Fee-for-Service vs PPO Dental Practice: Which Is Worth More?

Co-Founder, Minty Dental

In Summary

- Dental practice valuation has shifted from collections multiples to EBITDA multiples (typically 4-7x for strong practices), making profitability the primary driver of value

- PPO write-offs of 30-45% directly compress EBITDA even when production looks strong—a fee-for-service practice collecting 95% of production generates significantly more EBITDA than a PPO-heavy practice collecting 70% of the same production figure

- Buyers inherit the seller's PPO contracts and reimbursement rates at closing, which aren't easily renegotiated and represent baked-in structural risk affecting debt service capacity from day one

- Two practices producing $1M annually can have valuations differing by hundreds of thousands of dollars based solely on insurance mix and collection efficiency

Fee-for-Service Practices Command Higher Valuations Because Collections Drive EBITDA

When evaluating a practice listing, the production number catches your eye first. But that figure tells you almost nothing about actual worth.

The market has moved decisively toward EBITDA-based valuation, with strong practices commanding 4-7x EBITDA. This fundamentally reframes what you're buying: not production potential, but actual profitability.

PPO write-offs sit at the center of this calculation. Practices participating in PPO networks typically write off 30-45% of production, which means a practice producing $1M might only collect $650,000-$700,000. A fee-for-service practice producing the same $1M collects $950,000 or more. That $250,000-$300,000 gap compresses EBITDA directly, lowering the practice's valuation by a multiple of that difference.

