Dental Practice Seller Financing Terms: What's Normal for Buyers

Co-Founder, Minty Dental

In Summary

- Most seller notes represent 10-20% of the purchase price, with banks covering 75-85% and buyers providing 10-15% down payment

- Subordination means the seller gets paid only after the bank loan is current—if you default on the bank loan, seller note payments stop immediately

- SBA loans require a standby agreement (SBA Form 155) that formalizes subordination and prevents seller payments during any bank default period

- Seller financing above 25% often signals the bank sees elevated risk in the practice's cash flow or valuation

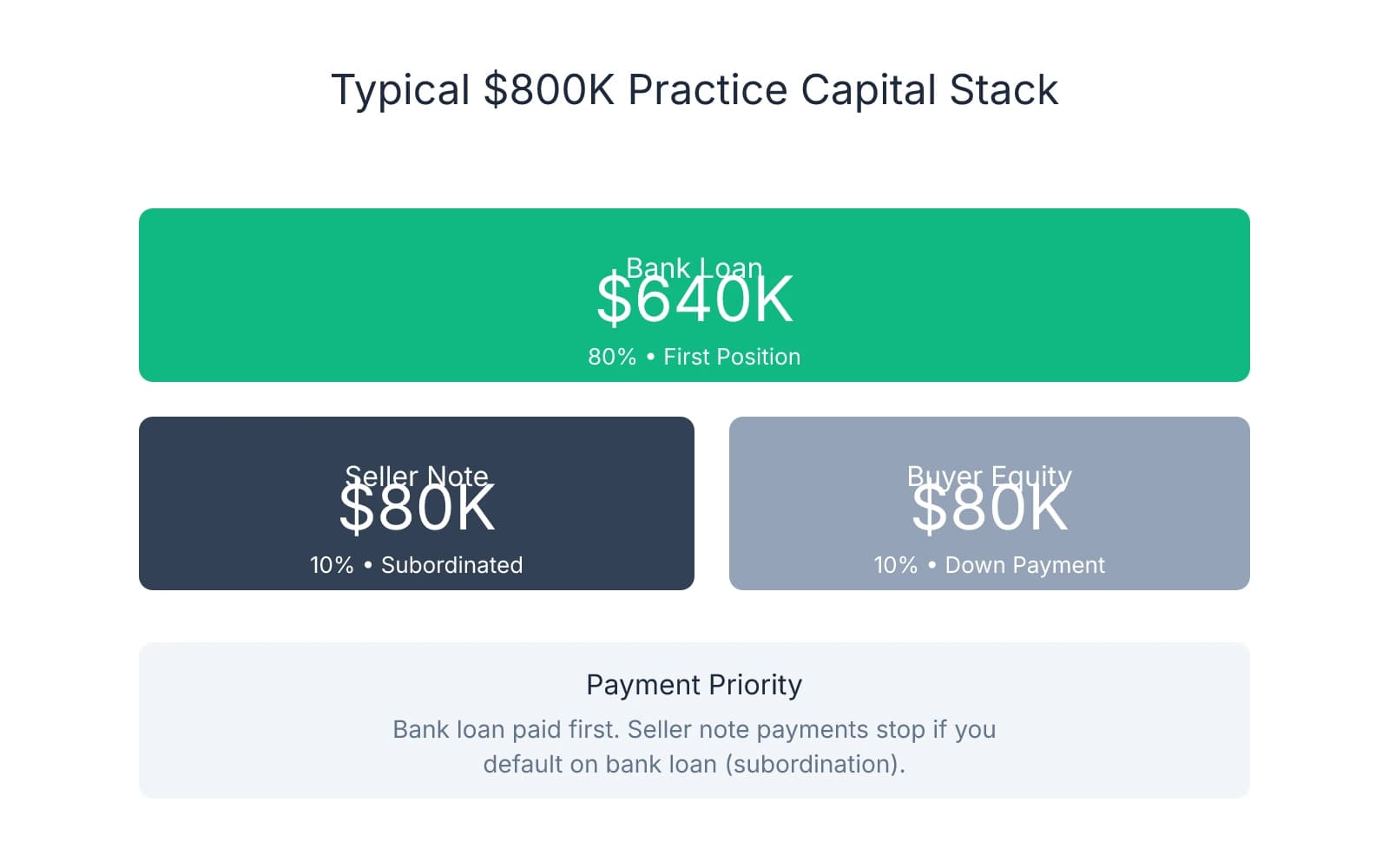

- A typical $800K practice might be financed with $640K bank loan (80%), $80K seller note (10%), and $80K buyer down payment (10%)

