understand what documentation you need to provide to exit cleanly.

The appraisal gap is a negotiation reset, not a failure. When the appraisal comes in low, you're learning something important about the market's view of this practice—and that information is worth acting on, even if it means walking away from a deal you thought was done.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- My appraisal is less than the sale price. What does that mean for me?— consumerfinance.govGovernment

- Demystifying the Practice Loan Process | American Dental Association— www.ada.orgIndustry

- The Dental Practice Appraisal – A Powerful Tool in the Transition ...— dentaltransitions.comIndustry

- What Went Wrong: We Disagreed on the Value of the Practice— www.ada.orgIndustry

- Reconsideration of Value: How to Dispute an Appraisal— www.classvaluation.com

- Interagency Guidance on Reconsiderations of Value of Residential ...— www.federalreserve.govGovernment

- Appraisal came in lower than offer : r/FirstTimeHomeBuyer - Reddit— www.reddit.com

Frequently Asked Questions

Navigate appraisal gaps with expert guidance

When a bank appraisal falls short of your offer, you need experienced advisors who understand dental practice valuations. Minty Plus provides hands-on support to help you bridge gaps and close your practice acquisition successfully.