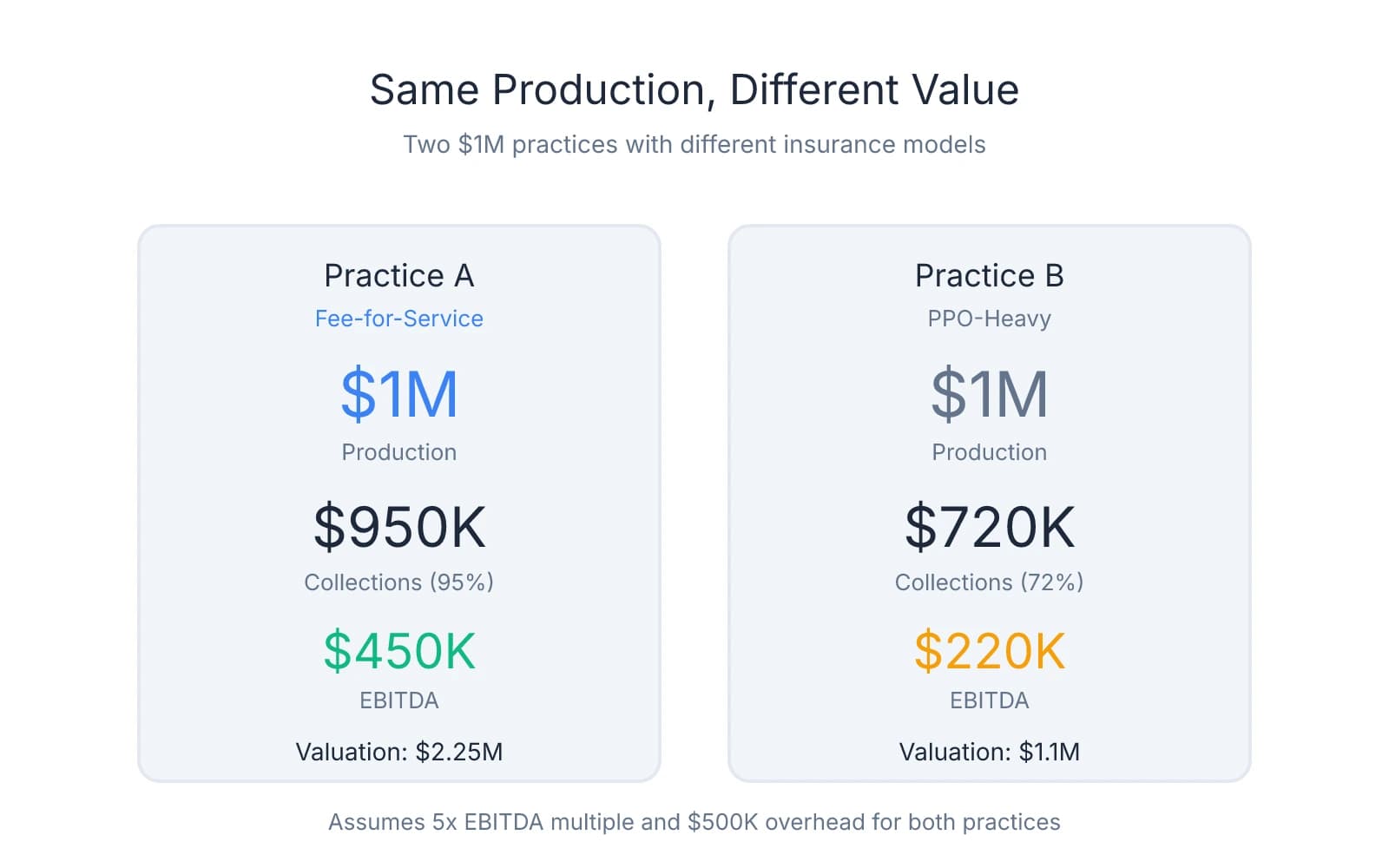

Consider two practices, both producing $1M annually. Practice A operates fee-for-service and collects 95%. Practice B participates heavily in PPO networks and collects 72% after write-offs. Practice A deposits $950,000; Practice B deposits $720,000. Assuming similar overhead, Practice A generates significantly higher EBITDA. At a 5x EBITDA multiple, that collection gap translates to over $1M in valuation difference—not because one practice is busier, but because one converts production to profit more efficiently.

The pressure on PPO-heavy practices has intensified as overhead costs have climbed. Labor, supplies, and occupancy expenses have risen 15-20% in many markets over recent years, while PPO reimbursement rates have remained flat or declined in real terms. This creates a profit squeeze where certain procedures approach zero or negative margins after accounting for true delivery costs.

One pattern worth noting: buyers—especially DSOs and private equity-backed groups—scrutinize payer mix closely during due diligence. A practice with optimized PPO contracts or high fee-for-service percentage signals stability and scalability. A practice with low reimbursement rates and high write-offs raises questions about sustainability, particularly if the buyer plans to maintain or expand operations.

What catches many first-time buyers off guard is that you inherit the seller's PPO contracts at closing. Those reimbursement rates, fee schedules, and write-off percentages transfer with the practice. Renegotiating contracts post-acquisition is possible but neither quick nor guaranteed—and in the meantime, you're operating under the same financial constraints the seller faced, which affects your debt service capacity from day one.

The question isn't whether fee-for-service practices are "better" ideologically. The question is whether the practice generates enough profit to support the debt you'll carry and the income you need. Production figures don't answer that. Collection rates and EBITDA do.

How PPO Write-Offs Affect Your Ability to Service Acquisition Debt

The valuation question matters, but the cash flow question determines whether you can actually afford the practice. Lenders care whether it generates enough cash to cover loan payments, practice expenses, and personal income with margin to spare.

Most lenders require a debt service coverage ratio of 1.2x, meaning the practice must generate $1.20 in cash flow for every $1 in combined expenses. PPO write-offs reduce available cash to meet this threshold, which means a practice that looks profitable on paper can fail the lender's test—or worse, pass but leave you unable to meet income goals.