Seller Financing Typically Covers 10-20% of the Purchase Price, Subordinated to Your Bank Loan

When seller financing appears in a dental practice acquisition, it fills a specific slice of the capital stack—not the majority. The typical structure puts the bank in first position with 75-85% of the purchase price, the buyer contributing 10-15% as a down payment, and the seller carrying 10-20% as a promissory note. This arrangement reflects what banks will accept and what sellers can reasonably risk.

Subordination means the seller's claim on the practice sits behind the bank's. If you default on the bank loan, the seller stops receiving payments until the bank is made whole. SBA loans require a formal standby agreement (SBA Form 155) that legally prevents seller note payments during any period when the bank loan is in default. The seller's security interest is junior, which means they absorb more risk than the bank and typically charge a higher interest rate to compensate.

Here's what a standard capital stack looks like for an $800,000 practice:

| Component | Amount | Percentage | Payment Priority |

|---|---|---|---|

| Bank Loan | $640,000 | 80% | First position |

| Seller Note | $80,000 | 10% | Subordinated |

| Buyer Equity | $80,000 | 10% | Last (no repayment) |

This structure protects the bank's position while giving the seller some upside and the buyer a path to ownership with manageable cash requirements. The seller note typically carries a 3-7 year term with monthly payments, though some deals structure a balloon payment at the end to reduce the buyer's immediate cash flow burden.

When seller financing exceeds 25% of the purchase price, it's worth asking why. One possibility: the seller is confident in the practice and wants to maximize the sale price by making the deal accessible to more buyers. The other: the bank declined to fund the full amount because collections, patient retention, or equipment condition raised concerns. Practices with low hygiene production ratios or outdated equipment often see higher seller financing percentages because lenders won't extend full leverage.

The subordination structure also affects how you negotiate the seller note terms. Because the seller is taking more risk than the bank, they may push for a higher interest rate—often 6-8% compared to the bank's 5-6%. But subordination also gives you leverage: if the seller wants the deal to close, they need to accept that their note won't pay out if the practice underperforms and you can't service the bank debt.

One pattern worth noting: seller financing above 20% often pairs with earnout structures or extended transition periods. The seller is effectively saying, "I'll carry more of the risk if you'll agree to performance-based payments or keep me involved longer." That's not inherently bad, but it does signal the deal has structural complexity beyond standard financing.

Interest Rates on Seller Notes Range from 6-9%, with 3-7 Year Terms

Seller note interest rates typically sit between 6-9%—higher than most bank rates because the seller holds subordinated debt with no FDIC backing and limited recourse if the practice underperforms. The rate you negotiate depends on how much risk the seller perceives in the practice's stability, current market conditions, and whether the note is secured by specific assets or just a general lien on the practice.