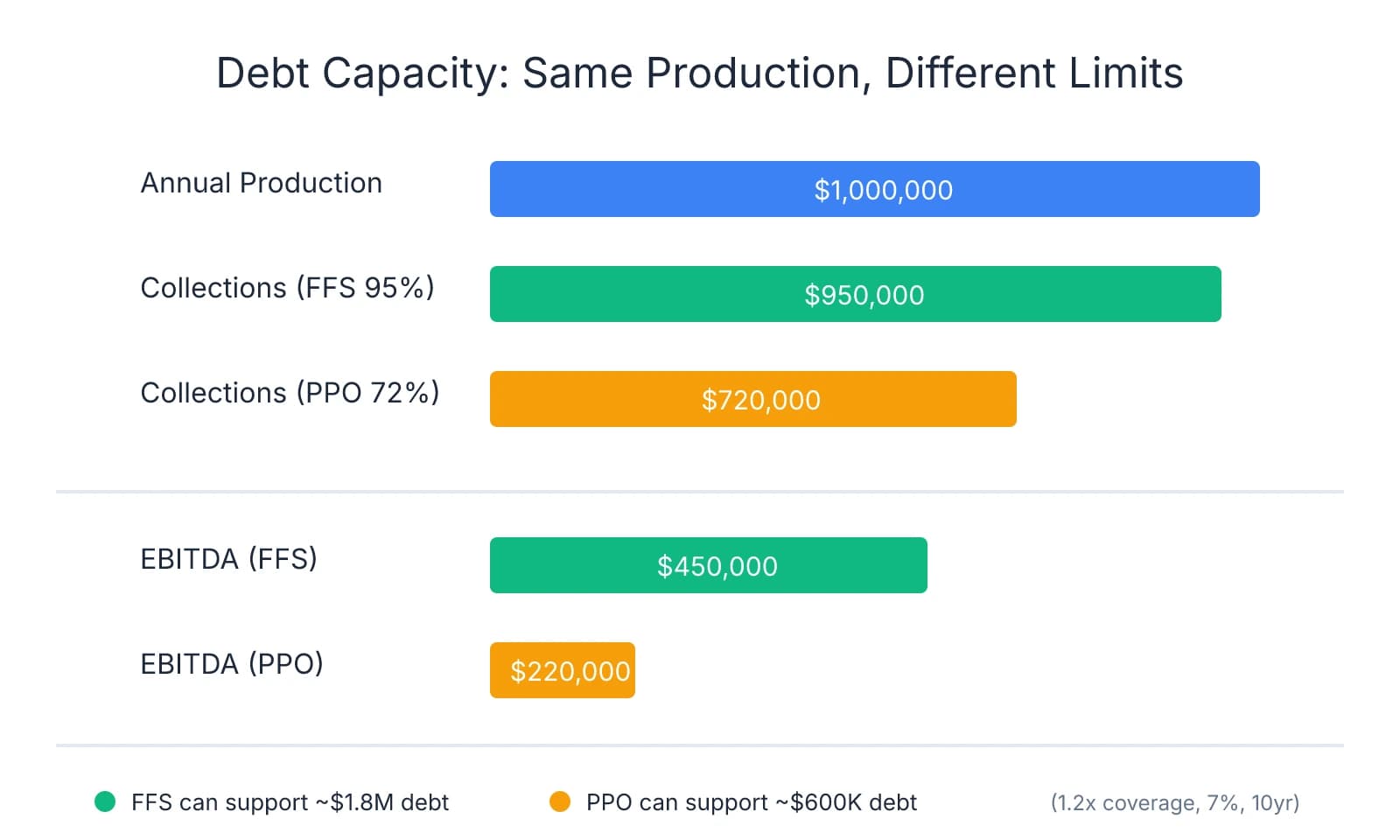

Walk through a comparison. Practice A produces $1M annually and operates fee-for-service, collecting 95%. Practice B produces the same $1M but writes off 35%, collecting 65%. Practice A deposits $950,000. Practice B deposits $650,000. That $300,000 collection gap determines how much debt the practice can support.

Assume both carry similar overhead: $500,000 annually for staff, supplies, rent, and operating expenses. Practice A generates $450,000 in EBITDA. Practice B generates $150,000. Financing an acquisition at 7% interest over 10 years, Practice A can support roughly $1.8M in debt while maintaining 1.2x coverage. Practice B can support around $600,000. Same production, vastly different debt capacity.

The second-order effect is harder to see but equally consequential. PPO-heavy practices often require higher patient volume to generate the same profitability as fee-for-service practices. You're seeing more patients, working longer hours, and managing more administrative complexity—claims, denials, bundling disputes—to collect less per procedure.

One protection many buyers overlook is calculating actual collections—not production—when modeling affordability. Pull three years of deposit records, not just P&L statements. Verify what percentage of billed production actually cleared the bank. If the practice shows $1M in production but only $700,000 in collections, build your debt service calculation on $700,000, not $1M. Production is a marketing number. Collections are what you deposit.

Where buyers get burned is assuming they can improve collections post-acquisition without understanding what's driving the write-offs. If the practice participates in low-reimbursement PPO contracts, those rates transfer with the practice. Renegotiating takes time—often 12-18 months if contracts allow it at all. In the meantime, you're operating under the same constraints the seller faced.

Fee-for-service practices typically offer better debt service coverage with less clinical volume. You're collecting more per procedure, generating the same EBITDA with fewer patient visits. That translates to more predictable cash flow, lower administrative overhead, and better capacity to absorb unexpected expenses without jeopardizing loan payments.

If evaluating a PPO-heavy practice, calculate whether collections support your financial obligations under the current payer mix. Don't assume you'll transition to fee-for-service immediately—that process takes time and carries patient attrition risk. Model the practice as it exists today. If the numbers don't work under those conditions, the practice isn't affordable, regardless of how busy it looks.

Due Diligence Questions That Reveal Whether the Insurance Mix Is Sustainable

Not every PPO practice is a bad investment, and not every fee-for-service practice is low-risk. What matters is whether the specific payer mix matches the market, whether contracts are structured favorably, and whether the patient base will remain stable under new ownership.

Start by requesting a breakdown of collections by payer type. You need to see what percentage of revenue comes from fee-for-service patients, PPO plans, Medicaid, and cash-pay. Many sellers present production figures without clarifying how much actually converts to deposited cash. Ask for a report showing collections by insurance carrier, average write-off percentage per plan, and patient count under each contract. This reveals which plans drive revenue and which compress margins.

One red flag that surfaces repeatedly: total PPO write-offs exceeding 35% of production. Practices writing off more than 35% face significant profit compression, especially as overhead costs rise. If write-offs sit at 40-45%, the practice likely operates on thin margins, and any expense increase—staff raises, supply costs, rent adjustments—can push profitability negative. The second red flag is heavy dependence on a single low-reimbursing carrier. If 40% of collections come from one PPO plan paying 50 cents on the dollar, you're inheriting concentration risk.

Ask when PPO fee schedules were last renegotiated and whether reimbursement rates have kept pace with overhead inflation. Many practices signed contracts years ago and never revisited them. Insurance reimbursement has stagnated while labor and supply costs have climbed 15-20% in many markets. If the seller hasn't renegotiated in five years, you're likely inheriting outdated fee schedules that no longer support current operating costs. Request copies of actual contracts—not summaries—and verify reimbursement rates for the top 10 procedures by volume.

The insurance mix should align with local market demographics. Fee-for-service practices perform better in affluent areas where patients have disposable income and value continuity of care over in-network discounts. A fee-for-service practice in a middle-income suburb where most employers offer PPO dental plans faces higher patient attrition risk. Check whether the practice's payer mix reflects the market's insurance penetration or whether it's misaligned with local patient expectations.

Patient attrition determines whether a payer mix is sustainable through ownership transition. Fee-for-service practices typically see 5-10% patient attrition when ownership changes, mostly patients loyal to the retiring dentist. PPO practices transitioning to fee-for-service post-acquisition face higher attrition—often 15-25%—because you're asking patients to pay more for the same care they previously received at in-network rates. If planning to shift a PPO practice toward fee-for-service, model the financial impact of losing 20% of the patient base and calculate whether remaining patients generate enough revenue to cover debt service.

One pattern worth attention: practices that have been gradually reducing PPO participation over the past 2-3 years. This can signal strategic positioning—the seller has been conditioning patients to accept fee-for-service pricing. But it can also signal patient loss. Request active patient counts by year and compare them to the reduction in PPO participation. If the practice dropped three PPO plans and lost 200 active patients in the same period, the transition didn't go smoothly.