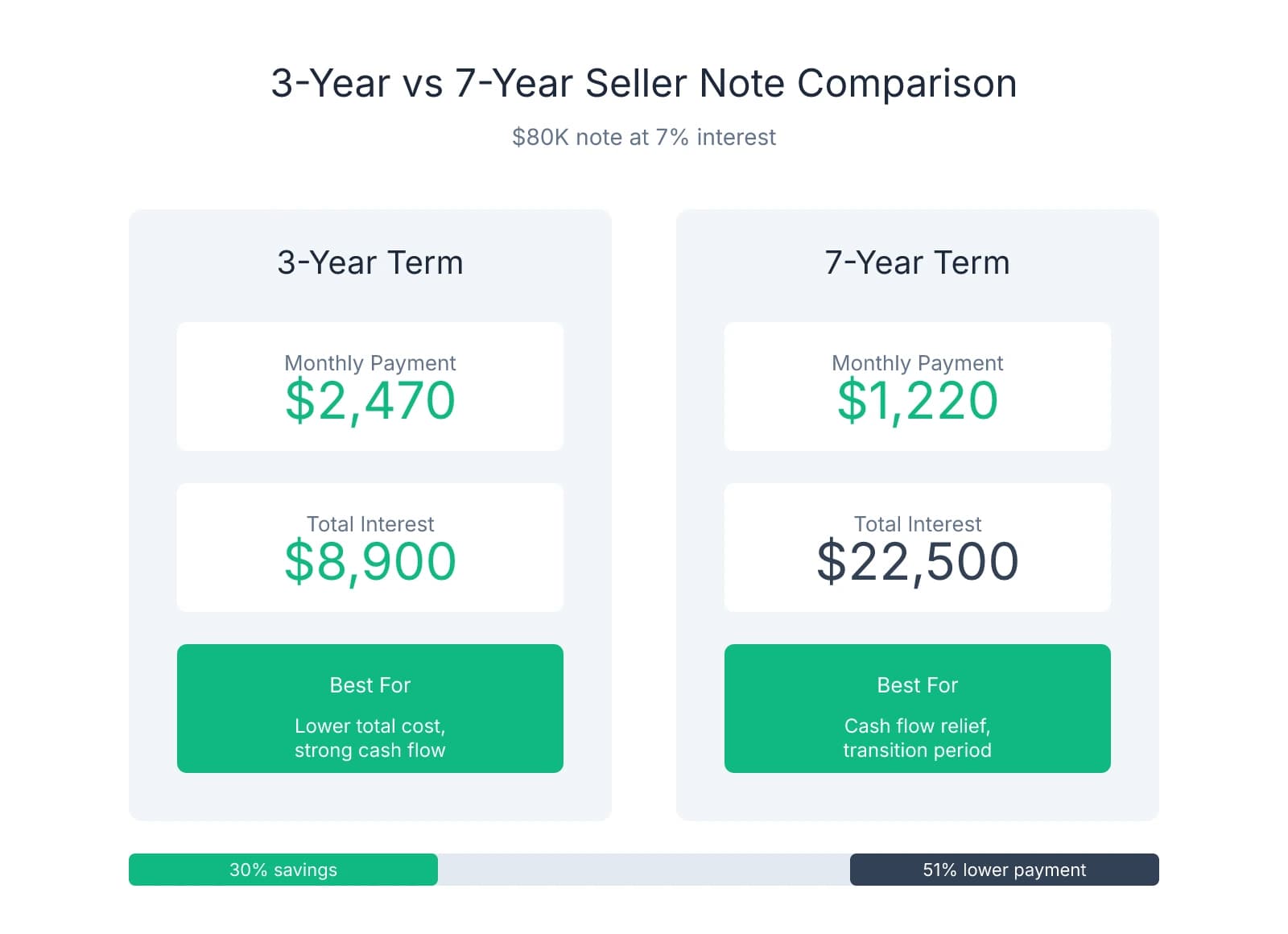

Most seller notes are structured with 3-7 year terms, with monthly payments covering both principal and interest. A 3-year term creates higher monthly payments but cuts total interest cost—on an $80,000 note at 7%, you'd pay roughly $2,470/month and $8,900 in total interest. Stretch that same note to 7 years and the monthly payment drops to $1,220, but total interest climbs to $22,500. The tradeoff is immediate cash flow relief versus long-term cost, and which structure works better depends on your break-even timeline.

Balloon payments—where you make smaller monthly payments and owe a large final payment at term end—are less common but sometimes used to ease cash flow in the first few years. A typical balloon structure might require interest-only payments for 3 years, then a lump sum of the full principal. This works if you're confident collections will grow enough to handle the balloon, but it also means you're not building equity in the note during the interest-only period.