Ask whether the practice has a membership plan or in-house discount program for uninsured patients. Practices with these structures often retain patients more effectively when transitioning away from PPO contracts, offering an alternative to insurance that still provides predictable pricing. If the practice relies entirely on PPO participation with no alternative for uninsured patients, you're inheriting a patient base conditioned to expect insurance coverage—and less likely to stay when you shift toward fee-for-service.

Matching the Practice's Insurance Model to Your Financial Goals and Clinical Style

The insurance model you inherit shapes more than cash flow—it defines your daily clinical experience, your relationship with patients, and whether the practice supports your financial plan from day one. The right choice depends on your debt load, income requirements, clinical preferences, and whether you're willing to invest time reshaping the practice's payer mix after closing.

Fee-for-service practices: Higher per-patient revenue and better profit margins, but they require strong case acceptance skills and effective patient communication. You're asking patients to pay full fees without insurance subsidies, which means treatment conversations focus on value, outcomes, and trust rather than coverage limitations. But it requires confidence in presenting treatment plans and tolerance for a longer ramp-up period as you build credibility with the patient base. If you're carrying significant acquisition debt and need immediate cash flow, a fee-for-service practice can feel financially tight in the first 6-12 months.

PPO practices: Predictable patient volume and lower marketing costs, since in-network status drives referrals through employer benefit plans. Patients arrive pre-qualified by insurance, reducing friction in scheduling and case acceptance. But the trade-off is efficiency pressure. You're seeing more patients to generate the same profitability a fee-for-service practice achieves with fewer appointments. PPO practices often operate on thinner margins per patient visit, which means your schedule needs to stay full and your team needs to move quickly.

Hybrid models offer a middle path. Practices that maintain selective PPO participation—typically 2-3 high-reimbursing plans—while operating fee-for-service for the rest of the patient base combine volume stability with better margins. You're not writing off 40% of production, but you're also not starting from zero when building a fee-for-service patient base. The key is evaluating which PPO plans the practice participates in and whether their reimbursement rates justify the write-offs. A plan paying 75-80% of your fee schedule is a different proposition than one paying 50-60%.

One decision that surfaces early: whether you're willing to transition the practice's payer mix post-acquisition. Shifting a PPO practice toward fee-for-service requires patient communication, tolerance for attrition, and time—often 12-24 months to complete without destabilizing cash flow. If you're not prepared for that process, buy a practice that already operates under the model you want.

Model your first-year cash flow using actual collections, not production. Pull the practice's deposit records and calculate what percentage of billed production clears the bank each month. If the practice collects 70% of production after PPO write-offs, build your budget on that figure—not the headline production number. Then calculate whether those collections cover your debt service, operating expenses, and personal income with enough margin to absorb unexpected costs.

Your clinical style matters more than most buyers acknowledge upfront. If you value autonomy, longer appointments, and comprehensive care, a fee-for-service practice aligns better with how you want to practice. If you're efficient, comfortable with volume, and prefer predictable patient flow over case acceptance conversations, a well-structured PPO practice can work. The mismatch happens when buyers acquire a practice that conflicts with their clinical preferences and then spend years trying to reshape it.

Before you close, verify that the insurance mix supports your financial obligations under current conditions. Don't assume you'll transition to fee-for-service immediately or renegotiate PPO contracts within six months. If the practice can't support your debt service and income goals as it exists today, it's not the right acquisition—regardless of how much potential you see. The practice you buy should work financially from day one, with any payer mix changes treated as upside, not a requirement for survival.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- How PPO Contracts Influence Your Dental Practice's Valuation— pponegotiationsolutions.comIndustry

- [PDF] Dental PPO Collection Loss Analysis— cdr.lib.unc.eduAcademic

- Buying a Dental Practice: Top Tips for a Successful Dental Practice ...— business.bankofamerica.comIndustry

- What Buyers Must Review Before Acquiring a Practice— pponegotiationsolutions.comIndustry

Frequently Asked Questions

Find Your Ideal Practice Model Today

Whether you're drawn to fee-for-service independence or PPO stability, the right practice acquisition depends on your goals and market. Explore available practices that match your preferred model and get expert guidance on maximizing your investment.