Where rates and terms signal risk: if a seller proposes a rate above 9% or a term shorter than 3 years, they're likely trying to exit the note quickly. That's not always a red flag—some sellers simply want liquidity—but it can indicate concerns about whether the practice will sustain its current performance. A 2-year note at 10% tells you the seller wants their money back fast, which raises the question of what they know about patient retention or pending insurance contract changes that you don't.

One protection many buyers overlook is working capital provisions tied to the seller note. If the practice's cash flow dips in the first year and you can't make both the bank payment and the seller payment, the subordination agreement already protects the bank—but you're still contractually obligated to the seller. Negotiating a 90-day deferral clause or a temporary interest-only period can give you breathing room if collections lag during the transition.

The rate you accept should reflect the seller's actual risk exposure. If they're staying on for 90 days of structured transition support and the practice has stable collections with minimal insurance dependency, a 6-7% rate is reasonable. If they're exiting immediately and the practice relies heavily on a few high-production associates, 8-9% compensates the seller for the uncertainty they're absorbing. Anything above that range suggests either an aggressive seller or a practice with structural issues that couldn't secure full bank financing—particularly as rising interest rates compress practice valuations and tighten lending standards.

When Seller Financing Signals Confidence—and When It's a Red Flag

Seller financing isn't inherently good or bad—it's a structural choice that reveals something about the deal. The question worth asking is: why is the seller offering to carry part of the note? The answer determines whether you're looking at a competitive advantage or a warning sign the bank already spotted.

Tax deferral is one legitimate reason sellers offer financing. Structuring the sale as an installment allows the seller to spread capital gains over multiple years rather than taking the full tax hit in year one. This is especially common when the seller is close to retirement and wants to smooth their income for tax planning. If the seller's CPA recommended the structure and the practice has strong fundamentals, this is a strategic move—not a red flag.

Another reason: the seller believes in the practice's future performance and wants to make the deal more attractive in a competitive market. When multiple buyers are bidding on the same practice, offering 10-15% seller financing can tip the scales by lowering the buyer's upfront cash requirement. This signals confidence—the seller is willing to tie part of their payout to your success because they trust the practice's patient base, location, and systems.

But seller financing above 25% of the purchase price often tells a different story. When a bank declines to fund more than 75% of the deal, it's usually because they see risk the seller isn't disclosing—weak collections, high staff turnover, or outdated equipment that will require immediate capital investment. The seller steps in to fill the gap because they need the deal to close, not because they're confident in the practice.

Unsecured seller notes are another red flag. If the seller is offering financing but won't secure the note with collateral—typically a second lien on the practice assets or, in rare cases, the real estate—they're either taking on risk they don't fully understand or they know the practice won't support the debt. An unsecured note leaves the seller with no recourse if you default, which can create post-closing conflict when they realize they're last in line for payment behind your mortgage, payroll, and bank loan.

One pattern that should immediately raise questions: a seller who resists subordination or wants payments to continue even if you default on the bank loan. Standard subordination agreements—including the SBA's Form 155—explicitly state that seller note payments stop if the bank loan goes into default. If the seller is pushing for a structure where they get paid regardless of your bank status, they're either unfamiliar with how practice acquisitions work or they're trying to shift risk onto you in a way that no experienced advisor would recommend.

Where seller financing makes sense: when it's 10-20% of the purchase price, secured by a second lien, subordinated to the bank, and offered by a seller who's staying on for a structured transition period. That combination tells you the seller is confident enough to bet on your success but realistic enough to protect both sides with proper legal structure. If the seller is offering 30% unsecured financing and planning to exit within 30 days, it's worth asking whether the deal is worth pursuing at all.

Structuring Seller Financing to Protect Your Cash Flow and Avoid Post-Closing Surprises

The seller note terms you agree to in the LOI will shape your cash flow for the next 3-7 years—get them wrong and you'll spend the first year scrambling to cover payments instead of growing the practice. A well-structured seller note includes subordination language, realistic payment terms, and clear triggers for what happens if collections drop. A poorly structured note becomes a liability the moment you miss your first bank payment.

Subordination and standby provisions are non-negotiable if you're using bank financing. The seller note must explicitly state that payments stop if you default on the bank loan—this is what SBA Form 155 formalizes, but even conventional loans require similar language. Without this protection, you could be legally obligated to pay the seller while simultaneously in default with the bank, which creates a cash flow crisis neither party benefits from. Confirm this language appears in both the LOI and the final promissory note.

Where many buyers underestimate risk is in the payment schedule. A 3-year seller note at 8% on $100,000 means $3,130/month in combined principal and interest. If your bank loan is already consuming 50% of net income, adding another $3,130/month can push your debt service ratio above 70%—the threshold where most practices start feeling cash flow pressure. One protection worth negotiating: a 5-7 year term instead of 3 years. Extending the term to 7 years drops that monthly payment to $1,520, which gives you more room to absorb the inevitable dip in collections during the first 6-12 months.

Collateral structure determines what happens if you can't pay. Most seller notes are secured by a second lien on the practice assets—equipment, patient records, accounts receivable. This is standard and reasonable. What's not reasonable: a seller who wants a lien on your personal residence or other assets outside the business. If the practice fails, the seller's recourse should be limited to the practice itself, not your home equity. Push back on any personal guarantee that extends beyond the business assets.

One clause that rarely appears but should: a performance-based adjustment or deferral provision tied to collections. If gross revenue drops more than 15% in the first year, some seller notes allow you to defer payments for 90 days or switch to interest-only until collections stabilize. This isn't common, but it's worth proposing if the practice has high patient concentration or relies heavily on a few key insurance contracts.

Working capital is where most buyers get surprised. If the combined bank loan and seller note payments exceed 70% of net income, you won't have enough cash flow to cover payroll, supplies, and your own salary in the first year. Before signing, calculate your monthly debt service (bank + seller note) and compare it to the practice's trailing 12-month net income. If the ratio is above 70%, you need to either negotiate for more working capital at closing, extend the seller note term, or reduce the purchase price.

Get the seller note terms locked into the LOI, not just the purchase agreement. Many buyers assume the LOI's "seller financing: 10%, terms TBD" language is sufficient, but that leaves the rate, term, subordination, and collateral structure open for negotiation later—often when you've already spent $15,000 on due diligence and feel pressured to close. Specify the rate, term, subordination language, and collateral in the LOI so both sides know exactly what they're agreeing to before due diligence begins.

Before you sign, confirm these terms are documented:

- Subordination language stating payments stop if you default on the bank loan

- Term length (5-7 years preferred for cash flow protection)

- Interest rate (6-8% is standard for subordinated debt)

- Collateral limited to practice assets, not personal property

- Deferral or adjustment clause if collections drop >15% in year one

- Monthly payment amount and total interest cost over the term

The seller note isn't just a financing tool—it's a risk-sharing agreement that determines whether you'll have enough cash flow to operate the practice or spend the first year managing a debt crisis. Structure it with the same rigor you'd apply to negotiating the purchase agreement itself, and make sure your attorney reviews the subordination and collateral language before you commit.

Sources & References

The data and claims in this article are drawn from the following sources. We prioritize government data, peer-reviewed research, and established industry publications to ensure accuracy.

- Dental Practice Purchase Financing: Complete Guide - Jaffe Law— jaffelawpllc.comIndustry

- Interest Rates & Practice Values— www.integritypracticesales.com

- Should You Offer Seller Financing When Selling Your Dental Practice?— dentalpracticeguide.comIndustry

- What Dentists Need to Know About Seller Financing— www.dentalbuyeradvocates.com

- Best Practices: SBA Standby Agreements and Other Considerations ...— starfieldsmith.comIndustry

Frequently Asked Questions

Ready to navigate your practice sale?

Understanding seller financing terms is just the first step. Minty Plus provides expert guidance through the entire acquisition process, helping you structure deals that work and manage your practice post-close with confidence.